From a 52-week low of Rs 168 to Rs 584 in twelve months, Bajaj Consumer Care has been one of India's best-performing FMCG stocks. A deep dive into the fundamentals and technicals behind the move — and whether the rally has more to run.

Stock Snapshot (as of 9 June 2026)

The Rally in Context: How Far Has BAJAJCON Run?

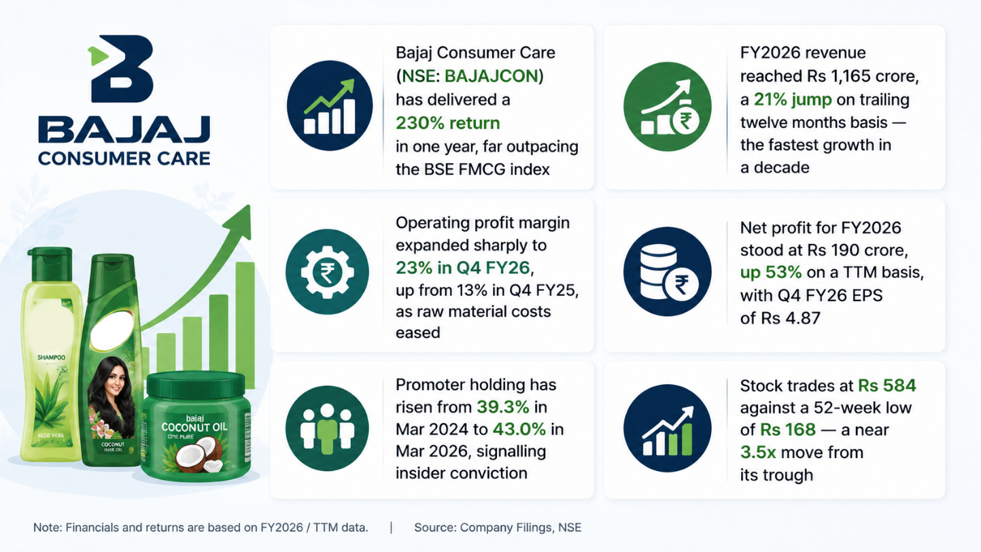

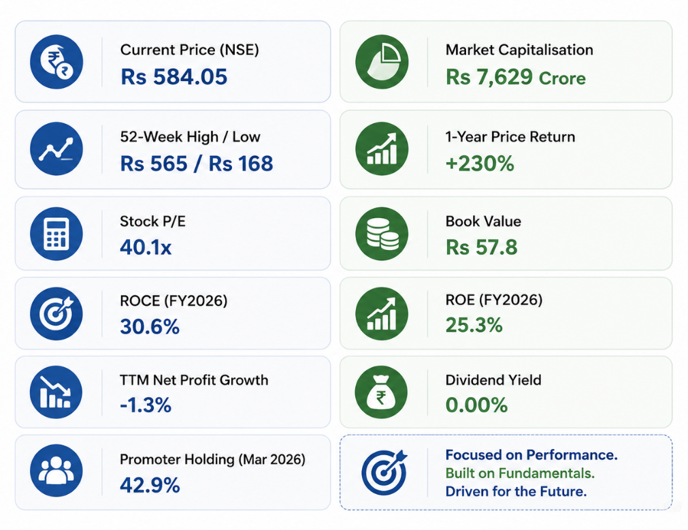

Bajaj Consumer Care's share price has undergone a dramatic re-rating over the past twelve months. From a fifty-two-week low of Rs 168, the stock has appreciated to Rs 584 as of 9 June 2026 — a gain of approximately 248% from the trough and a 230% return on a one-year basis. This performance places BAJAJCON among the top-performing large and mid-cap FMCG names in India over the past year, in a period when the broader Indian equity market has been under pressure.

The move has not been a linear one. The stock spent much of 2024 and early 2025 range-bound at deeply depressed levels, reflecting the poor operating performance of FY2025, when annual revenue fell slightly to Rs 965 crore and net profit dropped to Rs 125 crore — the lowest in nearly a decade. The re-rating began in earnest in the second half of 2025 as quarterly results started to show a clear inflection in operating leverage, and has accelerated sharply through the March and June 2026 quarters.

To understand whether the rally is sustainable, it is necessary to understand both the fundamental drivers that triggered it and the technical picture that has supported the price action.

Fundamental Drivers: Why the Business Turned Around

1. Revenue Inflection After Years of Stagnation

Bajaj Consumer Care's top line had been largely flat for nearly a decade. Revenue grew from Rs 817 crore in FY2015 to Rs 965 crore in FY2025 — a compound annual growth rate of less than 2%. This chronic underperformance relative to peers was one of the primary reasons the stock derated heavily through the decade, trading at a discount to FMCG peers on multiple valuation metrics.

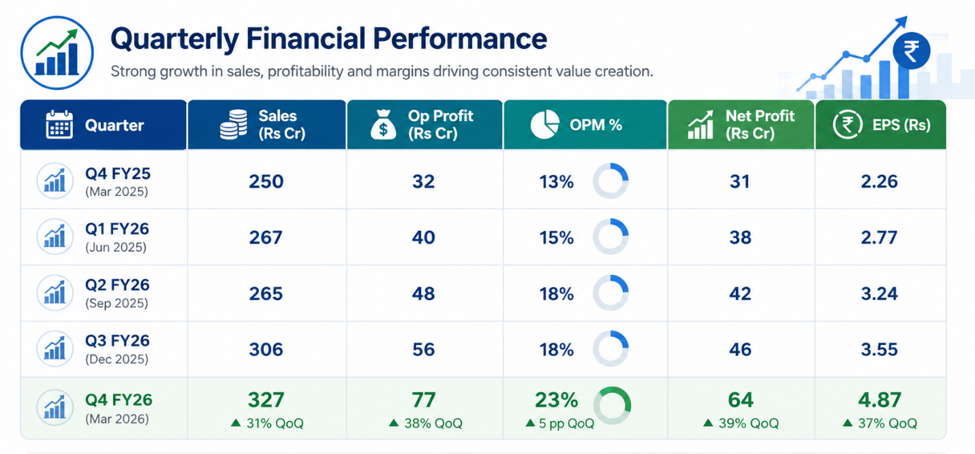

FY2026 marked a clear break from this pattern. Full-year revenue came in at Rs 1,165 crore, a year-on-year increase of approximately 21% and the first time the company has crossed the Rs 1,000 crore mark on an annual basis. More encouragingly, the acceleration has been visible across consecutive quarters: sales grew from Rs 267 crore in Q1 FY26 to Rs 306 crore in Q3 FY26 and Rs 327 crore in Q4 FY26, suggesting the momentum is building rather than front-loaded.

FY2026 revenue of Rs 1,165 crore represents a 21% year-on-year jump — the fastest top-line growth Bajaj Consumer Care has recorded in over a decade.

The growth has been driven by a combination of volume recovery in the core Bajaj Almond Drops Hair Oil franchise, price increases taken in prior periods flowing through the P&L, and outperformance from the company's newer product lines including Pure Coconut Oil, which grew 19% in FY2025 and has continued to gain distribution reach.

2. Operating Margin Expansion — The Key Re-Rating Trigger

The more powerful driver of the share price re-rating has been the dramatic recovery in operating profit margins. After compressing from 30%+ levels in FY2015-FY2019 to a trough of 13% in FY2025, operating margins have recovered sharply. The OPM reached 23% in Q4 FY26 — the highest quarterly margin in several years — up from just 13% in the same quarter of the prior year.

This margin recovery has been driven by two forces working simultaneously. First, raw material costs, particularly vegetable oils including almond oil and coconut oil, peaked and have since moderated, reducing the key input cost for hair oil manufacturing. Second, operating leverage has kicked in as revenues have grown at a faster pace than fixed cost growth, allowing the incremental revenue to drop through to the operating profit line at a high rate.

The trajectory is unambiguous. From a net profit of Rs 31 crore in Q4 FY25, the company delivered Rs 64 crore in Q4 FY26 — more than double — in the space of four quarters. This kind of earnings acceleration tends to attract significant market attention and justify a meaningful re-rating of the price-to-earnings multiple.

3. Working Capital Normalisation — A Watch Point

One area that warrants attention is the working capital cycle, which has stretched materially. Working capital days increased from 21 days in FY2025 to 124 days in FY2026, a significant widening that suggests the company is either extending more credit to distributors to drive volumes or facing slower collections as it pushes into new channels and geographies.

This working capital expansion is a potential flag. Rapid top-line growth financed by extended credit terms can mask underlying demand quality and creates receivables risk. Cash from operations came in at Rs 197 crore in FY2026 — a recovery from the weak Rs 65 crore in FY2025 — but investors should watch whether the working capital cycle tightens as distribution matures, or whether it continues to stretch.

Working capital days surged from 21 to 124 in FY2026 — a red flag worth watching. The company needs to demonstrate that revenue growth is not being funded by unsustainable credit extension.

4. Promoter Buying: A Confidence Signal

Promoter shareholding has risen steadily from 39.3% in March 2024 to 43.0% in March 2026. This consistent increase in promoter stake over two years is a meaningful signal of insider conviction in the company's recovery thesis. Promoters rarely increase holdings at scale unless they have a high degree of confidence in the near-term earnings trajectory.

The increase in promoter holding has also been accompanied by a modest decline in FII holding (from a peak of 14.76% in September 2023 to 9.70% in December 2025), with a notable jump back to 16.59% in March 2026 as institutional investors began to recognise the earnings inflection. The return of FII buying in the March 2026 quarter, coinciding with the strongest quarterly result in years, is a technically positive signal for continued institutional accumulation.

5. Debt-Free Balance Sheet and Return on Capital

Bajaj Consumer Care carries negligible debt — borrowings of just Rs 16 crore against total assets of Rs 945 crore as of March 2026. This effectively debt-free status means the company has full financial flexibility and does not face refinancing risk or interest cost pressure in a rising-rate environment.

ROCE has recovered from a trough of 19% in FY2025 to 30.6% in FY2026, and ROE stands at 25.3%. These are healthy return metrics that compare favourably with several larger FMCG peers, and the improvement in ROCE over a single year is directly attributable to the earnings recovery. As margins stabilise at higher levels, ROCE and ROE have scope to improve further.

Technical Analysis: Reading the Price Action

1-Year Chart: A Classic Recovery Pattern

The BAJAJCON chart over the past year reads as a textbook recovery from an oversold base. The stock spent much of 2024 trading in the Rs 170-220 range, consolidating at multi-year support levels after a prolonged decline from its 2019-era highs near Rs 400-450. This extended base-building phase, characterised by declining volume and narrowing price ranges, is typically a precursor to a sustained upward move.

The breakout began in earnest in mid-2025, with the stock clearing the Rs 250-260 resistance zone on above-average volume — a classic high-volume breakout that typically marks the beginning of a new trend phase rather than a short-covering bounce. From that level, the stock has made a series of higher highs and higher lows, the defining characteristic of an established uptrend.

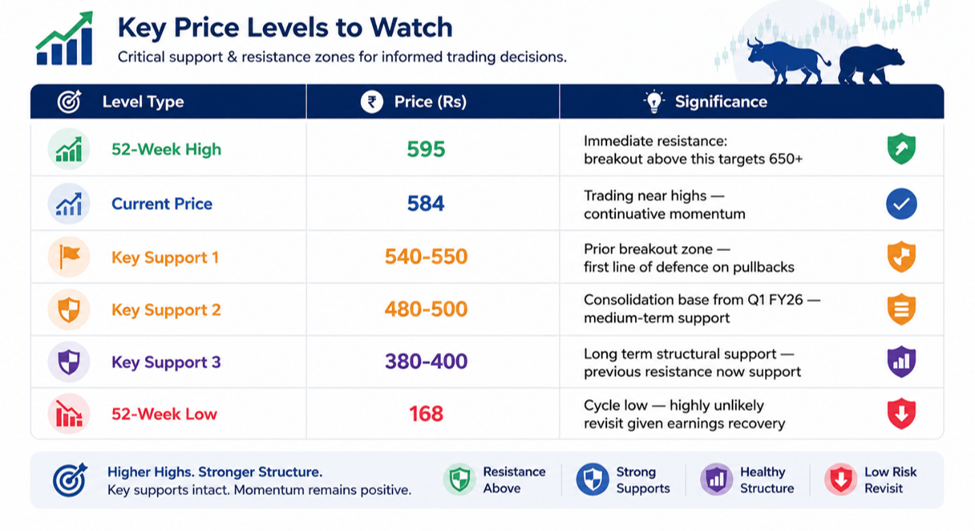

Key Technical Levels

Momentum Indicators

On a momentum basis, BAJAJCON has been in a strong uptrend. The stock has been trading well above both its 50-day and 200-day moving averages for much of the past year, a configuration that signals trend health. The 50-DMA has been consistently above the 200-DMA in a positive 'golden cross' formation, which many institutional traders use as a buy confirmation signal.

Relative Strength versus the BSE FMCG index has also improved materially. While the broader FMCG sector has faced headwinds from rural demand concerns and input cost pressures, BAJAJCON's category-specific tailwinds (hair oil being a low-unit-price, high-frequency purchase category) have allowed it to outperform.

Volumes on up-days have generally been higher than volumes on down-days over the past six months, a pattern of accumulation that is consistent with institutional buying rather than retail-driven speculation. The expansion of FII holdings from 9.70% to 16.59% in the March 2026 quarter confirms this reading.

Potential Red Flags in the Technical Picture

At Rs 584 and 40x trailing earnings, the stock is now trading at a meaningful premium to its historical average multiple. After a 230% gain in twelve months, momentum is extended and the stock is not cheap by any absolute valuation measure. Any earnings disappointment or guidance cut in the coming quarters would likely trigger a sharp correction, as stocks re-rated on earnings momentum are acutely sensitive to negative earnings surprises.

The stock is trading within 2% of its fifty-two-week high of Rs 595. A failure to make new highs and a close back below the Rs 540 level would be a short-term bearish signal that warrants caution. Investors entering at current levels should be aware that chasing price near 52-week highs always carries higher entry risk.

Peer Comparison: Is BAJAJCON Fairly Valued?

Relative to listed FMCG peers, Bajaj Consumer Care at 40x P/E is priced in line with the sector median. This is a notable re-rating from the deep discount at which it traded twelve months ago. The question for investors is whether a company with 4-5% five-year sales growth deserves the same multiple as larger, more diversified FMCG franchises.

BAJAJCON's quarterly sales growth of 30.4% stands out as the highest in the peer group by a considerable margin. ROCE of 30.6% also compares well with Godrej Consumer (19.1%) and Dabur (20.4%), though Colgate and Gillette operate on structurally higher returns. The case for the current valuation rests on whether the 30%+ quarterly growth rate is a new normal or a temporary catch-up from a low base.

If quarterly sales growth normalises toward the 10-15% range over the next few years — which is more typical of mature FMCG companies — then 40x earnings would be a full valuation. If the company sustains 20%+ growth as its newer products gain scale, the current multiple could prove to be reasonable in hindsight.

What Next? Bull Case, Base Case, and Bear Case

Bull Case: Sustained Earnings Upgrade Cycle

If Bajaj Consumer Care delivers another strong quarter in Q1 FY27, sustaining OPM above 20% and revenue growth above 20%, the earnings upgrade cycle would likely continue. Analysts who have not yet raised price targets would be forced to revise upward. FII holding, which jumped to 16.59% in March 2026, could continue expanding as global emerging market funds seek India FMCG exposure at a mid-cap size. Under this scenario, the stock has scope to reach Rs 680-720, implying approximately 35-40x forward FY27 earnings at an Rs 18-20 EPS run rate.

Base Case: Consolidation at Current Levels

The more likely near-term scenario is consolidation in the Rs 520-620 range as the market digests the sharp re-rating and waits for the next quarterly result to confirm that Q4 FY26's margin performance was not a one-quarter outlier. The working capital deterioration will also attract investor scrutiny. A stable, range-bound phase following a 230% gain is healthy and does not invalidate the longer-term thesis.

Bear Case: Earnings Disappointment Triggers Correction

If Q1 FY27 results show margin compression — due to input cost reversal, volume deceleration, or higher advertising and promotional spend — the stock could correct sharply to the Rs 420-480 range. At those levels it would trade at approximately 30-32x earnings — still not cheap in absolute terms, but more defensible given the balance sheet quality and return profile. Investors should note that FMCG stocks with extended working capital cycles and no dividend payout are vulnerable to sentiment shifts.

Frequently Asked Questions

Q. Why is Bajaj Consumer Care stock rising?

- The stock has risen due to a combination of earnings recovery, operating margin expansion, promoter buying, and institutional accumulation. Revenue grew 21% in FY2026, operating margins recovered to 23% in Q4 FY26, and net profit nearly doubled year-on-year in the latest quarter.

Q. What is Bajaj Consumer Care's 52-week high and low?

- The fifty-two-week high is Rs 595 and the fifty-two-week low is Rs 168. The stock has risen approximately 248% from its trough.

Q. Is BAJAJCON a good buy at current levels?

- At 40x trailing earnings, the stock is not cheap. Investors should weigh the earnings momentum against the stretched working capital cycle and absence of dividend payouts. Entry on dips toward the Rs 520-540 zone offers a better risk-reward ratio than chasing price near the 52-week high.

Q. What is the target price for Bajaj Consumer Care?

- No specific price target is provided in this article. At a 35-40x forward multiple on projected FY27 EPS of Rs 18-20, a range of Rs 630-800 represents the bull case. The base case assumes consolidation near current levels pending further earnings confirmation.

Q. Why is Bajaj Consumer Care not paying dividends?

- Dividend payout has fallen from 93% of profits in FY2019 to 0% in FY2025 and FY2026. The company has not disclosed a formal dividend policy change, but the reduction coincides with the period of weaker earnings and higher working capital requirements. A resumption of dividends as earnings recover would be a positive signal for long-term investors.