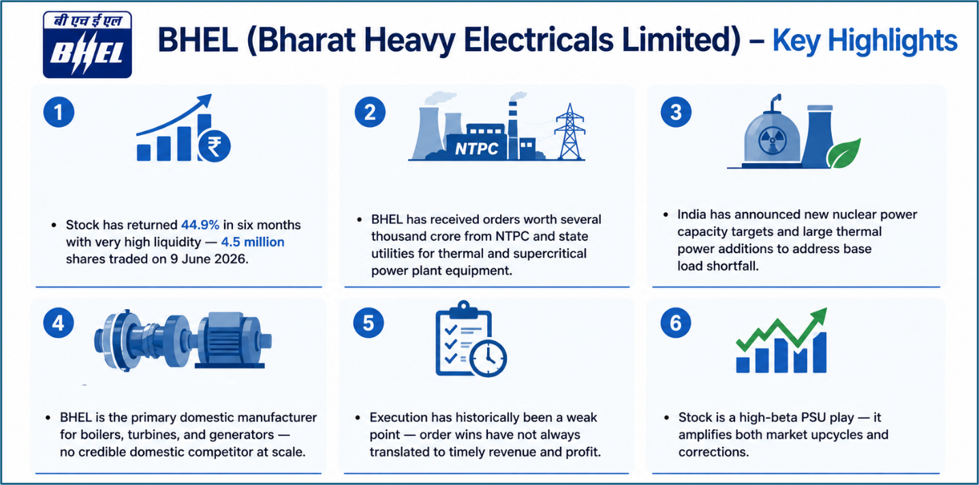

At Rs 390.7, Bharat Heavy Electricals has re-rated sharply on the back of a massive order book and India's thermal and nuclear power capacity addition plan — but execution challenges remain the key investor debate.

Why Has BHEL Surged?

Thermal Power Is Back on India's Energy Agenda

After years of policy ambiguity about the future of coal-based thermal power, the Indian government has made a decisive pivot. The Ministry of Power has identified a 80,000 MW shortfall in dispatchable (non-intermittent) power capacity that will develop as renewable energy penetration rises further. The solution is a combination of new coal-fired supercritical thermal plants and nuclear capacity — both of which require equipment that only BHEL can supply at scale in India.

NTPC has placed orders for new supercritical thermal units across multiple sites. State electricity boards in high-demand states like Maharashtra, Madhya Pradesh, and Rajasthan are also procuring new thermal capacity. Each 800 MW supercritical unit represents an order worth approximately Rs 5,000-6,000 crore for BHEL, covering the full range of boiler, turbine, and generator equipment.

Nuclear Power Expansion

India's nuclear power expansion programme has received significant policy support. The government has approved 10 new nuclear reactors and has an ambitious long-term target of 100 GW of nuclear capacity. BHEL has been a supplier to the nuclear programme for decades and has been working with NPCIL on indigenous Pressurised Heavy Water Reactor technology. This is a long-cycle business but provides multi-decade revenue visibility at very high margins.

BHEL's current order book is estimated at over Rs 1.5 lakh crore — the highest in the company's history. Revenue recognition from this book will flow over the next five to eight years, providing long-term earnings visibility.

Sector Insights: Thermal and Nuclear in India

The narrative that thermal power in India is in terminal decline has been challenged by the realisation that a 500 GW renewable energy grid still needs dispatchable backup capacity for the 40-50% of hours when solar and wind are unavailable. Grid stability requires firm power. New supercritical and ultra-supercritical plants — which are significantly more efficient and less polluting than old subcritical plants — are the government's preferred solution to this baseload requirement.

Technical View

BHEL is one of the most actively traded stocks on the NSE with 4.5 million shares changing hands on 9 June 2026. This high liquidity makes it a favourite among traders and institutional investors. The stock is in an uptrend on monthly charts but has faced resistance near the Rs 380-400 zone in recent weeks, suggesting consolidation after the sharp run-up. A clear close above Rs 400 would signal a continuation toward Rs 440-460.

The PSU sector in general has faced volatility, and BHEL is no exception. The stock remains highly sensitive to budget announcements, NTPC order disclosures, and any changes in government policy toward the power sector. Relative strength versus the Nifty PSU index has been outperforming.

BHEL has a long history of disappointing on execution. The order book is record-large, but the critical question is whether management capacity and supply chain capability have improved enough to deliver on this opportunity.

Bull, Base, and Bear Case

Bull Case — Rs 480-550

Improved execution leads to accelerating revenue recognition, margins recover toward 6-8% EBITDA as fixed cost absorption improves, and the government places additional thermal and nuclear orders. PSU re-rating continues. Target: Rs 480-550.

Base Case — Rs 350-420

Revenue grows steadily but execution delays persist. The market gives BHEL credit for its order book but remains cautious about margin delivery. Consolidation in the Rs 350-420 range is the base case.

Bear Case — Rs 240-290

Significant order execution delays, margin pressure from commodity costs, or a government policy shift away from new thermal capacity triggers a de-rating to 15-18x forward earnings.

What Next?

The upcoming quarterly result will be watched closely for revenue growth and margin trends. Order inflow announcements from NTPC and state utilities are near-term catalysts. BHEL remains a high-risk, high-reward play on India's power capacity addition cycle. The business quality is improving but is not yet at the level that justifies a set-and-forget approach.

Disclaimer

This article is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any securities. All market data as at 9 June 2026. Past performance is not indicative of future results. Investors should conduct their own due diligence and seek independent financial advice before making any investment decisions.