INDIA MARKET ANALYSIS

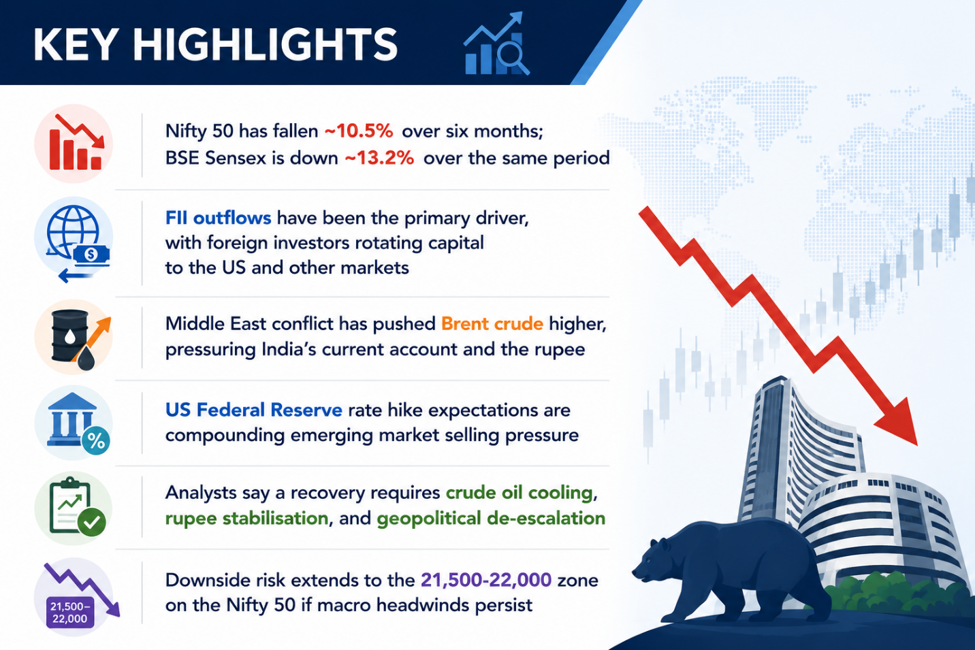

Nifty 50 and BSE Sensex have shed over 10% and 13% respectively in six months, with no clear floor in sight as multiple macro headwinds converge on Asia's third-largest economy.

9 June 2026 | Kalkine Media

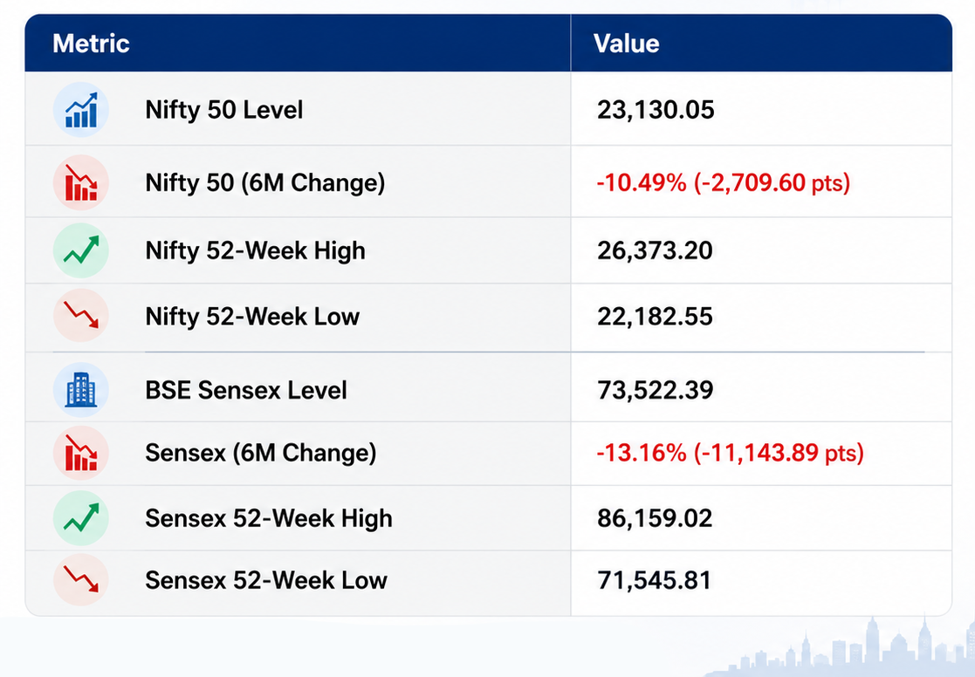

Market Snapshot (as at 9 June 2026)

The Six-Month Slide: What Has Happened

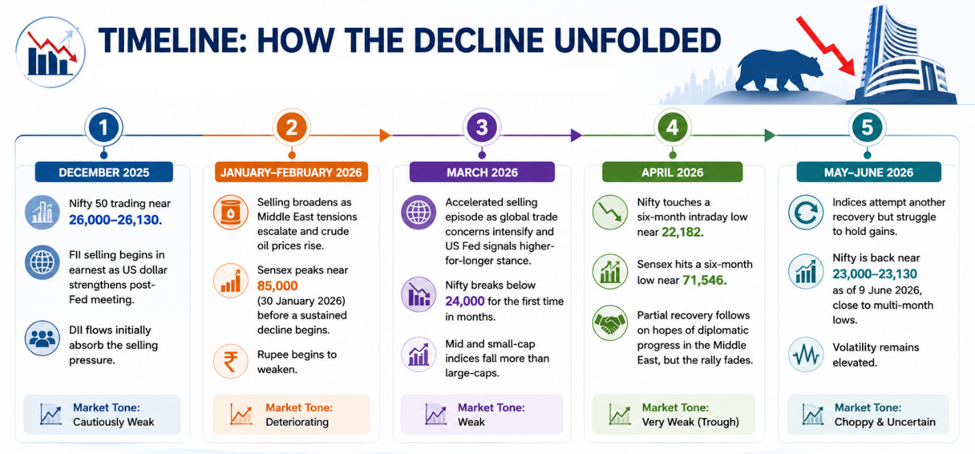

India's equity benchmarks entered 2026 under pressure and have not found their footing since. The Nifty 50, which stood at approximately 26,130 at the start of December 2025, has declined to 23,130 as of 9 June 2026, a fall of roughly 10.5%. The BSE Sensex has fared even worse on a percentage basis, shedding over 13% from above 84,600 to under 73,600 over the same window.

The decline has not been a single-event crash. It has been a slow, grinding erosion punctuated by bouts of acute volatility, particularly in March and April 2026, when the Nifty briefly dipped below the 22,200 level before staging a partial recovery. That recovery has since reversed, and the index is again approaching its six-month lows, raising questions about whether the current phase is a prolonged correction or the beginning of a structural bear market.

What makes the current episode particularly painful for domestic investors is the contrast with global markets. While Indian indices have been falling, several international benchmarks, including US technology indices, have moved in the opposite direction, hitting new highs. This divergence has reinforced the case for foreign capital rotation out of India and into markets with more visible earnings momentum.

Driver 1: Foreign Institutional Investor Outflows

The most immediate and quantifiable pressure on Indian equities has come from Foreign Institutional Investors (FIIs), who have aggressively reduced their exposure to Indian stocks over the past six months. FIIs are a structurally important source of capital for Indian markets; their buying and selling activity can have an outsized impact on index levels given the relatively limited depth of domestic institutional flows.

The outflow cycle began in earnest in the final quarter of 2025, initially driven by a stronger US dollar and rising US Treasury yields that made dollar-denominated assets comparatively more attractive. As the dollar strengthened and US equity markets continued to post gains, the opportunity cost of holding Indian equities rose for global portfolio managers operating in dollar terms.

The trend accelerated into early 2026 as several large emerging market funds rebalanced away from India in favour of markets with lower valuations and more direct exposure to the AI-driven US equity rally. Indian markets, which had been trading at premium multiples relative to other emerging markets through much of 2024 and 2025, became a natural source of funds as global investors sought to reduce risk.

Domestic Institutional Investors (DIIs), particularly mutual funds backed by retail Systematic Investment Plan (SIP) inflows, have partially absorbed FII selling. However, the scale of foreign outflows has exceeded DII buying capacity during peak selling episodes, resulting in significant index falls on high-volume days.

Driver 2: Rising Crude Oil Prices and the Middle East

India imports approximately 85% of its crude oil requirement, making it one of the most exposed major economies to global oil price movements. The escalation of conflict in the Middle East through late 2025 and into 2026 has pushed Brent crude prices higher, creating a multi-channel problem for the Indian economy.

Higher crude prices directly widen India's trade deficit, as the country's import bill rises without a corresponding increase in export revenues. A wider trade deficit puts downward pressure on the Indian rupee, as more dollars must be sold to pay for oil imports. A weaker rupee, in turn, makes imports more expensive in rupee terms, feeding into domestic inflation, which complicates the Reserve Bank of India's monetary policy stance.

For corporate India, rising crude oil prices have a broad earnings impact. Oil marketing companies face margin compression when they are unable to fully pass on input cost increases. Airlines, logistics companies, paint manufacturers, tyre producers, and a wide range of consumer goods companies face higher raw material and operating costs. These earnings pressures have been reflected in downward revisions to FY2026 and FY2027 earnings estimates, which has weighed on valuations.

Geopolitical risk premiums in the oil market are notoriously difficult to price and even harder to time. Markets have at times discounted Middle East conflict as a temporary spike, only to see prices remain elevated as conflicts persist longer than initially expected. The current episode has followed a similar pattern, with each perceived de-escalation followed by fresh flare-ups.

Driver 3: US Federal Reserve Rate Expectations

The Federal Reserve's monetary policy trajectory has been a persistent source of pressure on emerging markets, and India has not been immune. Through 2024 and into early 2025, markets had priced in a relatively aggressive easing cycle as US inflation moderated. However, a resilient US labour market and a rebound in services inflation through late 2025 forced a reassessment of that view.

By the start of 2026, expectations had shifted toward the Fed maintaining higher-for-longer rates, with some forecasters even pricing in the possibility of additional rate increases. This backdrop strengthened the US dollar, drove US Treasury yields higher, and reduced the yield differential between Indian fixed income and US assets. For global fixed income and equity investors, the relative attractiveness of Indian assets declined.

Higher US rates also increase the cost of external borrowing for Indian corporates that have issued dollar-denominated debt. As refinancing conditions tighten, overleveraged companies face earnings pressure, and credit conditions for new investment tighten. This effect, while not immediately visible in index-level data, acts as a slow brake on corporate expansion and investment, with delayed but real consequences for earnings growth.

The combination of a stronger dollar, higher US yields, and the prospect of further Fed tightening has historically been associated with periods of underperformance for emerging market assets relative to developed markets. The current cycle fits this pattern closely.

Driver 4: Global Trade Uncertainty and Tariff Risk

Broader global trade uncertainty has added another layer of pressure on Indian equities. Expanded US tariff policies and the prospect of retaliatory measures from trading partners have created uncertainty about the global growth outlook, particularly for export-oriented economies and sectors.

India's direct exposure to US tariffs is lower than China's, given the different composition of bilateral trade. However, the indirect effects through global supply chain disruptions, commodity price volatility, and reduced appetite for risk assets in general have still been felt. Information technology companies, which generate a large share of their revenues from US clients, have faced concerns about discretionary spending cuts as US corporate margins come under pressure.

The IT sector, which has historically been a defensive anchor for the Nifty 50 given its relatively low correlation to domestic economic cycles, has provided less shelter in the current downturn than in previous episodes. This has reduced the diversification benefit that large-cap technology weightings typically provide to the index.

How Much Further Can Indian Markets Fall?

The question of further downside is not easily answered, but it can be framed through a combination of technical levels, valuation metrics, and macro scenario analysis.

Technical Perspective

From a technical standpoint, the Nifty 50 has already broken several key support levels that had previously held during prior corrections. The index has been making lower highs and lower lows on monthly charts, a pattern that technical analysts typically read as a downtrend in force. Key levels to watch on the downside include the 22,000-22,182 range, which represents the recent six-month low, and the 21,000-21,500 zone below that, which corresponds to prior consolidation from mid-2024.

A sustained break below 22,000 on the Nifty 50 would likely trigger stop-loss selling and increase the probability of a move toward 21,000-21,500. In a more adverse macro scenario involving a significant crude oil spike or a disorderly rupee depreciation, the 20,000 level, last seen in early 2024, cannot be entirely ruled out.

Valuation Perspective

Indian equities remain at a premium to broader emerging market peers on most valuation metrics, including price-to-earnings and price-to-book ratios. While this premium has historically been justified by India's superior earnings growth trajectory and the quality of its listed companies, a prolonged period of earnings downgrades could erode that justification.

At current levels, the Nifty 50 is trading at a forward price-to-earnings ratio that has compressed from the elevated levels seen in late 2024, but is still not clearly cheap relative to historical averages. For the market to find a sustainable floor, either earnings estimates need to stabilise or valuations need to compress further to a level that attracts fresh buying from value-oriented investors.

Macro Scenario Analysis

Three broad scenarios can be outlined for the months ahead:

Scenario 1 — Gradual Stabilisation (Base Case)

If Middle East tensions plateau without further escalation, crude oil prices moderate toward USD 75-80 per barrel, and the US Fed signals a pause, Indian markets could find a base in the 22,000-23,000 range on the Nifty 50. A gradual recovery toward 24,500-25,000 over the second half of 2026 is possible under this scenario, but it is unlikely to be linear or swift.

Scenario 2 — Prolonged Pressure (Bear Case)

If geopolitical tensions intensify, crude oil sustains above USD 90 per barrel, the rupee breaches 90 against the dollar, and the US Fed delivers another rate hike, the Nifty 50 could extend its decline to the 20,500-21,500 range. This scenario would likely be associated with a broad-based earnings downgrade cycle and significantly weaker sentiment in the mid and small-cap segments.

Scenario 3 — Positive Surprise (Bull Case)

A ceasefire or credible diplomatic progress in the Middle East, combined with a sharp fall in crude prices and a dovish Fed pivot, could trigger a sharp relief rally. Under this scenario, FIIs could reverse their selling, and the Nifty could recover toward 25,000-25,500 relatively quickly. However, this scenario currently has lower probability given the structural nature of several headwinds.

What Would It Take for Markets to Recover?

Analysts at institutions including Kotak Neo and several domestic brokerages have consistently identified three prerequisites for a sustained market recovery:

- De-escalation of Middle East Conflict: A ceasefire, peace agreement, or credible diplomatic process that removes the geopolitical risk premium from oil prices would be the single most powerful catalyst for Indian market recovery. It would simultaneously ease crude prices, stabilise the rupee, and reduce the risk aversion that is driving FII outflows.

- Stabilisation of Brent Crude: Even without full conflict resolution, a sustained cooling in oil prices below USD 75-80 per barrel would meaningfully reduce pressure on India's current account, corporate margins, and inflation outlook. It would give the RBI more room to ease monetary policy if needed, which would support market valuations.

- Rupee Stabilisation: A stabilisation of the Indian rupee against the US dollar would reduce the currency-related exit pressure on FIIs. For foreign investors holding Indian equities in dollar terms, a weakening rupee erodes returns independent of stock price performance. Rupee stabilisation would make the risk-reward of Indian equities more attractive from a global capital allocation perspective.

Beyond these immediate triggers, a longer-term recovery would also benefit from earnings upgrades, improvement in global risk appetite toward emerging markets, and evidence that domestic consumption demand remains resilient despite cost-of-living pressures.

Domestic Factors: What Is Holding Up

It is worth noting that not all domestic indicators are negative. India's economic growth rate remains among the fastest of any major economy. The government's capital expenditure programme has continued, supporting infrastructure and construction activity. Domestic consumption, while showing some stress at the lower income end due to food inflation, has held up reasonably well in urban segments.

The Reserve Bank of India has maintained a broadly calibrated monetary stance, and the banking system remains well-capitalised. Non-performing loan ratios, a source of significant stress in previous downturns, are at multi-decade lows for the listed banking sector. This provides a degree of systemic resilience that was absent during earlier market downturns such as 2018-2019.

Retail investor participation through SIPs into mutual funds has remained remarkably sticky, providing a regular flow of domestic buying that has cushioned the impact of FII selling. Monthly SIP inflows into equity mutual funds have continued to run at elevated levels, reflecting the maturing of India's domestic investor base and a cultural shift toward financial market participation among the middle class.

These domestic positives suggest that the current weakness is primarily externally driven rather than a symptom of a fundamental deterioration in India's economic prospects. However, external pressures can persist for longer than expected, and their secondary effects on corporate earnings and credit conditions can compound over time.

Conclusion: A Correction with Unresolved Catalysts

Indian equity markets are navigating a confluence of external headwinds that have few quick fixes. The combination of FII outflows, elevated crude oil prices, a weakening rupee, and US rate uncertainty has created a difficult environment for risk assets, and the Nifty 50 and BSE Sensex have reflected this reality in their six-month performance.

The floor for this correction is not yet clearly defined. On a technical and valuation basis, the 21,500-22,000 range on the Nifty 50 represents meaningful support, but a break below it in an adverse macro scenario cannot be excluded. A recovery toward 25,000 and beyond requires at least some resolution of the macro headwinds, particularly on crude oil and geopolitics, neither of which is predictable in timing.

For long-term domestic investors, history suggests that corrections driven by external macro factors tend to create entry opportunities in high-quality Indian businesses, provided the underlying economic fundamentals remain intact. India's structural growth story, demographic dividend, and expanding domestic market have not changed. What has changed is the near-term price at which that story can be accessed.

The current environment calls for selectivity, patience, and attention to global macro signals rather than a blanket optimism or pessimism about the Indian market as a whole.

Disclaimer

This article is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any securities. All market data referenced as at 9 June 2026. Past performance is not indicative of future results. Investors should seek independent financial advice before making any investment decisions. Kalkine Media Pty Ltd does not hold an Australian Financial Services Licence.