Highlights

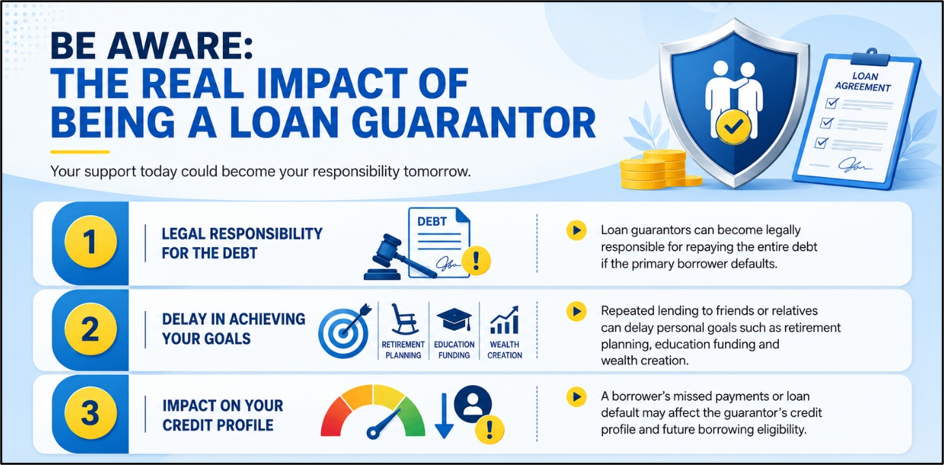

- Acting as a loan guarantor can create legal repayment obligations.

- Lending money repeatedly may delay personal financial goals and savings.

- Credit scores and borrowing capacity can be affected by another person's repayment behaviour.

Helping family members or friends during financial hardship is often viewed as an act of support and trust. Whether it involves lending money directly or agreeing to become a loan guarantor, such decisions are frequently influenced by emotional considerations rather than financial analysis.

While occasional assistance may not create significant problems, repeated financial support or loan guarantees can expose individuals to risks that affect savings, investments, borrowing capacity and long-term financial security. Financial planners frequently advise people to evaluate these commitments carefully before agreeing to them.

The Reality Behind Loan Guarantees

Many people believe that becoming a guarantor is merely a procedural formality required by lenders. However, a guarantor assumes legal responsibility for the debt if the primary borrower fails to meet repayment obligations.

If repayments are delayed or the borrower defaults, lenders may seek recovery from the guarantor. This can create a substantial financial burden, particularly if the loan amount is significant. In addition, the guaranteed loan may influence the guarantor's financial profile and future borrowing eligibility.

Because of these obligations, financial experts often recommend reviewing a borrower's repayment capacity and financial discipline before agreeing to guarantee a loan.

Source: Analysis by Kalkine

When Personal Lending Becomes Complicated

Direct lending between friends and relatives introduces a different set of challenges. Unlike formal lending arrangements, personal loans are often based on verbal commitments and mutual trust.

Repayment schedules may remain unclear, discussions about money can become uncomfortable and lenders may hesitate to request repayments in order to preserve relationships. Over time, financial ambiguity can lead to frustration and strained personal connections.

In many situations, the issue extends beyond the money itself. The lack of clearly defined terms can create misunderstandings that affect both finances and relationships.

Opportunity Cost: The Overlooked Financial Impact

One of the most underestimated consequences of lending money is opportunity cost. Funds provided to others are no longer available for personal financial priorities.

Emergency funds, retirement planning, children's education, property purchases and long-term investments may be delayed when substantial amounts are repeatedly directed toward supporting others. This impact may not be immediately visible, but it can accumulate over several years.

Individuals often view financial assistance as temporary, yet recurring support can gradually weaken their own financial position.

Credit Profile Risks Can Extend Beyond the Borrower

Many people are unaware that their credit standing can be affected by loans they guarantee or co-borrow.

If the borrower misses payments, restructures the loan or defaults, the guarantor's credit profile may also face scrutiny depending on lender reporting practices. This can affect future applications for home loans, personal loans, business financing and premium credit products.

In some cases, individuals only become aware of these consequences when applying for their own credit facilities years later.

Why Emotional Decisions Often Create Financial Stress

Financial requests from family members and close friends can generate emotional pressure. Many people agree to lend money or provide guarantees because they fear appearing unsupportive, distrustful or selfish.

However, decisions made primarily to avoid guilt can create long-term anxiety. If the borrower struggles financially, the lender or guarantor may face ongoing uncertainty regarding repayment. Eventually, financial stress can affect trust, communication and personal relationships.

Community discussions on personal finance forums frequently highlight cases where individuals assumed loans on behalf of friends and later faced repayment challenges themselves.

Setting Financial Boundaries Matters

Providing financial assistance is not inherently problematic. Families and friends often support each other during difficult periods.

However, experts generally recommend establishing clear boundaries, understanding repayment expectations and ensuring that any support provided does not compromise personal financial stability. Evaluating affordability and discussing responsibilities openly can help reduce misunderstandings later.

In some situations, maintaining financial boundaries may help preserve relationships by reducing the likelihood of resentment and dependency.

Key Risks

- Guarantors can become legally liable for unpaid loans.

- Personal lending may delay savings and investment goals.

- Borrower defaults can affect future credit applications.

- Financial disputes may strain family and personal relationships.

Summary

Helping friends or relatives financially can appear straightforward initially, but personal loans and loan guarantees may create long-term consequences. Guarantors assume legal repayment responsibility, while informal lending can affect savings, investments and financial goals. Credit profiles may also be impacted if borrowers fail to meet obligations. Clear boundaries, realistic affordability assessments and transparent expectations can help reduce financial and relationship-related risks.

FAQs

Q: What happens if a borrower defaults on a loan I guaranteed?

A: The lender may seek repayment from you because guarantors share legal responsibility for the debt.

Q: Can guaranteeing a loan affect my credit profile?

A: Yes, repayment issues linked to guaranteed loans may influence borrowing eligibility and credit assessments.

Q: Is lending money to relatives always a financial risk?

A: Not necessarily, but unclear repayment terms and repeated lending can create financial and relationship challenges.