Highlights

- Interest rate movements can influence loan costs, bond values and investment returns.

- Rising rates generally reduce bond prices, while falling rates can support bond valuations.

- Long-term bonds typically face greater interest rate sensitivity than short-term securities.

Interest rate changes are among the most closely watched developments in financial markets because they affect borrowing costs, savings returns and investment performance. Whether an individual has a home loan, owns bonds, invests in debt mutual funds or participates in equity markets, shifts in interest rates can influence financial outcomes.

Interest rate risk refers to the possibility that changes in market interest rates may affect the value of investments, particularly fixed-income securities such as bonds. Understanding how this risk works can help investors make more informed decisions about asset allocation and portfolio management.

Source: Analysis by Kalkine

Understanding the Basics of Interest Rate Risk

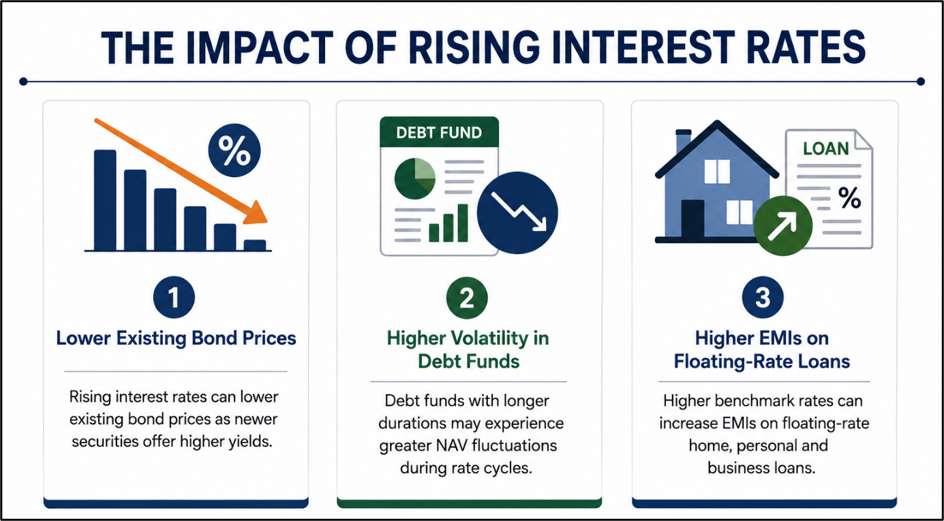

Interest rate risk arises because bond prices and interest rates generally move in opposite directions. When market interest rates rise, newly issued bonds offer higher yields, making existing lower-yield bonds less attractive. As a result, the market value of older bonds may decline.

Conversely, when interest rates fall, existing bonds with higher coupon rates become more attractive, potentially increasing their market value.

This relationship makes interest rate movements a key consideration for investors holding bonds, debt funds and other fixed-income instruments.

Why Bond Prices React to Interest Rate Changes

Consider an investor holding a bond paying 7 percent interest. If newly issued bonds begin offering 8 percent due to rising market rates, investors may prefer the newer bonds. To remain competitive, the older bond's market price may fall.

The reverse can also occur when rates decline. Existing bonds offering higher coupons can attract greater demand, potentially pushing their prices upward.

As a result, investors who need to sell bonds before maturity may experience gains or losses depending on prevailing interest rate conditions.

Long-Term Bonds Face Greater Sensitivity

One of the most important aspects of interest rate risk is duration. Generally, bonds with longer maturities are more sensitive to interest rate changes than shorter-term bonds.

A long-dated bond has more future interest payments that can be affected by changes in market rates. Consequently, a rise in interest rates may have a larger impact on its market value.

Shorter-term bonds usually experience lower price fluctuations because they mature sooner, reducing exposure to future rate movements.

Impact on Loans and Borrowing Costs

Interest rate changes do not affect only investors. Borrowers can also experience the effects through changes in loan costs.

When benchmark rates increase, banks may raise lending rates, leading to higher EMIs for borrowers with floating-rate loans. Home loans, personal loans and business borrowings can become more expensive.

When rates decline, borrowers may benefit from lower financing costs, although the speed and extent of transmission can vary across lenders.

Recent monetary policy discussions have kept attention focused on benchmark rates, given their influence on borrowing costs and broader economic activity. The Reserve Bank of India maintained its policy repo rate at 5.25 percent in June 2026 while monitoring inflation and currency-related developments.

Effect on Debt Funds and Fixed-Income Portfolios

Debt mutual funds that invest in government securities, corporate bonds and money market instruments are also exposed to interest rate risk.

Funds holding long-duration bonds may see greater NAV fluctuations when rates change. In contrast, ultra-short-duration and low-duration funds generally experience lower sensitivity.

Investors often review a fund's average maturity and duration profile to understand its potential exposure to interest rate movements.

Influence on Equity Markets

Interest rates can also affect stock markets. Higher borrowing costs may influence corporate profitability and investment decisions. Additionally, rising bond yields can make fixed-income investments more attractive relative to equities.

Lower rates, on the other hand, can improve liquidity conditions and reduce financing costs for businesses, factors that investors often monitor while evaluating market conditions.

Managing Interest Rate Risk

While interest rate risk cannot be eliminated entirely, investors may adopt several approaches to manage exposure.

Diversification across asset classes, investing in bonds with varying maturities and maintaining a balanced portfolio can help reduce concentration risk. Some investors also use bond ladders or a mix of short- and long-duration securities to navigate changing rate environments.

Understanding investment objectives, time horizons and risk tolerance remains essential when evaluating interest rate-sensitive assets.

Key Risks

- Rising interest rates can reduce existing bond market values.

- Long-duration funds may witness higher NAV volatility.

- Floating-rate borrowers may face increased EMI obligations.

- Rapid policy changes can affect portfolio valuations unexpectedly.

Summary

Interest rate risk is a key factor affecting bonds, debt funds, loans and broader financial markets. Bond prices generally move inversely to interest rates, while long-term securities tend to be more sensitive than shorter-term instruments. Borrowers may experience changes in loan costs as rates move. Diversification, duration management and awareness of policy developments can help investors understand and manage interest rate-related exposure.

FAQs

Q: What is interest rate risk?

A: Interest rate risk is the possibility that changing market rates affect bond prices, debt investments and borrowing costs.

Q: Which investments are most affected by interest rate risk?

A: Bonds, debt mutual funds, government securities and other fixed-income instruments are typically most sensitive to rate changes.

Q: Why do long-term bonds face higher interest rate risk?

A: Longer maturities increase exposure to future rate movements, making bond prices more sensitive to changing yields.