Highlights

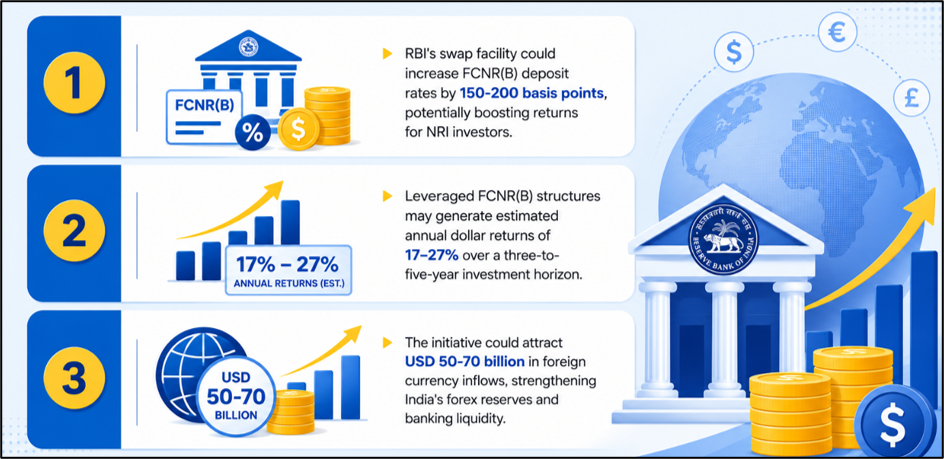

- RBI's swap facility may increase FCNR(B) deposit rates by 150-200 basis points.

- Leveraged structures could generate estimated annual dollar returns of 17-27 percent.

- The initiative may attract USD 50-70 billion in foreign currency inflows.

Foreign Currency Non-Resident (Bank), or FCNR(B), deposits have come back into focus after the Reserve Bank of India (RBI) introduced measures aimed at attracting foreign currency inflows from non-resident Indians (NRIs). The latest initiative is designed to lower hedging costs for banks, potentially enabling them to offer higher returns on FCNR(B) deposits.

The move has generated interest among NRI investors because FCNR(B) deposits are maintained in foreign currencies, helping protect depositors from direct rupee exchange-rate fluctuations while offering fixed-income returns.

Source: Analysis by Kalkine

Source: Analysis by Kalkine

RBI's Swap Facility Could Improve Deposit Returns

The RBI has introduced a concessional swap facility for fresh FCNR(B) deposits with maturities ranging from three to five years. The facility will remain available until September 30, 2026, and is intended to reduce the hedging burden faced by banks while mobilising overseas deposits.

Market estimates indicate that the reduction in hedging costs could improve FCNR(B) deposit rates by approximately 150 to 200 basis points. The central bank has also indicated that banks are expected to pass on part of this benefit to depositors through improved returns.

How Leveraged Structures Can Enhance Returns

A key feature of the latest framework is the ability for banks to offer leverage to eligible clients investing in FCNR(B) deposits. Under such structures, investors may combine their own capital with borrowed funds, increasing the amount invested in the deposit.

Based on prevailing assumptions regarding borrowing costs and deposit yields, leveraged strategies could potentially generate annual dollar-denominated returns ranging from 17 percent to 27 percent over a three-to-five-year investment horizon. Actual outcomes would depend on funding costs, leverage levels and prevailing market conditions.

Comparison With the 2013 FCNR(B) Programme

The latest initiative has invited comparisons with the FCNR(B) mobilisation programme launched in 2013.

During that period, concessional swap arrangements helped Indian banks mobilise significant foreign currency deposits. Historical data show that the earlier programme attracted substantial overseas inflows and contributed to strengthening foreign exchange reserves.

While current global interest rate conditions differ from those seen in 2013, the latest support mechanism seeks to offset part of the hedging expense, making FCNR(B) deposits more attractive than they would otherwise be under prevailing market conditions.

Potential Impact on Foreign Exchange Reserves

The initiative is expected to support India's foreign exchange reserves by encouraging additional inflows from overseas investors.

Market estimates suggest the programme could attract between USD 50 billion and USD 70 billion if participation remains favourable. Increased foreign currency inflows may help improve reserve buffers and support liquidity conditions in the banking system.

The RBI has also introduced operational guidelines, including a one-year lock-in requirement for deposits raised under the scheme, to support stability and prevent early exits.

Understanding FCNR(B) Deposits

FCNR(B) deposits allow NRIs to maintain fixed deposits in designated foreign currencies through Indian banks.

These deposits are available in currencies such as the US dollar, euro, pound sterling, Japanese yen, Canadian dollar and Australian dollar. Since both principal and interest are repaid in the same foreign currency, investors are protected from direct rupee depreciation risk during the deposit tenure.

FCNR(B) deposits are often considered by NRIs seeking foreign currency exposure while maintaining banking relationships in India.

What Investors Should Consider

Although the latest RBI measures may improve returns, investors should carefully review the terms offered by individual banks before investing.

The actual deposit rates available under the scheme may vary across institutions. In addition, leveraged strategies involve borrowing and therefore carry higher risks than conventional fixed deposits. Returns will depend on funding costs, interest rate movements and the structure of the investment.

Key Risks

- Leverage can magnify losses if borrowing costs increase.

- Deposit rates may vary across participating banks.

- Regulatory changes may alter programme economics.

- Foreign funding access may not be available to all investors.

Summary

RBI's latest FCNR(B) initiative is aimed at attracting foreign currency inflows by reducing hedging costs for banks and improving the attractiveness of NRI deposits. The scheme could lead to higher FCNR(B) deposit rates and, in leveraged structures, potentially generate annual dollar returns of 17-27 percent. Participation levels, borrowing costs and bank-specific offerings will determine actual investor outcomes.

FAQs

Q: What is an FCNR(B) deposit?

A: It is a foreign currency fixed deposit offered by Indian banks to eligible non-resident Indians.

Q: Why has RBI introduced the latest FCNR(B) measures?

A: The measures aim to attract foreign currency inflows and improve banking system liquidity.

Q: How can leveraged FCNR(B) structures increase returns?

A: Investors combine personal capital with borrowed funds, increasing exposure and potential returns as well as risks.