Company Overview

GK Energy Limited (NSE:GKENERGY) is an engineering, procurement and construction company whose core business is the design, supply, installation and commissioning of solar-powered agricultural water pumping systems. A typical installation replaces a diesel or electric irrigation pump in a farmer's field with a solar PV array and a matched submersible or surface pump, decoupling irrigation cost from rising fossil-fuel prices and unreliable grid power.

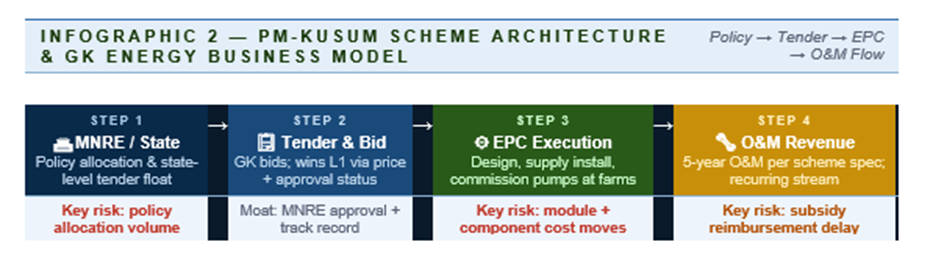

The Indian government's flagship policy vehicle for this segment is the Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan — PM-KUSUM. The scheme subsidises standalone solar pumps (Component B), solarisation of grid-connected pumps (Component C), and small decentralised solar power plants on farmer lands (Component A). GK Energy's business is most directly exposed to Component B, where state-level tenders are floated for supply and installation of standalone solar pump systems in rural areas, typically with 60% central and state subsidy and a 30–40% farmer contribution.

Operationally, the business model is a classic EPC-plus-aftermarket. GK sources solar panels, controllers, pump sets and balance-of-system from a supplier base, deploys trained installation crews to remote rural geographies, and provides multi-year operations and maintenance support per scheme specifications. Reference approvals from MNRE and individual state nodal agencies, coupled with on-ground execution capability in logistically challenging geographies, create a modest but real moat against pure trading competitors.

Financial Insights

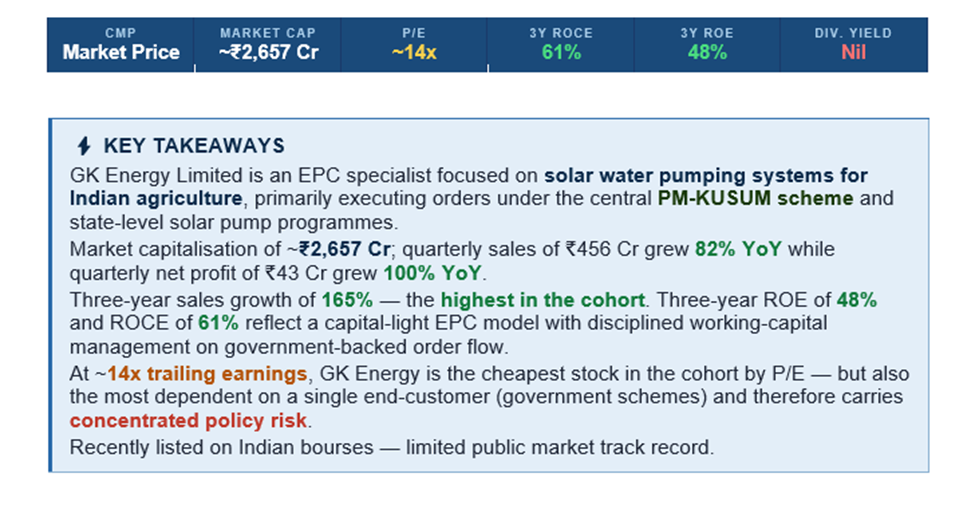

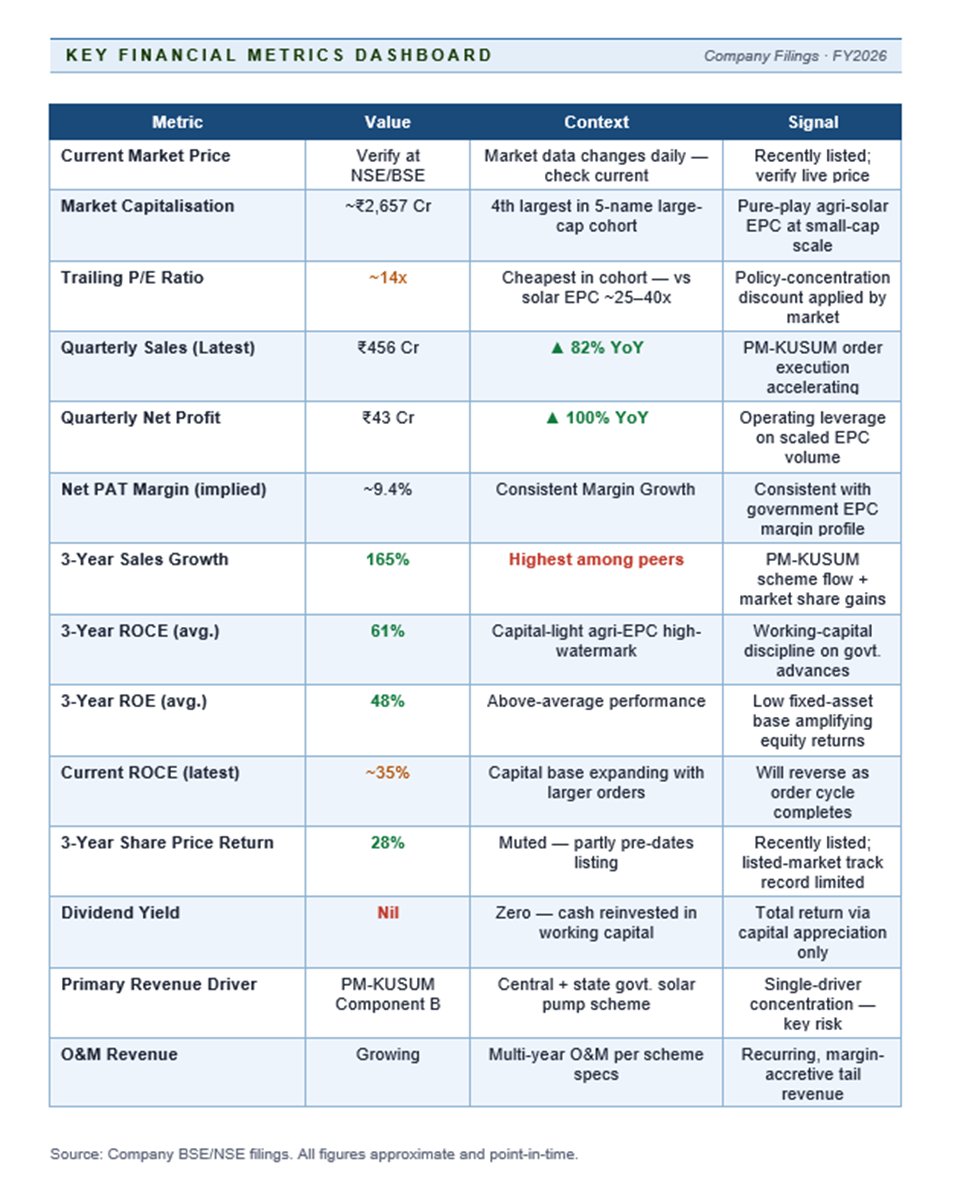

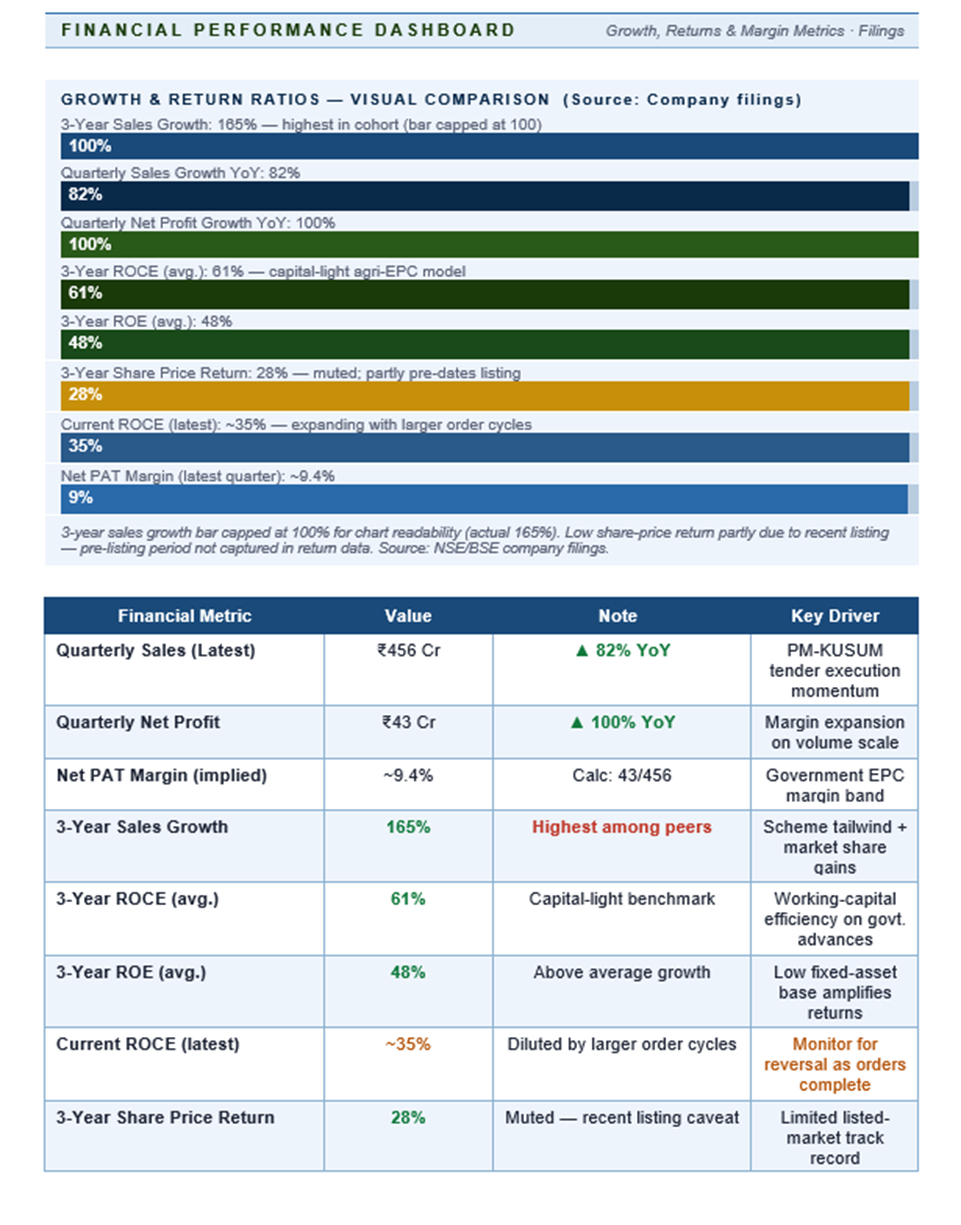

The financial trajectory captures a clean EPC scale-up. Quarterly sales of ₹456 Cr up 82% YoY, net profit of ₹43 Cr up 100% YoY, implying net margin in the 9–10% range — consistent with an EPC that captures system-supply margin, installation margin and long-tail O&M economics. Three-year sales growth of 165% is the highest in the cohort, reflecting both PM-KUSUM order flow acceleration and share gains against fragmented smaller competitors. Source: Company BSE/NSE filings.

Return ratios are exceptional: three-year ROE of 48% and ROCE of 61%. The arithmetic is characteristic of a capital-light government-EPC business where fixed assets are minimal and working capital turns quickly — subsidies flow through a defined process and, when administered properly, receivable days stay controlled.

Current ROCE at ~35% is lower than the three-year average, likely reflecting larger ticket-size orders with longer cycles as the company has scaled. Three-year share-price return of 28% is the most muted of the cohort, which is almost entirely attributable to GK Energy's relatively recent listing history — the three-year window partly predates public market pricing.

Price Performance

Since listing, GK Energy (NSE:GKENERGY) has moved roughly in step with the broader small-cap renewables sentiment, with pronounced moves on each state-level PM-KUSUM allocation and on union budget signals around scheme outlay. For investors, this creates a trading pattern where earnings releases matter less than order-book announcements and tender outcomes — a feature, not a bug, of a government-EPC business.

Dividend yield is nil; the business is reinvesting working capital into larger order execution.

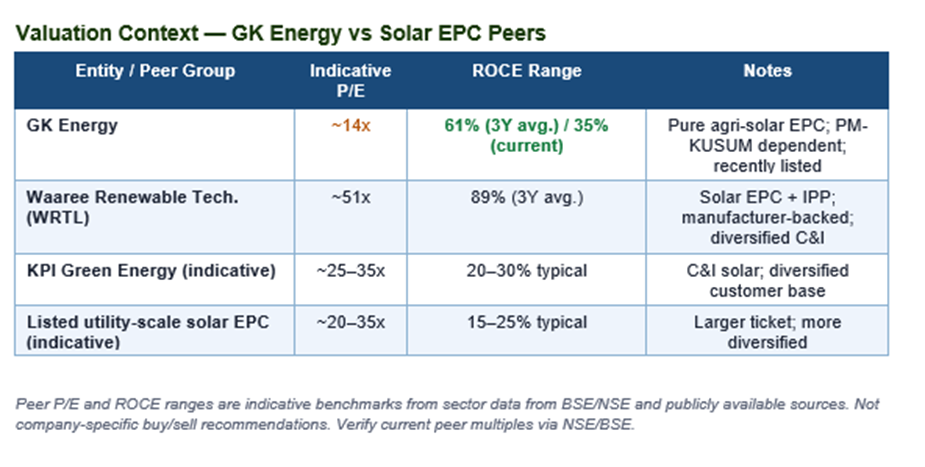

Valuation

At ~14x trailing earnings, GK Energy stands out as the most inexpensive name in the cohort on headline P/E. This discount to peers should not be misread as a mispricing — the market is simultaneously pricing in concentrated customer-scheme exposure, shorter listed history, and the risk that a policy slowdown or payment-cycle elongation could compress growth at short notice.

That said, if PM-KUSUM outlays continue at current or higher levels through the current five-year plan and execution remains clean, the forward P/E on realistic growth assumptions drops into the high single digits — a level where the stock transitions from being a policy-beta play to a compounding capital-light business. The key is to size the position with explicit acknowledgement that policy risk is the largest single variable.

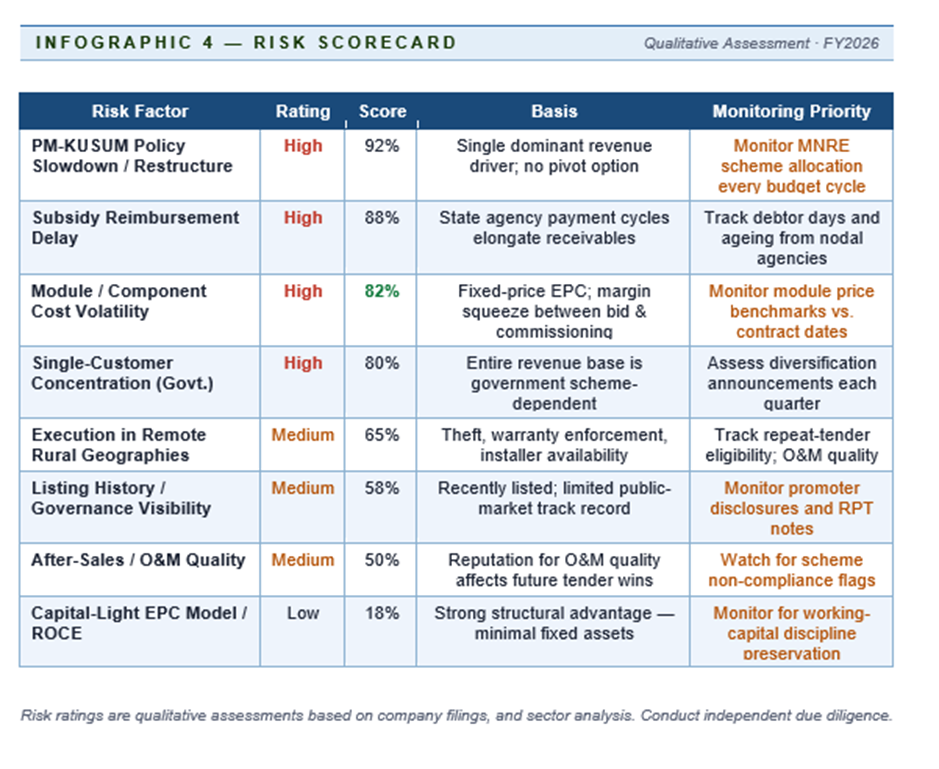

Key Risks

Risk 1 — Government Scheme Dependence

Government-scheme dependence is the dominant risk. A decision at the central or state level to slow PM-KUSUM allocation, alter the subsidy structure, or re-bid tenders at lower prices would directly compress GK Energy's revenue and margin profile. Unlike a diversified EPC with private-sector customers, GK cannot easily pivot.

Risk 2 — Payment Cycle and Subsidy Reimbursement

Even when orders are executed, release of the subsidy tranche from central and state authorities can elongate working-capital cycles. Any systemic slowdown in subsidy disbursement would pressure receivable days and ROCE. Debtor days and nodal-agency ageing schedule are the single most important monitoring metrics from a balance-sheet health perspective.

Risk 3 — Module and Component Cost Volatility

Fixed-price EPC contracts expose the company to input-cost moves between bidding and commissioning; a sharp upward move in module, controller or motor prices can compress project margin. This risk is amplified for longer-cycle orders and in periods of global supply-chain disruption.

Risk 4 — Execution and After-Sales in Rural Geographies

Installation quality, theft or damage to equipment, warranty enforcement, and contractor reliability in remote rural geographies are operational risks that rarely make the front page but can impair long-term customer relationships and repeat-tender eligibility. O&M quality is the key determinant of whether installed projects generate recurring revenue or recurring cost.

|

Investor Monitoring Checklist ① State-wise tender wins and order-book size — primary growth indicator ② Debtor days and subsidy-reimbursement timelines from state nodal agencies ③ Gross margin by state (varies with specification, component mix, geography) ④ Receivable ageing from nodal agencies — flag any elongation above 90–120 days ⑤ Any diversification announcements beyond PM-KUSUM (C&I, hybrid agri, micro-grids) ⑥ Central and state budget signals on PM-KUSUM outlay each February / state budget |

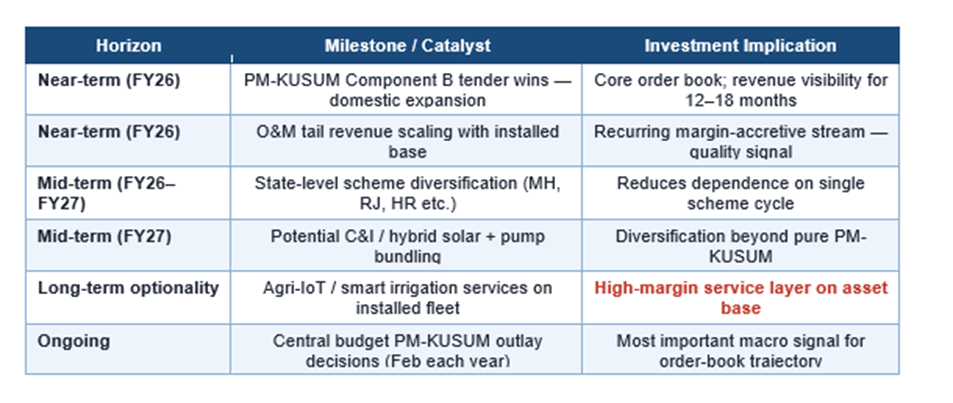

Company Outlook — FY26–FY27

India has committed meaningful resources to agricultural solarisation as part of its overall energy-transition strategy. The stated PM-KUSUM target of millions of solar pumps and solarised connections creates a long-dated pipeline in which GK Energy, as a scaled, approved vendor, is well-positioned. Parallel state-level schemes in Maharashtra, Rajasthan, Haryana and others extend the opportunity beyond the central scheme.

Longer-term, the business is a proxy for the agricultural clean-energy transition in India. Optionality exists in agri-IoT and smart irrigation services layered on top of installed pumps, and in potential expansion into decentralised solar for rural micro-enterprises. Management execution on diversification beyond PM-KUSUM will be the key signal for whether GK Energy can evolve into a broader rural clean-energy EPC.

Frequently Asked Questions

Q1. What does GK Energy do exactly?

It designs, supplies, installs and commissions solar-powered water pumping systems for Indian farmers, primarily under the PM-KUSUM scheme and comparable state programmes. It also provides multi-year O&M per scheme specifications, generating a recurring revenue tail on the growing installed base.

Q2. What is PM-KUSUM and why does it matter?

PM-KUSUM is the central government's scheme to solarise agricultural pumping and install decentralised solar generation on farm lands. It is GK Energy's dominant revenue driver. Scheme outlays and state-level tender flow therefore largely determine near-term growth — more so than general economic conditions or private-sector demand.

Q3. Why is the P/E so much lower than other solar peers?

Concentrated scheme dependence, relatively recent listing, and a more limited track record versus larger solar EPC platforms with diversified customer bases. The market applies a discount for this concentration until diversification reduces single-customer exposure.

Q4. How cyclical is the business?

Less cyclical than commodity or steel businesses but sensitive to policy cycles rather than demand cycles. Fiscal-year-end tender rushes, budget-cycle allocations and state-election-driven scheme pushes can produce lumpy quarterly prints. This makes order-book monitoring more important than quarterly revenue smoothing.

Q5. Is the stock a buy at ~14x earnings?

That depends on an investor's view of PM-KUSUM's trajectory and GK's ability to diversify. On continued strong scheme flow, the forward multiple compresses to an attractive level. On any policy pause, the stock can de-rate sharply. Position sizing should reflect this single-variable sensitivity — it is a concentrated bet on a specific policy programme.

Q6. What should investors monitor?

State-wise order book and tender win rate, debtor days and subsidy-reimbursement timelines, gross margin trends by state, any announcements of new product lines or geographies, and central/state policy changes affecting PM-KUSUM or comparable schemes.