The Shuddhi Ayurveda Chain That Quadrupled Quarterly Profit

Company Overview

Jeena Sikho Lifecare Limited (NSE:JSLL) is the operating company behind Shuddhi Ayurveda — one of India's fastest-scaling branded chains of Ayurvedic wellness clinics and multi-speciality Ayurvedic hospitals. The business has its roots in the health platform built around Acharya Manish, whose video content and public programming on lifestyle-led disease reversal grew into a substantial consumer following. That audience has been channelled into paying customers at physical clinics and hospitals, giving JSLL a zero-cost-of-acquisition top-of-funnel that most traditional healthcare chains cannot replicate.

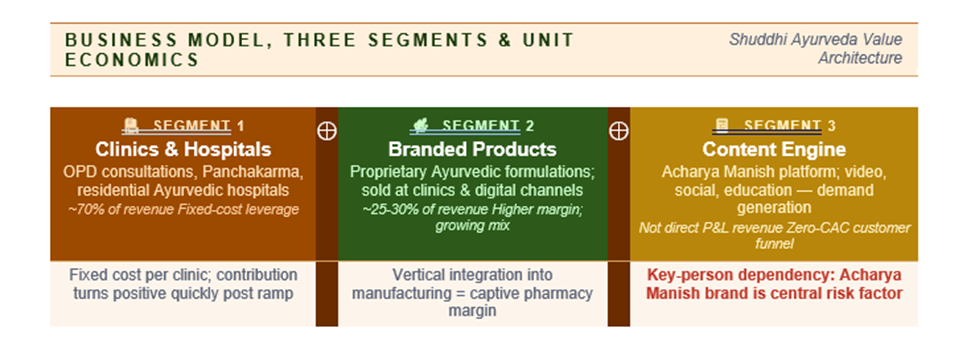

Operationally, the company runs in three interconnected segments:

- Clinic and Hospital Network: Shuddhi-branded outpatient consultation centres and larger multi-bed residential hospitals offering Panchakarma, diet-and-lifestyle protocols, and Ayurvedic treatments for chronic conditions such as diabetes, thyroid disorders, obesity, joint pain and hypertension.

- Product Portfolio: Proprietary Ayurvedic formulations and wellness products sold to patients at clinics and increasingly through digital and retail channels.

- Content and Education Engine: Not a direct revenue contributor at scale, but the demand-generation flywheel that makes the unit economics of the clinics work — social media, video content and wellness education driving inbound patient enquiries.

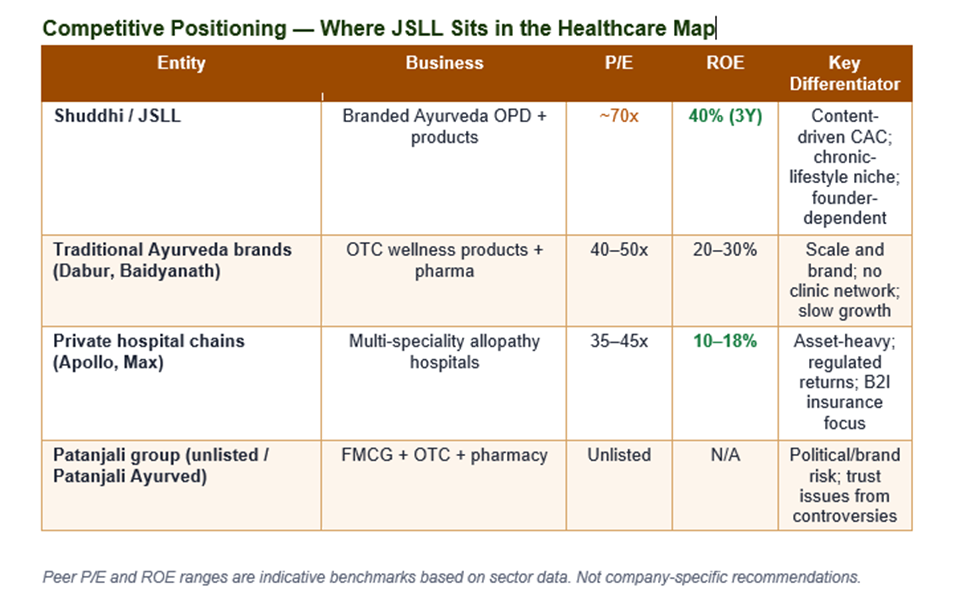

Strategically, the model combines brand marketing, franchise-plus-owned physical distribution, and vertical integration into Ayurvedic manufacturing. This positions JSLL in a different competitive space from both traditional Ayurveda brands (Baidyanath, Dabur, Patanjali) and private hospital chains; the business is closer in shape to a specialty outpatient chain with captive pharmacy attached.

Financial Insights

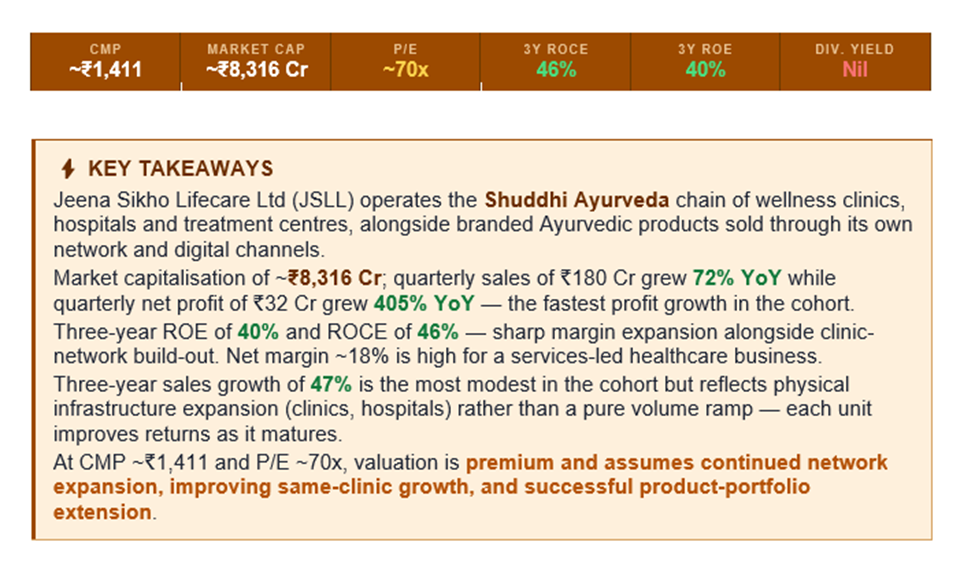

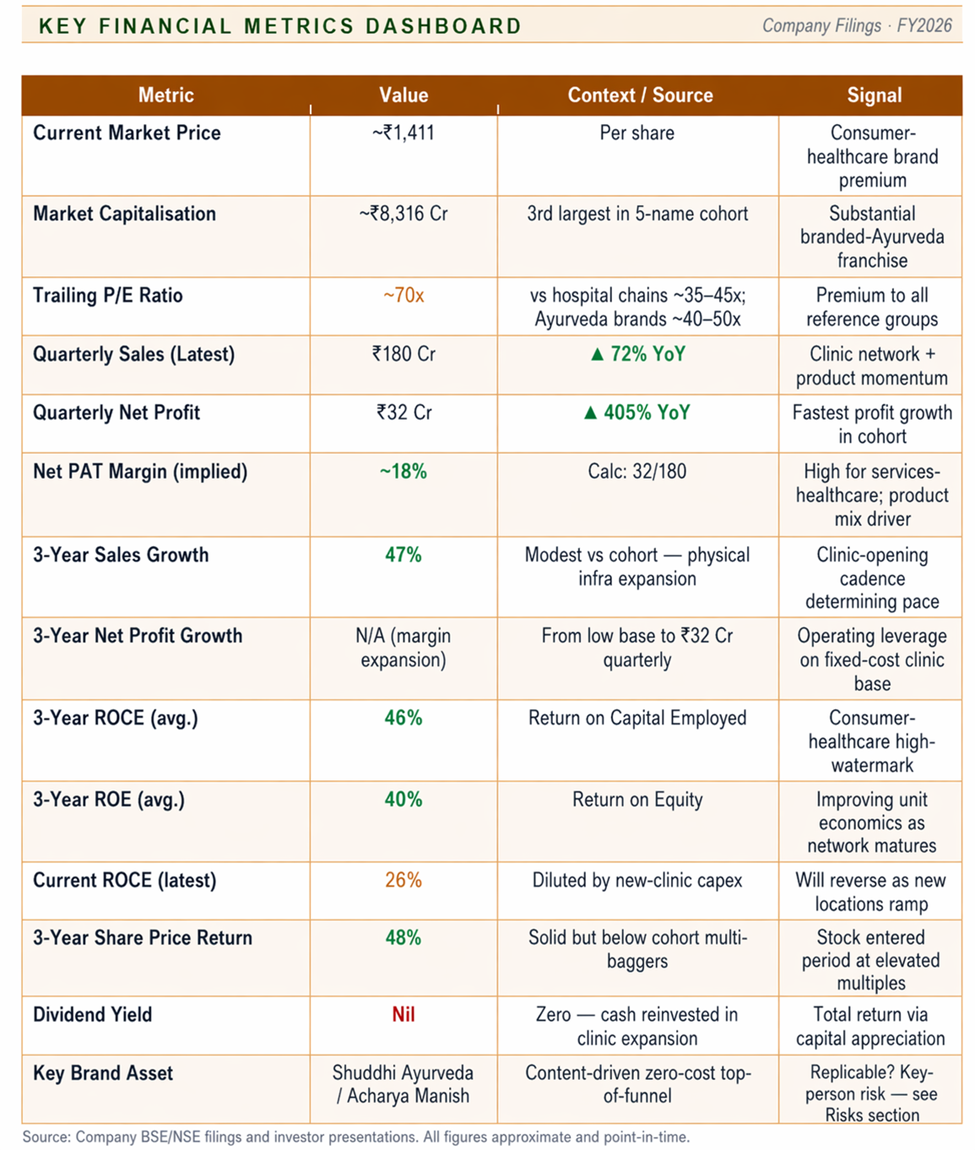

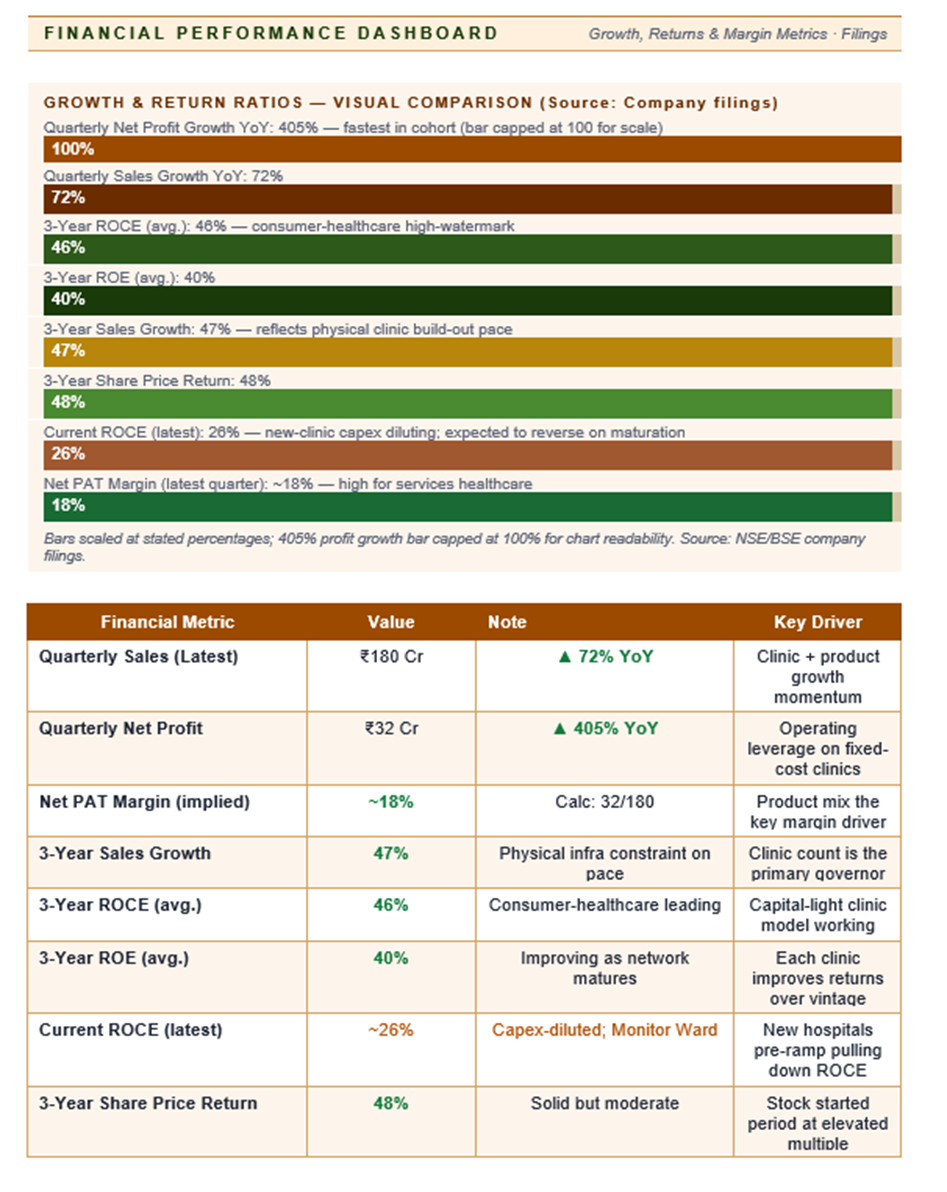

The quarterly print shows meaningful operating leverage. Revenue of ₹180 Cr was up 72% YoY while net profit of ₹32 Cr was up 405%, translating into a net margin of ~18% — high for a services-led healthcare business and a signal that the product and pharmacy trailing the consultation drives outsized incremental profitability. Source: Company BSE/NSE filings.

Across three years, sales growth of 47% looks modest versus the three-digit growth of some cohort peers, but this has to be read alongside the fact that JSLL is growing physical infrastructure — opening clinics and hospitals — rather than a purely commodity volume ramp. Three-year ROE of 40% and ROCE of 46% indicate the model is not merely scaling revenue but doing so with strong capital efficiency: each new clinic reaches contribution-positive status relatively quickly given the pre-existing brand pull.

Current ROCE at 26% is lower than the three-year average, which mathematically tracks the build-out of new hospitals that carry capex and working capital before they fully ramp. Historically, such dips have reversed as the new locations mature into their earnings run-rate.

Price Performance

Over three years, JSLL has delivered a share-price return of 48%— solid but less dramatic than some of its cohort peers. This reflects the fact that the stock already entered the period at elevated multiples and has re-rated somewhat more through earnings growth than through multiple expansion.

The stock has also seen episodes of volatility tied to governance questions, promoter pledge disclosures, and related-party-transaction discussion typical of founder-led consumer-healthcare companies at this stage of growth. Dividend yield is nil — all cash is being reinvested into network expansion.

Valuation

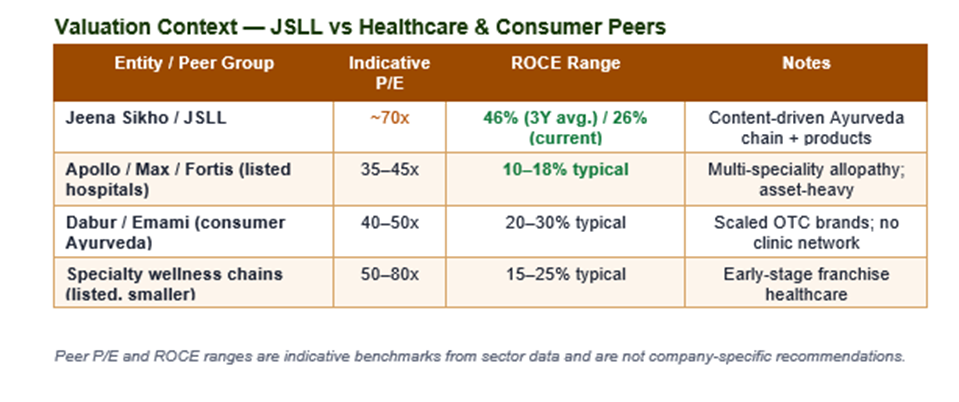

At ~70x trailing earnings, the market is pricing JSLL as a long-runway consumer-healthcare brand rather than a services business. For context, listed hospital chains like Apollo, Max, or Fortis typically trade at mid-30s to mid-40s P/E, while scaled consumer-Ayurveda brands like Dabur or Emami change hands in the 40s–50s. The JSLL multiple is therefore ahead of both reference points.

The implicit argument is that the content-driven customer acquisition model creates a brand moat that justifies valuation somewhere between a franchise consumer brand and a specialty hospital chain, while the chronic-lifestyle-disease addressable market is large and under-penetrated by organised Ayurveda. For investors, the key discipline is to size the position assuming multiple compression on any earnings hiccup.

Key Risks

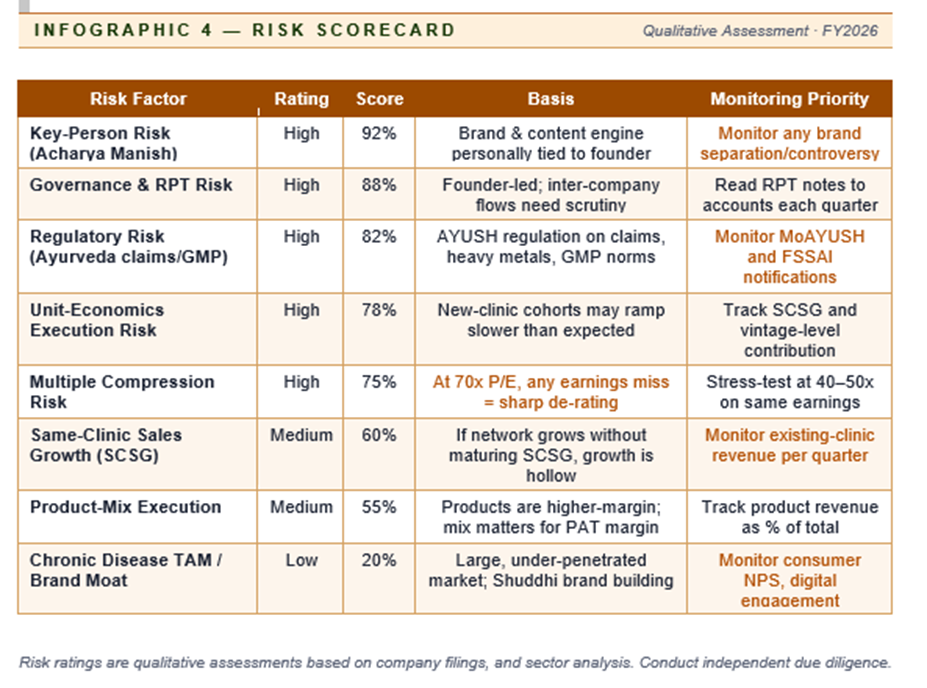

Risk 1 — Key-Person Dependency

Key-person risk is the first and most discussed. The Shuddhi brand and its content engine are closely tied to Acharya Manish personally; any event that impairs that association — health, controversy, or loss of focus — would materially affect customer pull. Companies built on individual brand equity typically trade at a valuation discount for exactly this reason, and JSLL's current multiple of ~70x leaves little cushion.

Risk 2 — Governance and Related-Party Transactions

In founder-led chains, the lines between promoter-owned content platforms, promoter-owned product brands, and the listed operating company need careful scrutiny. Investors should read notes to accounts for RPTs, revenue concentration, and any unusual inter-company flows each quarter. This is a standard governance screen for consumer-healthcare companies at this stage but is elevated in salience given the promoter-content-clinic structure of JSLL.

Risk 3 — Regulatory Environment for Ayurveda

Ayurveda medicine regulation in India has seen periodic tightening — around claim substantiation, heavy-metal testing, GMP norms and marketing standards under MoAYUSH, FSSAI, and state-level drug regulation. Any adverse regulatory turn, or public-health controversy attaching to herbal formulations, would pressure margins and brand perception across the industry.

Risk 4 — Unit-Economics and Clinic Network Execution

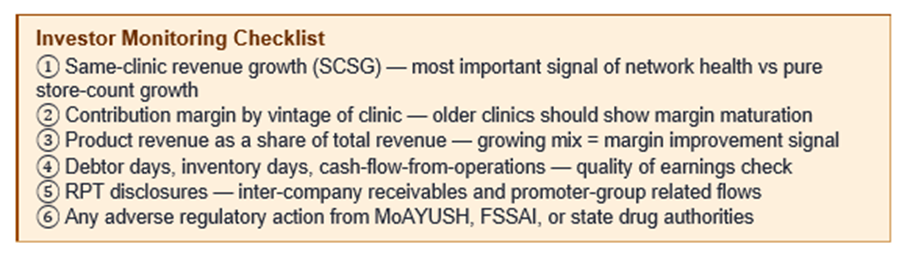

Scaling a clinic network requires disciplined real-estate selection, clinician hiring, and standardisation of treatment protocols. Slippage on any of these — for example, a new-clinic cohort that ramps more slowly than expected — would show up in compressed ROCE before it becomes obvious in top-line trends. Same-clinic sales growth (SCSG) is the metric investors should demand as the most reliable indicator of whether the network is genuinely healthy.

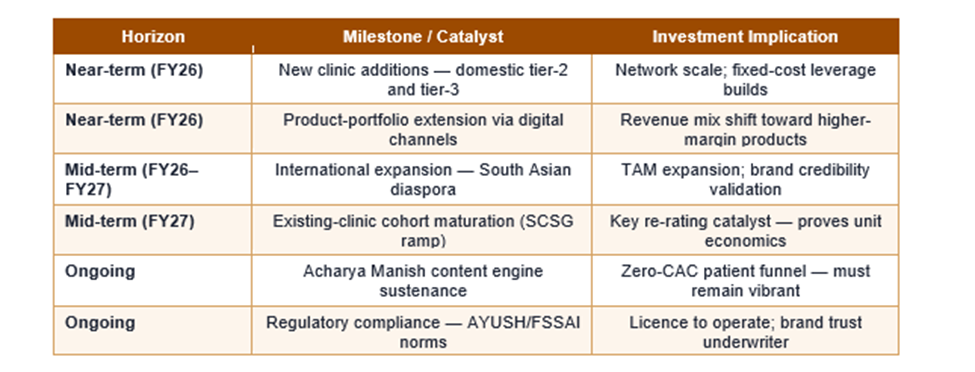

Company Outlook — FY26–FY27

The consumer backdrop for Ayurveda and lifestyle-led healthcare in India is robust. Rising chronic-disease burden, disenchantment with long-term chemical medication for non-acute conditions, and a growing willingness-to-pay for preventive and wellness care combine to expand JSLL's addressable market. Organised penetration of Ayurvedic outpatient care remains low, which leaves significant white space for a branded, standardised chain.

Management commentary and expansion plans point to continued addition of clinics and hospitals, deeper penetration into tier-2 and tier-3 cities, and selective international expansion targeting the South Asian diaspora. Parallel to this, the products business is being extended through digital commerce channels, which should improve mix and margin over time.

Frequently Asked Questions

Q1. What is Shuddhi Ayurveda and how is it connected to Jeena Sikho?

Shuddhi is the consumer brand under which Jeena Sikho Lifecare operates its chain of Ayurvedic clinics and hospitals. JSLL is the listed operating company; Shuddhi is its public-facing brand. The two are the same entity from an investor perspective.

Q2. How does the company acquire customers?

Predominantly through a large content-and-education engine built around its founder Acharya Manish and partners. This drives inbound enquiries and appointments into the clinic network, effectively making customer acquisition cost lower than in a traditional hospital chain — a key unit-economics differentiator.

Q3. Why is profit growth so much faster than revenue growth?

Operating leverage on a fixed-cost clinic network plus an expanding mix of higher-margin Ayurvedic products sold alongside consultations. As new clinics mature and the product attach rate grows, incremental revenue flows disproportionately to profit. The 405% YoY profit growth on 72% revenue growth is a direct expression of this dynamic.

Q4. What should investors worry about the most?

Key-person dependency (brand tied to Acharya Manish personally), governance and RPT hygiene (read notes to accounts each quarter), and regulatory risk around Ayurveda marketing and product claims. Each of these has the potential to significantly impact valuation even if unit economics themselves remain healthy.

Q5. How to read quarterly results?

Look past the headline growth into disclosures on clinic count, same-clinic sales growth (SCSG), contribution margin, RPTs and cash-flow-from-operations. A company growing revenue but not CFO, or growing new clinics without maturing existing ones, should raise questions. Company filings are the primary data sources to cross-check.