Pit-to-Plate Iron Ore & Steel Play With 113% Three-Year Sales Growth

Source: Investors presentations. All figures approximate

Company Overview

Lloyds Metals & Energy Limited (NSE:LLOYDSME) is an integrated iron ore and sponge iron company headquartered in Mumbai and promoted by the Gupta family of the Lloyds Group. The company traces its origins to the early 1990s as a sponge iron producer, but its modern story began with the acquisition and operationalisation of the Surjagarh iron ore mine in Gadchiroli district of Maharashtra — a deposit that had lain substantially under-exploited for decades due to its location in a Left-Wing-Extremism-affected zone.

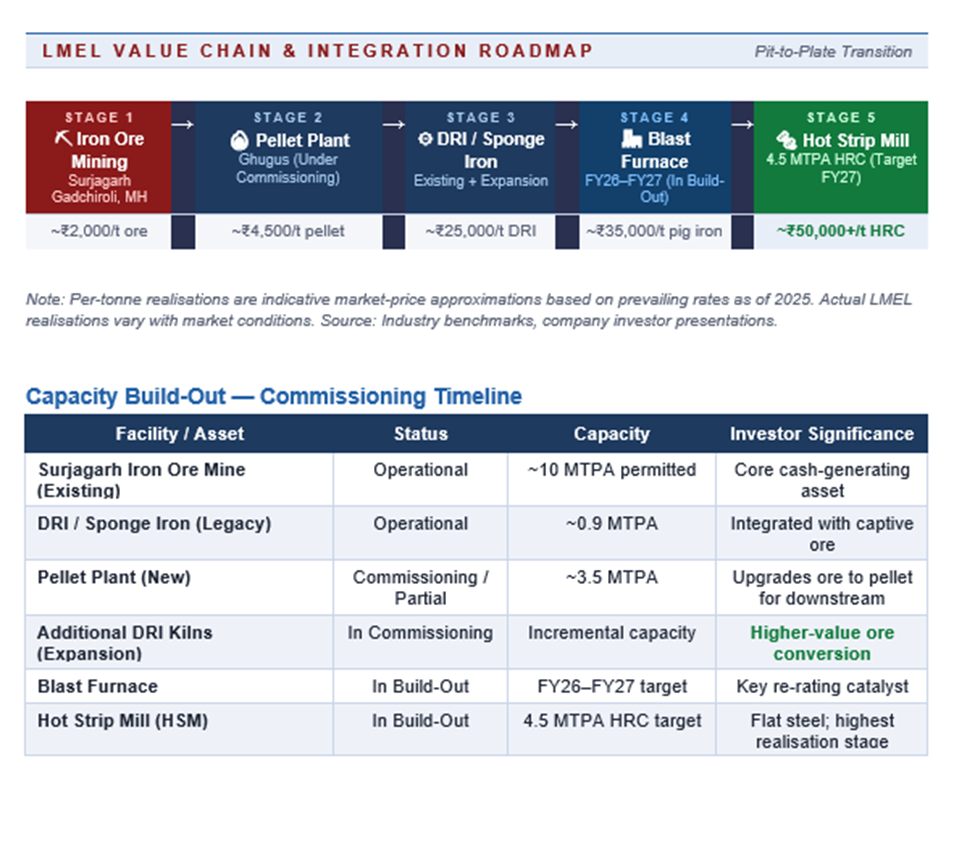

The business today rests on three pillars:

- Merchant Iron Ore Business: Ships run-of-mine and beneficiated ore from Surjagarh to domestic steel mills and pellet plants.

- Legacy DRI (Sponge Iron) Plant (Ghugus, Chandrapur): Converts part of the captive ore into sponge iron sold to induction-furnace-based secondary steelmakers.

- Greenfield Integrated Steel Complex (Ghugus): A pellet plant, additional DRI kilns, blast furnace, and hot strip mill being added to take the group into flat steel products — this is where the growth story is concentrated.

Strategically, this is a textbook backward-forward integration play. Captive ore at near-mining cost converts what is ordinarily a commodity-margin business into one capable of sustaining through-cycle EBITDA margins well above the industry mean. Once the HSM is commissioned, each tonne of ore mined at Surjagarh can theoretically be upgraded all the way to hot-rolled coil inside the LMEL perimeter, capturing value at every stage instead of selling at the first sellable point.

Financial Insights

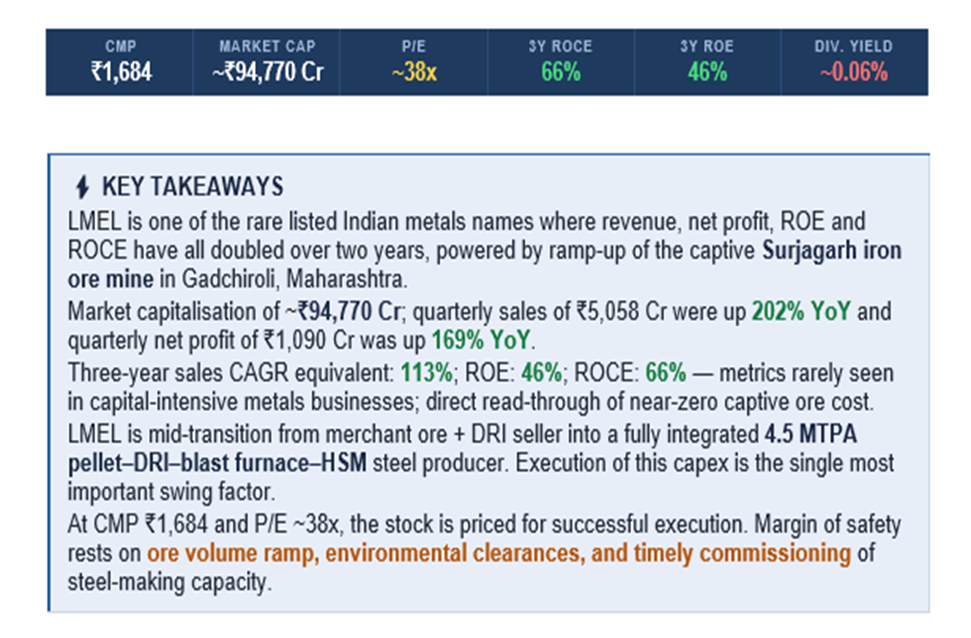

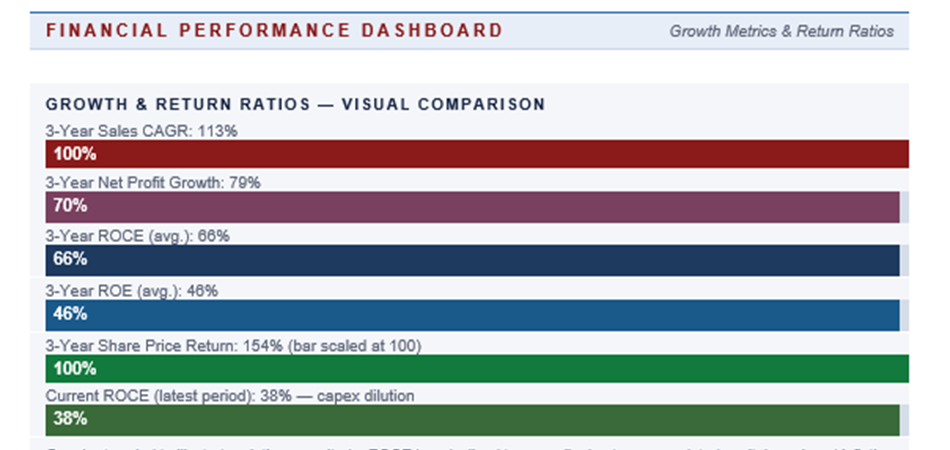

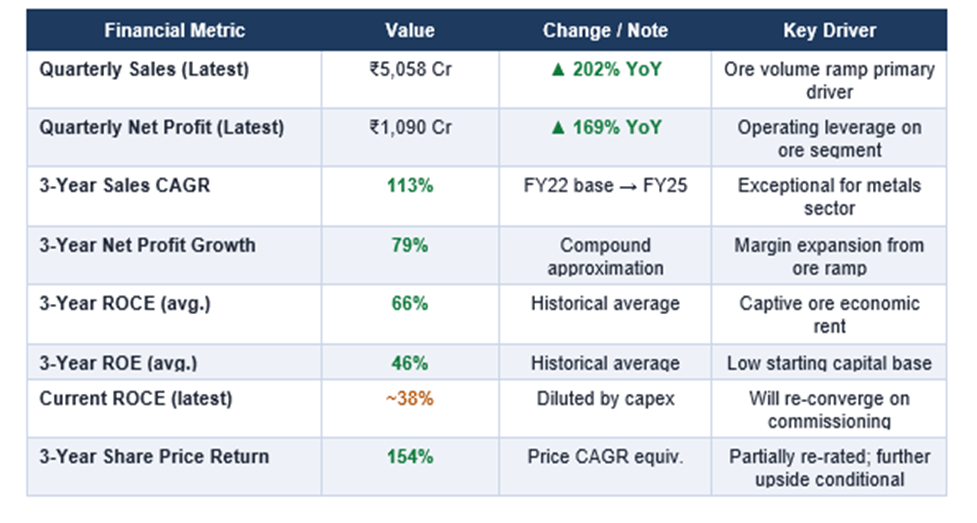

The operational inflection is visible in every line of the quarterly print. Sales of ₹5,058 Cr in the most recent quarter represent a 202% jump year-on-year, and net profit of ₹1,090 Cr is up 169%. Over a three-year frame, sales have compounded at 113%, net profit growth at 79%, and share-price return at 154% — the operational growth has been faster than the stock price in percentage terms, even though absolute market cap is now substantial.

The return ratios are where LMEL genuinely separates from the metals pack. A three-year ROCE of 66% and ROE of 46% are closer to a software or consumer business than to a mining-and-steel company. The explanation is economic rent on captive ore: when the marginal cost of mining ore is a fraction of the market selling price, every incremental tonne carries operating margins of 60%+ straight through to EBITDA.

The reported ROCE of 38% in the latest period is lower than the three-year average, which is a deliberate outcome of heavy capex for the steel complex inflating the capital-employed denominator ahead of the earnings from new capacity. Once the integrated plant stabilises at design utilisation, ROCE is expected to re-converge upward.

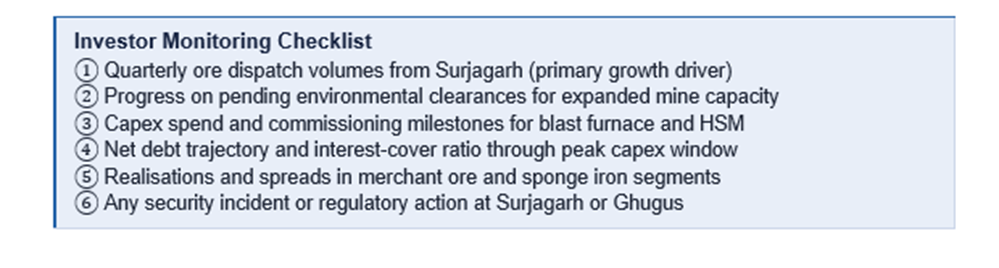

On the balance sheet, LMEL has historically been lightly leveraged and has used internal accruals plus modest borrowings to fund the steel expansion. The combination of high cash generation from the ore business and a measured debt draw has kept interest cover comfortable through the capex cycle. Investors should watch net debt and interest cost line items each quarter as the blast furnace draws closer to commissioning.

Price Performance

LMEL has been one of the standout multi-baggers of the post-COVID cycle on Indian bourses. The three-year share-price return of 154% captured in the screener is only a fragment of the longer run-up from sub-₹50 levels several years ago to current levels near ₹1,684. Over the last twelve months, the stock has traded in a wide band as the market has oscillated between rewarding ore-volume upgrades and de-rating on regulatory-risk headlines.

Dividend yield is negligible at ~0.06%, reflecting the company's choice to retain cash for capex rather than return it. For shareholders, total return is therefore almost entirely a function of capital appreciation driven by earnings growth and re-rating.

Valuation

At ~38x trailing earnings, LMEL is not priced like a pure-play metals stock. For comparison, large integrated producers such as Tata Steel and JSW Steel typically trade in the low-to-mid teens through-cycle and compress further when steel spreads are tight. The premium LMEL commands is the market's implicit net-present-value of the incremental earnings expected once the steel complex fully commissions, at margins supported by captive ore.

Two framing questions are useful for valuation:

- Forward view: If the 4.5 MTPA complex delivers mid-teens EBITDA margins at full utilisation, the implied forward multiple compresses meaningfully, and the current price starts to look defensible rather than exuberant.

- Downside view: If execution slips by 12–18 months, the stock is exposed to de-rating toward ore-company multiples in the interim, which are materially lower. The asymmetry today favours investors with patient capital and conviction on execution.

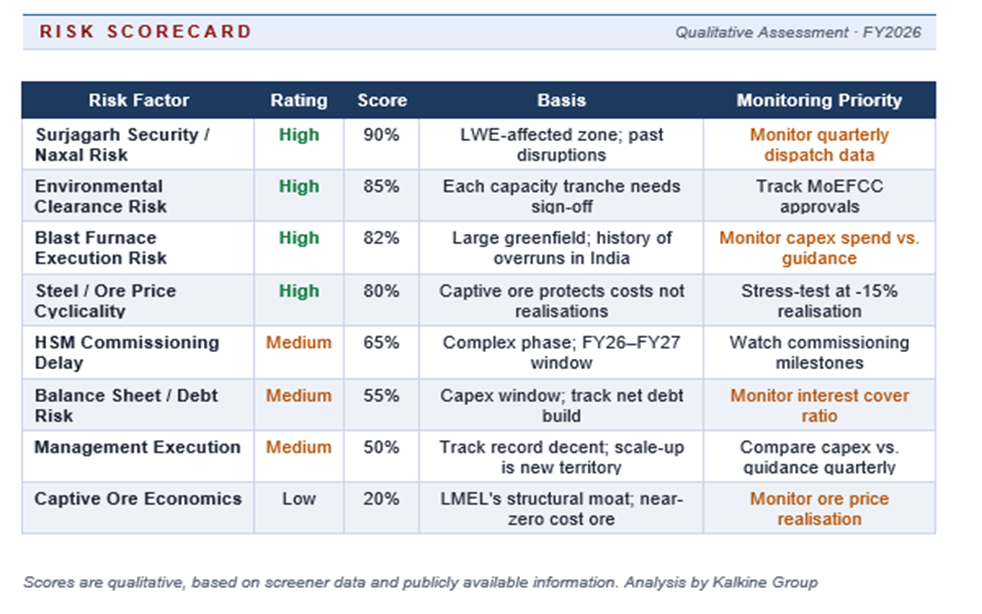

Key Risks

Risk 1 — Regulatory and Security at Surjagarh

The mine sits in a Naxal-influenced region, and the company has in the past faced temporary disruptions to mining, transport, and contractor operations. Any prolonged stoppage hits the cash-cow that is funding the steel capex. Related to this is ongoing dependence on environmental and forest clearances for expanded mine capacity; each tranche of permitted throughput requires regulatory sign-off.

Risk 2 — Execution on the Integrated Steel Complex

Large greenfield steel projects in India have a chequered history of cost overruns and timeline slippage. LMEL's management has so far tracked guidance reasonably well, but the blast-furnace-plus-HSM phase is the most complex. Any delay compresses the returns window, and cost overruns dilute the per-tonne economics that underpin the bull case.

Risk 3 — Iron Ore and Steel Price Cyclicality

Captive ore protects the cost side but does not immunise realisations. A sharp fall in domestic or global ore prices compresses the merchant-ore segment directly, while weak steel spreads would cap returns from the new capacity once commissioned. Investors should stress-test their models against a scenario of normalised ore prices and 10–15% lower steel realisations.

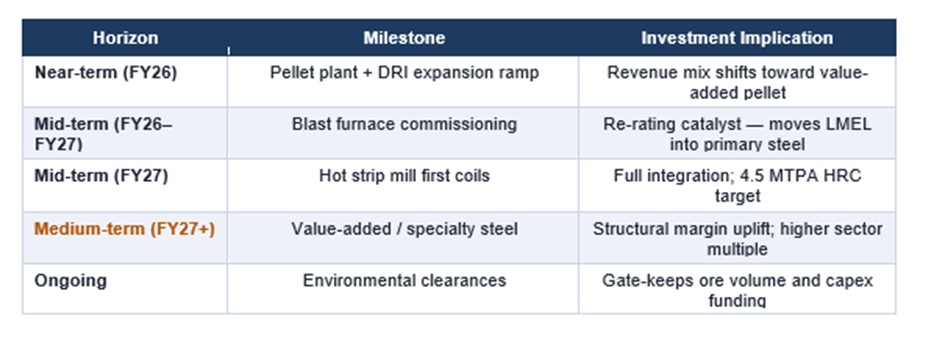

Company Outlook — FY26–FY27

The medium-term outlook is constructive if execution holds. Publicly disclosed capacity milestones point to progressive commissioning of the pellet plant and additional DRI capacity in the near term, with the blast furnace and hot strip mill tracking for completion over FY26–FY27. Successful ramp-up would shift revenue mix from lower-realisation ore and sponge iron toward higher-realisation flat steel products, defending return ratios even as ore prices normalise.

Parallel to the capacity build-out, management has indicated interest in pushing further along the value chain into specialty and value-added steel grades — a natural next step once the flat steel line stabilises. Such a shift, if executed, would further insulate margins from pure commodity cyclicality and support a structurally higher multiple than the sector average.

Frequently Asked Questions

Q1. What does Lloyds Metals & Energy actually do?

LMEL mines iron ore at Surjagarh in Maharashtra, operates a sponge iron (DRI) plant at Ghugus, and is building an integrated steel complex that will include pellet, DRI, blast furnace, and hot strip mill capacity. The model is to move progressively down the value chain from iron ore to finished flat steel using captive ore.

Q2. Why are LMEL's ROE and ROCE so high compared to other metals companies?

The captive Surjagarh mine produces ore at a very low cash cost relative to market prices. This structural advantage flows directly into higher EBITDA margins and, combined with a relatively asset-light starting capital base, translates into three-year ROE of 46% and ROCE of 66% — well above integrated-producer averages.

Q3. Is LMEL a pure mining play or a steel company?

Today it is closer to a mining-plus-DRI company, but by FY27 the mix is intended to shift materially toward integrated steel as the blast furnace and HSM ramp up. The investment thesis is essentially a bet on that transition completing on schedule and at targeted economics.

Q4. What are the most important numbers to track each quarter?

Ore dispatch volumes from Surjagarh, capex spend and commissioning milestones, EBITDA margin on the ore segment, net debt and interest cost, and progress updates on pending environmental clearances for expanded mine capacity.

Q5. Is the stock cheap at current levels?

On trailing earnings at ~38x it is not cheap relative to integrated steel peers. However, trailing earnings do not yet reflect the full contribution of the new steel complex. On a forward view that credits the ramp-up, the multiple compresses substantially. The cheapness or otherwise of the stock depends entirely on conviction in execution.

Q6. What would make the bull case break?

A prolonged disruption at the Surjagarh mine, a material slippage or cost overrun on the blast furnace project, or a sharp and sustained downturn in ore and steel prices coinciding with peak capex — any of these, individually or in combination, would challenge the thesis.