Company Overview

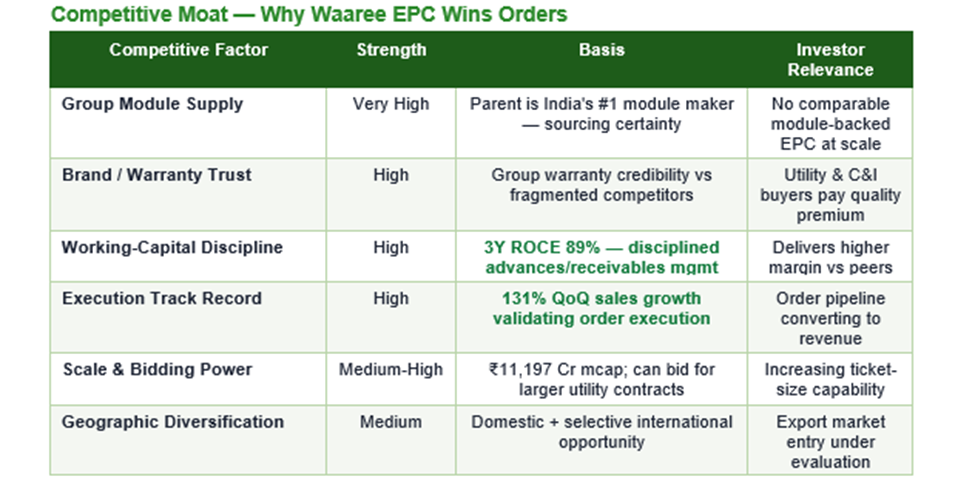

Waaree Renewable Technologies Limited, listed under the ticker (NSE:WAAREERTL), is a subsidiary of the Waaree group — a privately-held but publicly-listed conglomerate headquartered in Mumbai that has grown into India's largest solar photovoltaic module manufacturer by installed capacity. While the parent Waaree Energies is focused on module manufacturing and its recent IPO has put it firmly on the public radar, WRTL plays a different and complementary role inside the group: it is the downstream engineering, procurement and construction (EPC) and power-asset arm.

In practical terms, WRTL executes turnkey solar power projects for commercial, industrial and utility clients — handling design, land and statutory clearances, procurement (often of group-made modules), construction, commissioning and long-term operations and maintenance. It also selectively owns and operates solar plants, generating merchant or PPA-based power income.

The company therefore benefits from two tailwinds at once: the volume tailwind in Indian solar capacity addition, and the group synergy of sourcing modules from its own parent at scale and on reliable schedule. The Waaree group brand has become a meaningful advantage. In a market where solar EPC is otherwise fragmented, backed-by-a-manufacturer EPC offers customers confidence on module authenticity, warranty enforceability, and installation quality. That trust dividend shows up in WRTL's ability to secure large-ticket orders from utilities, state discoms, and commercial & industrial buyers.

Financial Insights

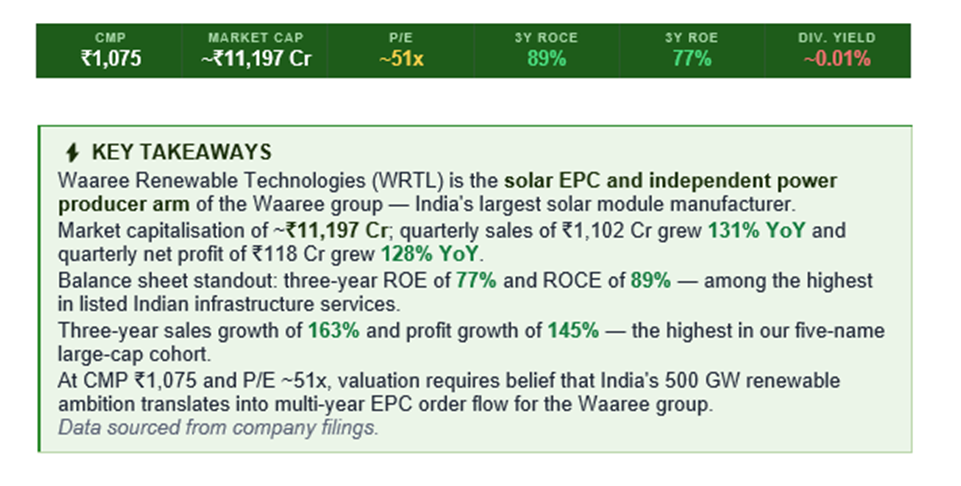

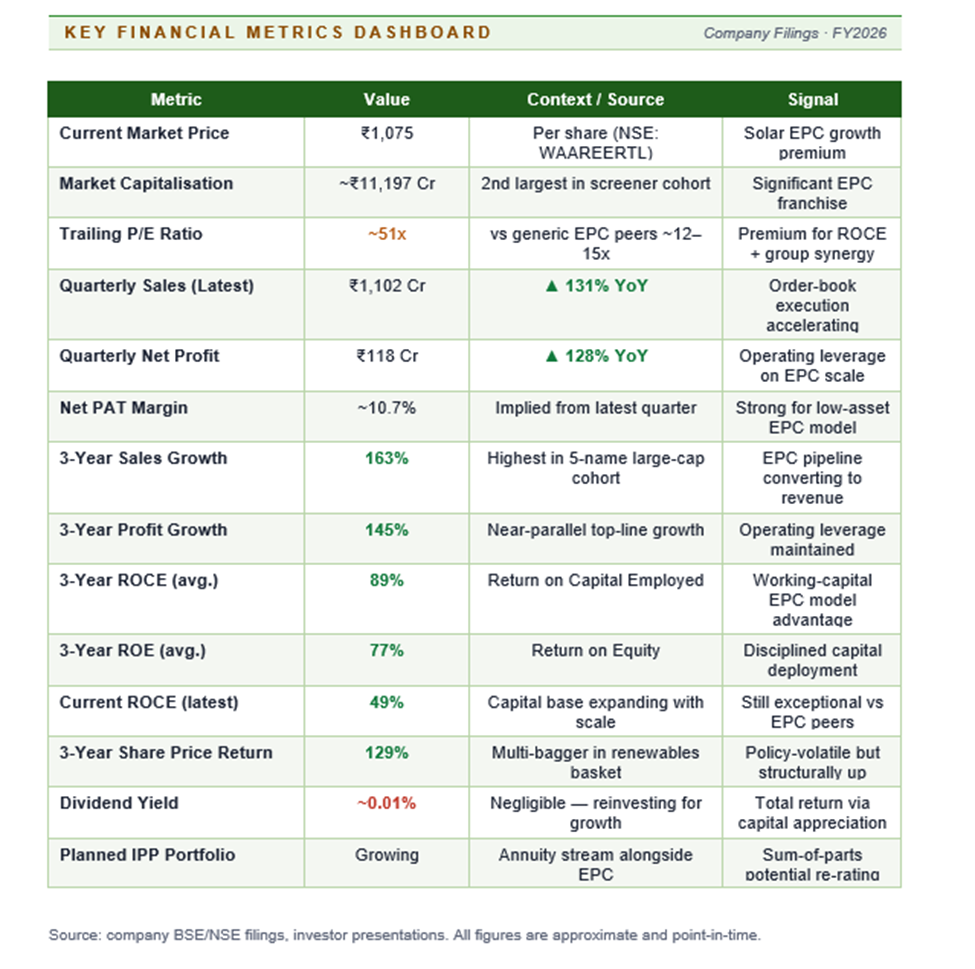

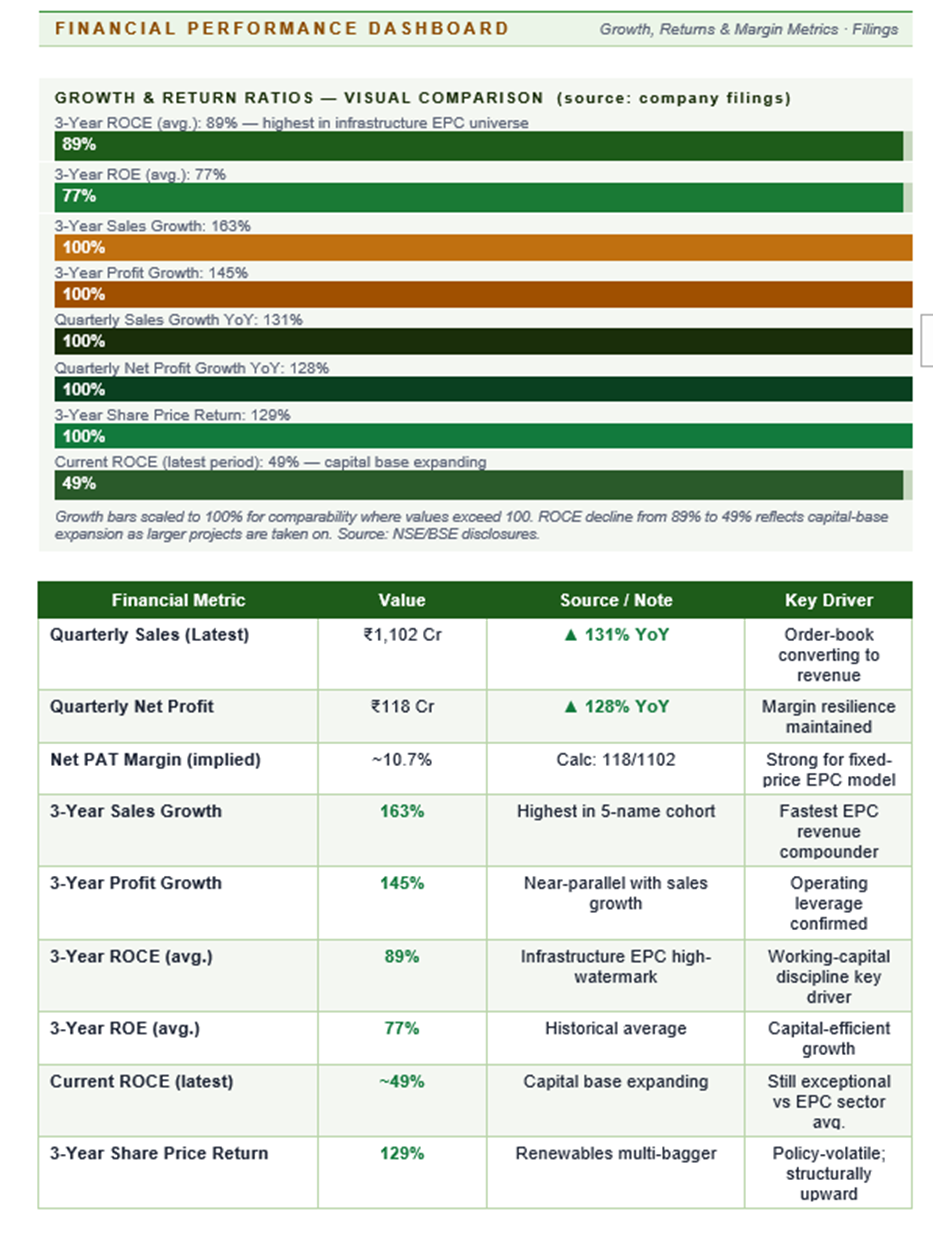

The reported numbers tell a compounder story. Quarterly sales of ₹1,102 Cr translate into an annualised run-rate well north of ₹4,000 Cr — several multiples of the base from three years ago. Net profit of ₹118 Cr in the quarter, up 128% YoY, implies net margins in the 10–11% range, which is strong for a low-asset-intensity EPC business, but consistent with an EPC outfit that captures both execution margin and the pull-through on group-sourced modules.

Return ratios are the marquee metric. Three-year ROE of 77% and ROCE of 89% position WRTL in a different league from traditional construction or capital goods peers. The mathematics is straightforward: EPC is a working-capital-driven business with low fixed assets, and the company has managed its advances and receivables cycle tightly while running high asset turnover.

Current ROCE at 49% is lower than the three-year average but still exceptional, and reflects some expansion in the capital base as the company has taken on larger projects with longer cash cycles. The three-year sales growth of 163% is the highest among the cohort of five large-caps, underscoring how quickly the Indian renewable-EPC pipeline has translated into realised revenue for a scaled, credible player.

Profit growth of 145% over the same window indicates that operating leverage and improved mix have largely kept pace with top-line growth — a non-trivial outcome in a business where mispricing a fixed-price EPC contract can quickly erode margins. Source: company BSE/NSE filings.

Price Performance

WRTL has been a prominent multi-bagger in the renewables basket over the past three years, with share-price return of 129% captured in data. The stock has also been among the more volatile in the basket, with sharp drawdowns whenever policy signals around anti-dumping duty, safeguard duty, BCD on modules, or ALMM norms have shifted. Investors should expect continued volatility as global module prices and Indian solar tariffs fluctuate.

Dividend payout is minimal at ~0.01% yield — as expected for a growth-mode EPC that reinvests cash into working capital for a larger order book.

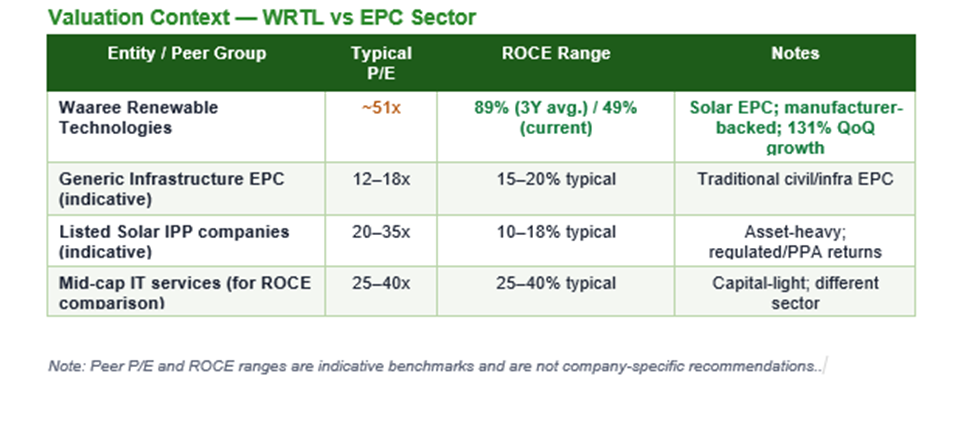

Valuation

At ~51x trailing earnings, WRTL trades at a substantial premium to traditional EPC contractors, which typically change hands in the mid-teens. The premium is best understood as a blend of three factors: superior return ratios (ROCE near 50% versus 15–20% for generic EPC), sector tailwind (India 500 GW renewable ambition), and group vertical integration on modules.

The bull case on valuation argues that forward earnings will compress the multiple quickly as the order book executes, and that India's 500 GW non-fossil capacity target by 2030 is a multi-decade TAM that supports sustained high-teens growth.

The bear case points out that EPC margins historically compress as competition scales, that module-price deflation can cut EPC ticket sizes even as megawatt volumes grow, and that any slowdown in auctions or PPA awards can create sudden order-book gaps.

Key Risks

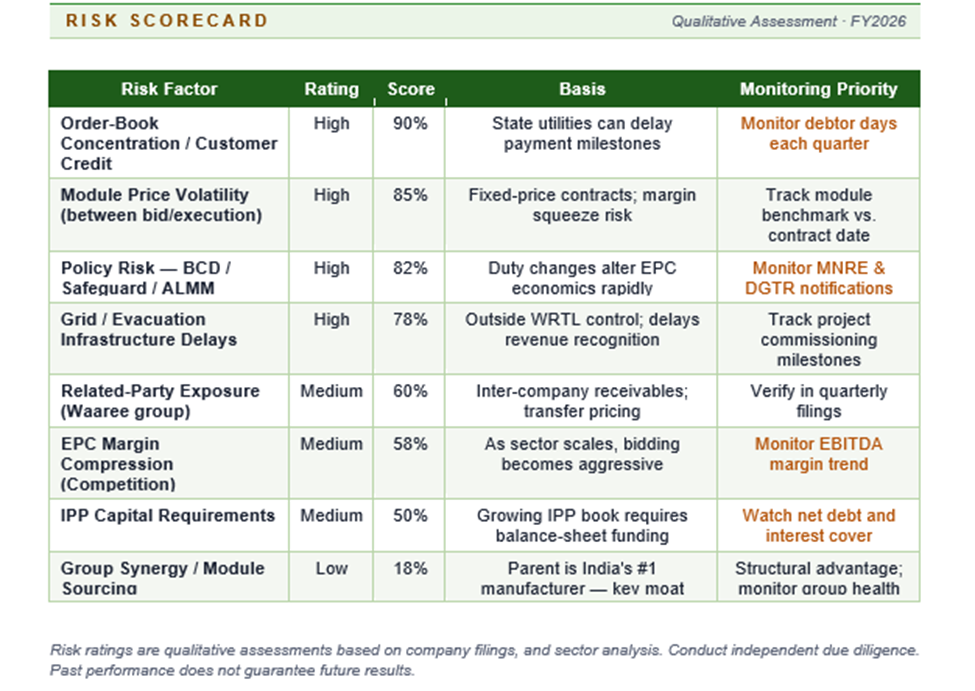

Risk 1 — Order-Book Concentration and Customer Credit

Order-book concentration and customer credit risk sit at the top of the risk list. Solar EPC involves material advances of working capital and payment milestones tied to project stages; any slip in payments from a state utility or a commercial-industrial customer can quickly impair receivable quality and working-capital returns. Debtor days is the single most important quarterly monitoring metric.

Risk 2 — Module Price Volatility

Module price volatility is the second risk. While group sourcing offers reliability, EPC contracts are often priced against prevailing module benchmarks; sudden movements between bidding and execution can compress gross margins. Policy changes — safeguard duty, anti-dumping duty, BCD, ALMM approved-list dynamics — can amplify this risk either way.

Risk 3 — Execution and Land/Grid Delays

Execution and land-related delays are endemic to Indian solar. Right-of-way, evacuation infrastructure, substation readiness, and grid connectivity all sit outside WRTL's direct control but can delay commissioning, revenue recognition, and cash release.

Risk 4 — Related-Party Exposure Within Waaree Group

WRTL is a related-party-heavy business within the Waaree group ecosystem. While synergies are real and disclosed, investors should stay attentive to transfer pricing, inter-company receivables, and any reorganisation decisions at the group level. These are disclosed in quarterly and annual filings and should be reviewed with each reporting period.

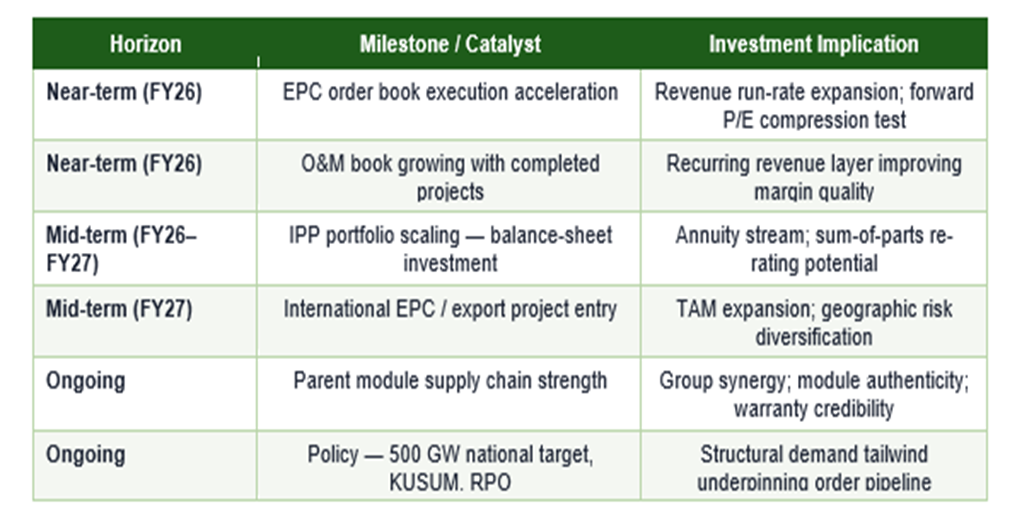

Company Outlook — FY26–FY27

The demand backdrop for WRTL is arguably the most favourable among the five companies in this analysis. India's stated ambition of 500 GW of non-fossil capacity by 2030, of which solar is the dominant component, creates a multi-year addressable market measured in the hundreds of gigawatts of new build. Within this, EPC captures roughly 15–20% of project cost, and players with credible manufacturer backing are positioned to take disproportionate share.

Management signals and group strategy suggest continued expansion both domestically and selectively in export markets, alongside a growing in-house IPP portfolio that would give WRTL a stream of annuity-like cash flows to complement the lumpier EPC revenues. If the IPP portfolio scales and is carried at book value, there is potential for sum-of-the-parts re-rating.

Frequently Asked Questions

Q1. Is Waaree Renewable Technologies the same company as Waaree Energies?

No. Waaree Energies is the separately listed parent and manufactures solar modules. Waaree Renewable Technologies is a listed subsidiary focused on solar EPC and selective IPP ownership. They are part of the same promoter group but are distinct companies with different business models and share prices.

Q2. How does WRTL make money?

Primarily by executing turnkey solar EPC contracts — design, procurement, construction and commissioning — for utility-scale, C&I, and hybrid clients, plus long-term O&M revenue. A smaller but growing stream comes from owning solar plants and selling power under PPAs or on a merchant basis.

Q3. Why is the ROCE so much higher than typical EPC companies?

EPC is inherently capital-light; ROCE is a function of asset turn and margin. WRTL has run a disciplined working-capital cycle and has captured operating leverage on a rapidly growing top line, pushing three-year ROCE to 89% versus mid-teens for generic infrastructure EPC peers.

Q4. Is the P/E of ~51x justified?

It depends on forward growth visibility. If the current order book and policy backdrop translate into 30%+ earnings CAGR over the next two years, the forward P/E compresses quickly. If growth moderates or margins compress, the multiple looks rich versus peers in the teens.

Q5. What is the biggest single risk?

A combination of order-book concentration with state utility customers and receivable-cycle elongation would hurt most — both P&L and balance sheet. Policy-driven module price swings are the second-order risk that can amplify or dampen any such stress.

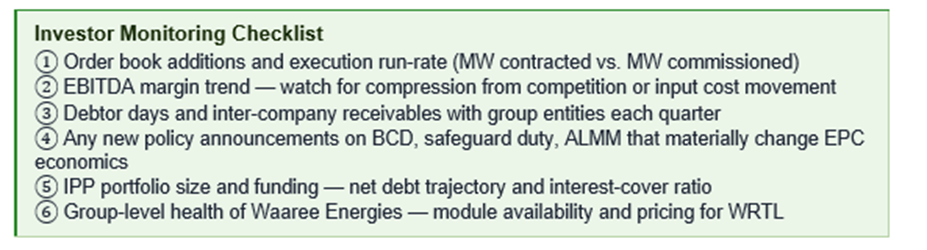

Q6. What should investors monitor each quarter?

Order book additions and execution run-rate, EBITDA margin trend, debtor days, inter-company receivables with group entities, and any new policy announcements that materially change EPC economics. Company quarterly filings are the primary reference points.