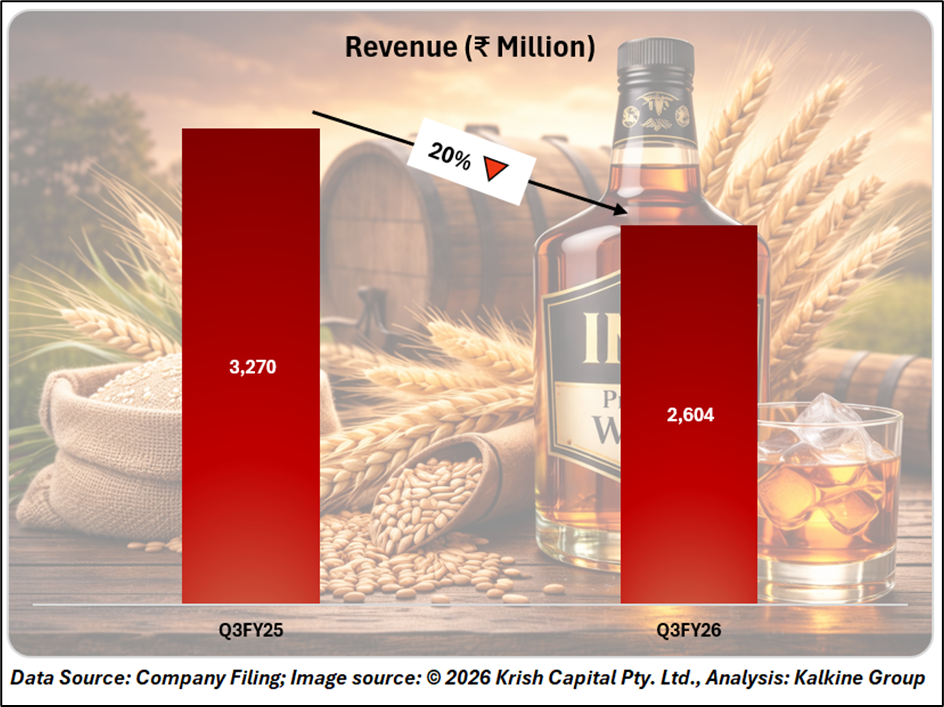

Shares of Associated Alcohols & Breweries Ltd. have witnessed a prolonged correction over the past year, declining nearly 29% over 12 months, around 24% in nine months, and close to 20% in the last six months. The pressure intensified following the company’s Q3FY26 earnings, which reported a 20% YoY decline in revenue to ₹2,604 million, compared with ₹3,270 million in Q3FY25.

At first glance, the sharp fall in revenues raised concerns over business momentum. However, a closer look at the earnings call and investor presentation suggests that the weakness reflects a strategic restructuring of operations, rather than a deterioration in demand or competitive positioning.

Why Revenue Decline?

The primary driver behind the topline contraction was the transition of the company’s franchisee and licensed business particularly with Inbrew from a license-based arrangement to a contract manufacturing model. Under this structure, revenues are no longer fully consolidated, even though production activity continues.

Management clarified that this shift led to the exclusion of Inbrew-related revenues from reported numbers, materially impacting the topline.

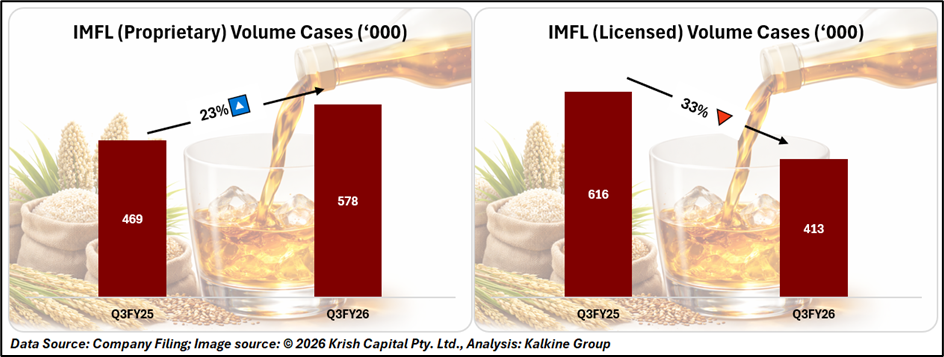

As a result, IMFL licensed volumes declined by 33% YoY, while licensed revenues dropped by nearly 30% YoY. This accounting and business-model change distorted year-on-year comparisons and weighed on investor sentiment. In parallel, ethanol sales remained subdued due to industry-wide oversupply, while merchant ENA volumes moderated as more output was consumed internally. These factors further contributed to the weak headline growth.

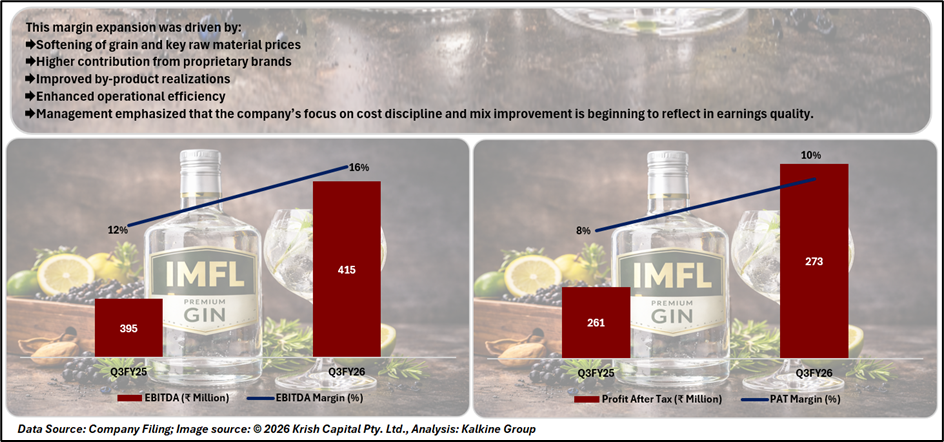

Margin-Led Performance Signals Underlying Strength

Despite the revenue decline, Associated Alcohol delivered a strong improvement in profitability. During Q3FY26, EBITDA increased to ₹415 million, with margins expanding sharply to 16% from 12% in the previous year. Profit after tax rose 5% YoY to ₹273 million, while PAT margins improved to 10% from 8%.

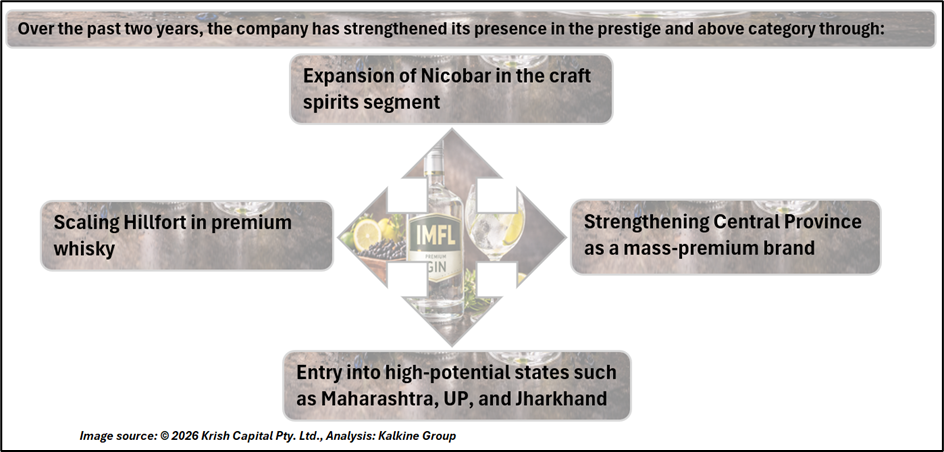

Premiumisation: Strategic Shift Toward Higher-Value Segments

Associated Alcohol is steadily repositioning itself from a volume-driven manufacturer to a premium-focused alcobev player.

Strong Product Pipeline Enhances Growth Visibility

These launches are aligned with state excise renewal cycles and regulatory timelines to ensure smoother market entry.

Notably, Associated Alcohol has obtained authorization to bottle authentic tequila, positioning it among early domestic players in this fast-growing category.

Technical Analysis

Associated Alcohols is trading near ₹827.50, close to key support at ₹800.00–820.00, while remaining below its 20-day (₹860.00) and 50-day (₹886.00) moving averages, indicating a weak short-term trend. The downward-sloping averages and formation of lower highs reflect ongoing consolidation within a corrective phase. The RSI (~41) suggests subdued momentum. Volume remains muted, indicating lack of strong accumulation. Immediate resistance lies at ₹950.00–1,100.00, while a breakdown below ₹773.00 may extend weakness. Overall, the outlook remains cautious, with confirmation needed for trend reversal.

Conclusion

While Associated Alcohols has faced sustained stock price pressure, the correction appears more reflective of structural realignment than operational weakness. Margin expansion, premiumisation initiatives, and a strong product pipeline indicate improving business quality. Although near-term technical indicators remain cautious, the company’s strategic shift toward higher-value segments strengthens its medium-term growth visibility and profitability outlook.