Highlights

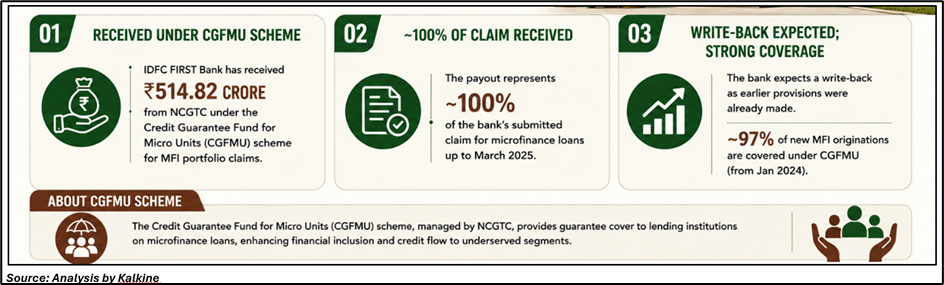

- IDFC FIRST Bank received INR 514.82 crore under CGFMU scheme from NCGTC.

- Claim relates to microfinance (MFI) portfolio loans sanctioned up to March 2025.

- Bank expects amount to be treated as write-back of earlier provisions.

IDFC FIRST Bank Limited (NSE:IDFCFIRSTB) announced that it has received a payout of INR 514.82 crore from the National Credit Guarantee Trustee Company (NCGTC) under the Credit Guarantee Fund for Micro Units (CGFMU) scheme.

The disclosure was made under Regulation 30 of SEBI Listing Regulations. The update was also submitted to National Stock Exchange of India Limited and BSE Limited as part of the regulatory compliance requirements.

CGFMU Claim Payout Details

The bank confirmed that the payout of INR 514.82 crore pertains to its microfinance loan portfolio under the CGFMU scheme. These loans are primarily extended to women entrepreneurs operating in Joint Liability Groups.

The claim represents approximately 100% of the amount submitted by the bank for eligible microfinance loans sanctioned up to March 2025. The payout has been received from NCGTC under the credit guarantee framework designed for micro units.

Impact on Provisioning and Financials

According to the disclosure, IDFC FIRST Bank had already made provisions for these microfinance loan defaults in earlier periods. As a result, the amount received is expected to be accounted for as a write-back of provisions.

This implies that the payout may contribute to an improvement in the bank’s financial position by reversing earlier credit loss provisions related to the MFI portfolio.

The bank clarified that the microfinance lending segment continues to be covered under the CGFMU scheme, with around 97% of new MFI loan originations from January 2024 onwards included under the guarantee framework.

Microfinance Exposure and Coverage

The bank’s microfinance portfolio includes loans extended under the Joint Liability Group structure, which is commonly used for small-ticket lending to women borrowers.

The CGFMU scheme provides credit guarantee support for eligible micro units, reducing risk exposure for lending institutions in case of defaults. The bank stated that coverage under the scheme has increased significantly for recent originations.

Regulatory Disclosure and Compliance

The announcement was made in compliance with Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015. The bank confirmed that the information has also been made available on its official website.

The disclosure was signed by Satish Gaikwad, General Counsel and Company Secretary of IDFC FIRST Bank.

Key Risks Investors Should Track

- Microfinance portfolio performance may remain sensitive to rural credit cycles.

- Dependence on government guarantee schemes may influence recovery timing.

- Changes in CGFMU scheme terms could impact future coverage levels.

- Higher provisioning cycles may affect earnings stability in lending segments.

Summary

IDFC FIRST Bank (NSE:IDFCFIRSTB) reported receipt of INR 514.82 crore under the CGFMU scheme from NCGTC for its microfinance portfolio. The payout relates to loans sanctioned up to March 2025 and is expected to be treated as a write-back of earlier provisions made by the bank. The update reflects continued coverage of most new MFI originations under the government-backed credit guarantee framework.

FAQs

Q: What amount did IDFC FIRST Bank receive under CGFMU scheme?

A: The bank received INR 514.82 crore from NCGTC under the Credit Guarantee Fund for Micro Units scheme.

Q: What does the CGFMU payout relate to?

A: It relates to microfinance loans given to women entrepreneurs under Joint Liability Group structure.

Q: How will the payout impact the bank’s financials?

A: The amount is expected to be treated as a write-back of earlier provisions made for MFI loan defaults.