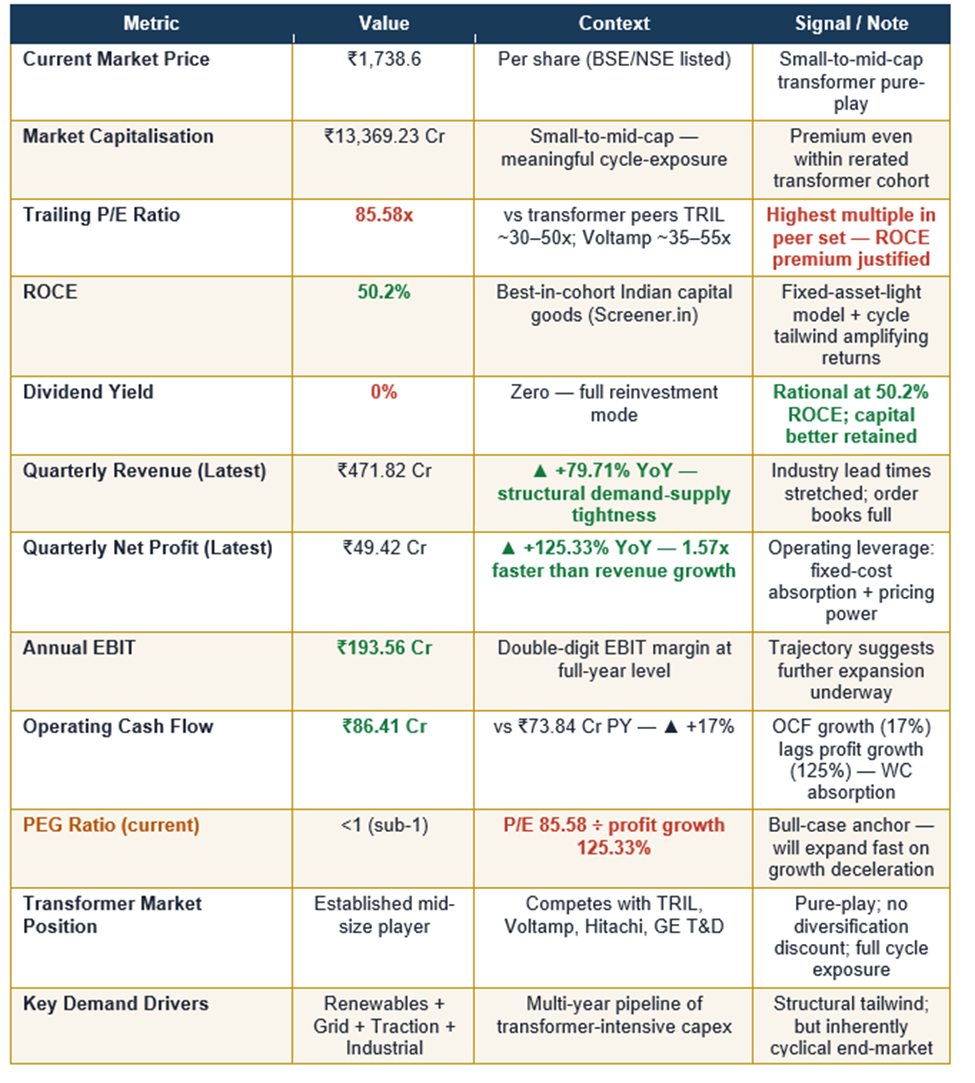

Key Financial Metrics:

Source: company BSE/NSE filings. Verify current data at bseindia.com and nseindia.com

Company Overview

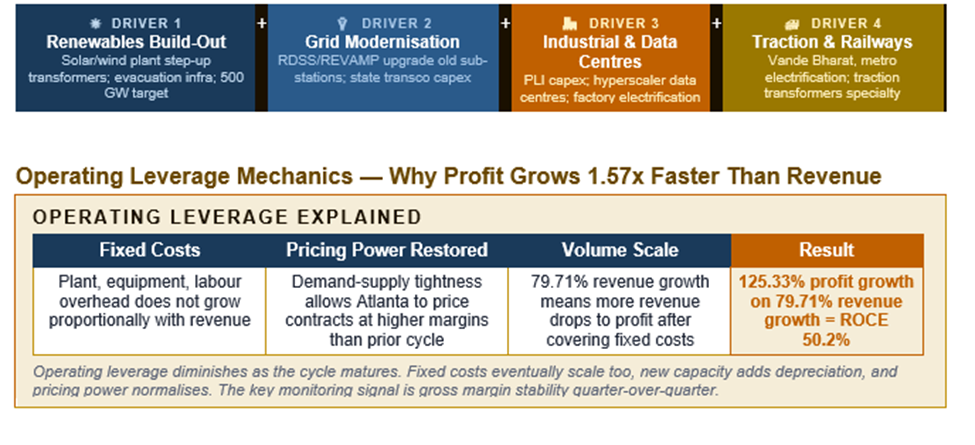

Atlanta Electricals Limited (NSE/BSE:ATLANTAELE) is an Indian transformer manufacturer specialising in power transformers, distribution transformers, and specialty transformers for renewable-energy plants, traction (railways), and industrial applications. The company sits squarely in the middle of one of the strongest demand cycles in Indian capital goods: a structural shortage of transformers driven by the simultaneous build-out of renewable-energy capacity, grid modernisation, transmission expansion to evacuate renewable power, and rising electricity demand from industrials and data centres.

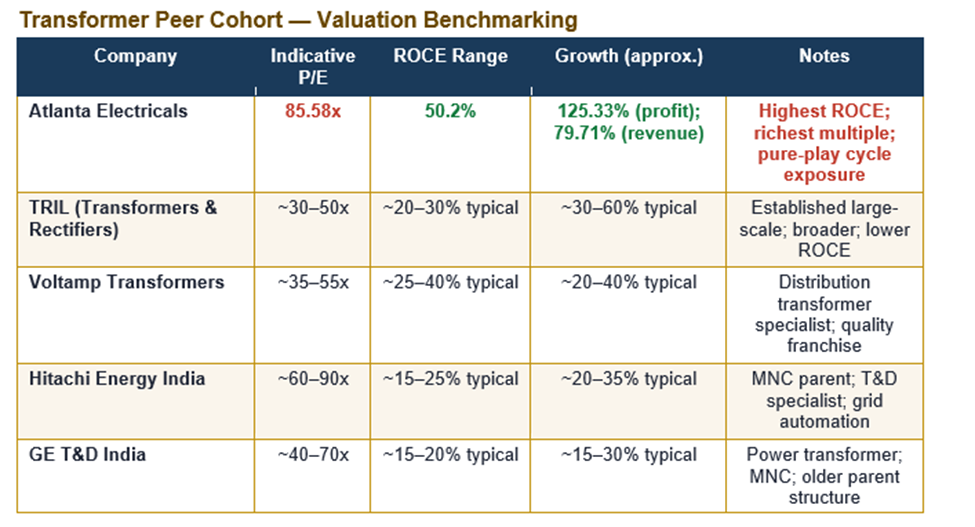

The transformer industry in India — dominated by established names including Transformers and Rectifiers India (TRIL), Voltamp, Hitachi Energy, GE T&D, and Atlanta Electricals — has moved from a structurally low-margin commoditised business to a sellers' market in the past two to three years. Order books across the industry have expanded sharply, lead times have stretched, and pricing power has returned. This is the macro environment driving Atlanta's exceptional 80% revenue growth and 125% profit growth in the latest quarter.

Transformer Demand Architecture & Market Position:

Peer P/E and ROCE ranges are indicative from publicly available data..

Financial Performance & Insights

The latest quarter is one of the strongest prints in the Indian capital-goods space. Revenue of ₹471.82 crore grew 79.71% YoY. Net profit of ₹49.42 crore grew 125.33% — dramatically outpacing revenue growth and confirming powerful operating leverage. Profit growing 1.57x faster than revenue suggests fixed-cost absorption is improving rapidly and pricing realisation in transformer contracts is firm.

Annual EBIT of ₹193.56 crore implies a healthy double-digit EBIT margin at the full-year level, and the trajectory suggests further margin expansion is underway. Operating cash flow of ₹86.41 crore versus ₹73.84 crore in the prior year shows positive cash generation, though notably cash flow growth (17%) lags profit growth (125%) — typical of a transformer business in aggressive scale-up mode where receivables and work-in-progress inventory absorb cash as the order book expands.

ROCE of 50.2% is exceptional. Few Indian manufacturers operate at this level of capital efficiency. The combination of triple-digit profit growth, expanding margins, and elite ROCE is the kind of combination that justifies premium multiples — the question is for how long the cycle holds.

Risk ratings are qualitative assessments based on Screener.in data and BSE/NSE filings. Analysis by Kalkine

Price Performance

Atlanta Electricals has been a market favourite, with the stock rerating dramatically as the transformer cycle has accelerated. Price action reflects two layers: the broad rerating of the entire transformer cohort, and Atlanta's idiosyncratic outperformance driven by its superior ROCE and operating leverage. Comparable transformer plays such as TRIL and Voltamp have all moved sharply higher, and the entire cohort now trades at multiples that would have been unimaginable two years ago.

Volatility is high. Transformer stocks move on order-book disclosures, capacity-addition announcements, and quarterly margin prints. Investors entering at current levels should expect this volatility to persist, with sharp swings around quarterly results and any industry-level news on order flows.

Shareholder Returns & Capital Allocation

Atlanta Electricals pays no dividend (0% yield). Capital is being reinvested in capacity expansion, working capital to support order-book conversion, and potentially product diversification. Given a ROCE of 50.2%, this is straightforwardly the right capital-allocation decision — every rupee of internal accruals retained is generating substantial value well above its cost.

Long-term shareholders should evaluate total return through earnings compounding rather than current income. As the business matures and the cycle moderates, a transition to modest dividend payments would be a signal that management believes reinvestment opportunities at 50%+ ROCE are becoming scarce — a structural milestone to watch for.

Key Risks

1 — Transformer Cycle Risk (Dominant)

Cycle risk is the dominant concern. Transformer demand has historically been cyclical, and current order-book strength reflects an unusually favourable confluence of factors. When this cycle eventually moderates — even to a still-healthy 15–20% growth rate — transformer stocks have historically de-rated sharply. Investors should think of Atlanta Electricals as a tactical cyclical position rather than a structural compounder.

2 — Valuation Risk at 85.58x P/E

At 85.58x P/E with a PEG below 1, the valuation is supported by current extraordinary growth rates. The moment growth decelerates toward 25–30% (still excellent), PEG expands rapidly, and the market typically re-rates transformer stocks toward their historical 20–40x range. A stress-test at 30–40x P/E (the level of TRIL and Voltamp in a normal cycle) on current earnings implies 50–65% downside from current levels — not a prediction, but a scenario investors must size against.

3 — Other Risks

- Working-capital risk: Rapid order-book scaling absorbs cash; execution slippage on large contracts can stretch receivables. OCF/PAT ratio is the key metric to monitor.

- Raw-material risk: Copper, CRGO electrical steel, and transformer oil are major cost inputs. Sustained spikes compress margins.

- Customer concentration: State-utility tenders carry payment-cycle risk during fiscal stress or political transitions.

- Competitive intensity: Established peers are adding capacity; global majors targeting the Indian transformer market will intensify bidding competition.

- Quality and warranty risk: Transformer failures can produce significant warranty exposure and reputational damage.

Valuation

At a P/E of 85.58x and a market cap of ₹13,369 crore, Atlanta Electricals is priced at a meaningful premium even within the already-rerated transformer cohort. The bull case rests on the cycle having multiple years to run, 50.2% ROCE earning a structural premium, and operating leverage continuing to deliver profit growth above revenue growth. On these assumptions, valuation can be justified by forward earnings.

Business Strategy & Outlook

Strategy centres on four pillars. First, capacity expansion to capture the multi-year transformer demand cycle without losing share to peers also adding capacity. Second, mix-shift towards higher-rated power transformers and specialty applications — renewable-plant transformers, traction, industrial — where pricing and margins are superior to standard distribution transformers.

Third, deepen relationships with state utilities (PGCIL and state transcos) and large private renewable-energy developers to secure long-tenor order visibility. Fourth, maintain operational excellence and quality track record — reputation is the moat in a tendered industry where past performance qualifies for future bids.

The 80% revenue growth and 125% profit growth confirm execution is excellent. The next watch-items are order-book additions, capacity utilisation post-expansion, and any signs of receivables stretching. Consistent delivery on these metrics is what validates the premium multiple; slippage on any one is what triggers the de-rating.

Frequently Asked Questions

Q1. What does Atlanta Electricals do?

It manufactures power transformers, distribution transformers, and specialty transformers for utilities, renewable-energy projects (solar and wind), railways (traction), and industrial customers. It is a pure-play on India's power-infrastructure build-out.

Q2. Why did profit grow 125% when revenue grew only 80%?

Operating leverage — fixed-cost absorption improves rapidly as volumes scale, and pricing realisation in transformer contracts has firmed up given industry-wide demand-supply tightness. The same phenomenon that drives ROCE to 50.2% creates the profit-revenue growth differential.

Q3. Is the transformer demand cycle durable?

The demand cycle is supported by India's transmission build-out, renewable capacity additions (500 GW target by 2030), grid modernisation, and rising industrial/data-centre electricity demand — a multi-year runway. However, transformer demand is historically cyclical, and current growth rates (79–125%) will normalise over time. The investment case depends on the cycle remaining active for 2–4 more years.

Q4. What are the biggest risks?

Cycle risk (primary — de-rating when growth moderates), valuation risk at 85.58x P/E, working-capital risk during scale-up (OCF lagging profit growth), raw-material volatility (copper, CRGO, transformer oil), customer concentration in utility tenders, intensifying competition, and quality/warranty exposure.

Q5. Does Atlanta Electricals pay dividends?

No. Dividend yield is 0%. Capital is being reinvested in capacity expansion and working capital. At 50.2% ROCE, retention is the value-maximising choice.