For Indian retail investors looking to capitalise on India's economic growth story, the best PSU stocks for 2026 offer a compelling blend of government backing, sector dominance, regular dividends, and participation in the country's largest infrastructure and defence capex programmes. Public Sector Undertakings (PSUs) — companies where the central or state government holds more than 51% equity — form the backbone of India's strategic industries, from oil exploration to fighter aircraft manufacturing.

As of mid-2026, the BSE PSU index has navigated a mixed macro environment: global crude volatility, domestic interest rate cuts, a robust Union Budget capital expenditure push of ₹12.2 lakh crore for FY27, and a structural uptick in defence indigenisation. Total PSU market capitalisation stands near ₹69–70 lakh crore, and aggregate PSU profits have grown from roughly ₹1.2 lakh crore in FY20 to an estimated ₹5.3 lakh crore in FY25 — a 36% CAGR. This article examines the key PSU names across sectors, their fundamentals, catalysts, and the risks every investor should understand.

Sector Overview: The PSU Universe in 2026

India's listed PSU universe is large and diverse. The S&P BSE PSU Index and the Nifty PSE Index together cover oil and gas, power generation and transmission, banking and financial services, defence and aerospace, metals and mining, railways and logistics, and telecommunications. As of March 2026, the BSE PSU Index stood at approximately 21,405 and the Nifty PSE's dividend yield (2.96%) ran nearly double that of the Nifty 50 (1.39%), reflecting the sector's stronger income profile.

The index remains concentrated in oil and gas (ONGC, IOC, BPCL, GAIL), power (NTPC, Power Grid), and banking (SBI, Bank of Baroda), with SBI commanding the highest BSE PSU Index weightage at 15.47%, followed by LIC (7.79%), NTPC (5.75%), ONGC (5.22%), Power Grid (4.35%), and HAL (4.15%). Defence and railway PSUs — though smaller in weightage — have seen outsized re-rating in recent years thanks to order book momentum and policy tailwinds.

Why PSU Stocks Matter in 2026

Several structural themes make 2026 a particularly relevant year to study PSU stocks. First, India's government capex cycle remains robust: Central Public Sector Enterprises (CPSEs) spent over 99% of the revised FY26 capex target of ₹7.47 lakh crore — the fourth consecutive year of near-full execution. FY27 public capex guidance of ₹12.2 lakh crore represents another step-up, benefiting PSUs in defence, railways, power, and infrastructure.

Second, the PSU re-rating narrative — where PSU stocks' P/E and P/B multiples converge toward private-sector peers — remains partially intact. PSU banks, for instance, rallied nearly 33% in the Nifty PSU Bank Index over FY25, driven by a dramatic improvement in asset quality (gross NPAs down from 10–15% to 2.5–5% range).

Third, the government's dividend incentive is structurally significant: the Government of India relies on PSU dividends as a meaningful source of non-tax revenue. This creates a strong implicit incentive for PSUs to maintain high payout ratios, making many of them attractive income stocks. That said, dividends are subject to annual board approval and depend on profitability — they are never guaranteed.

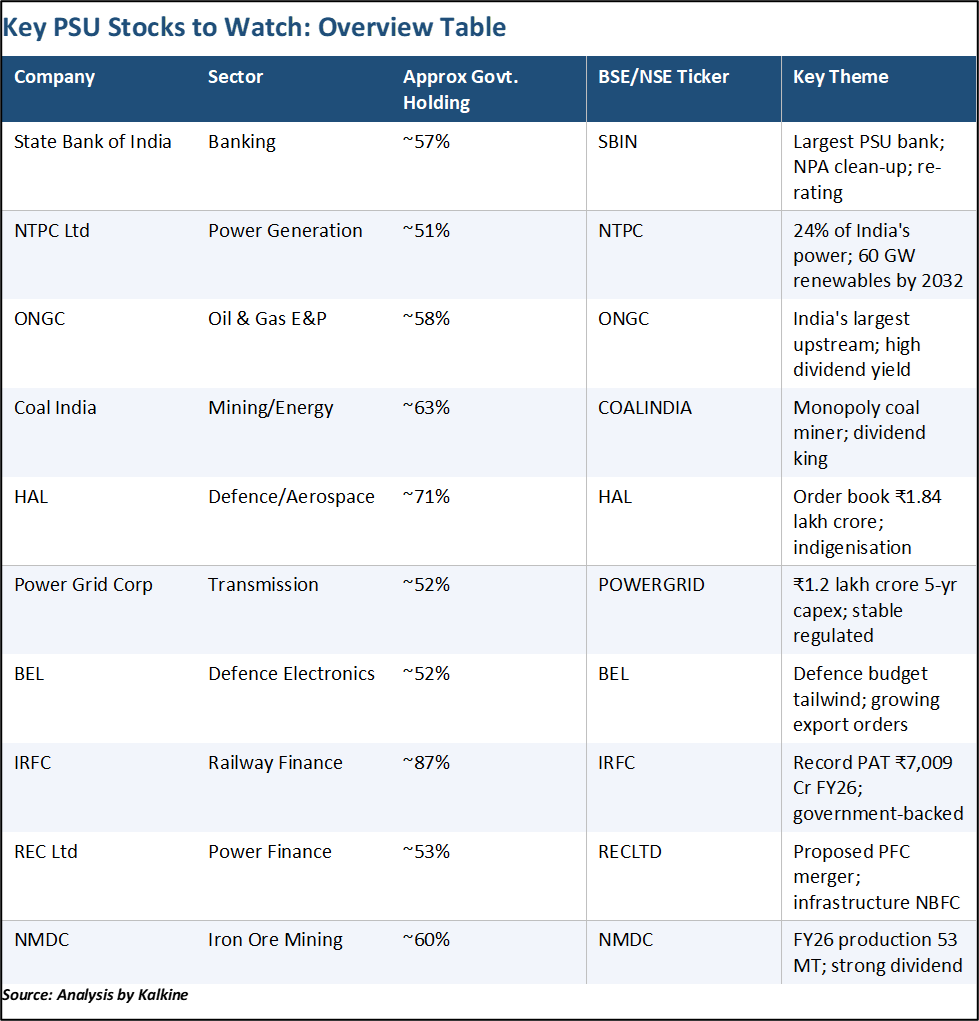

Company-by-Company Analysis

State Bank of India (SBI)

SBI is India's largest bank by assets and the biggest PSU by market capitalisation in the BSE PSU Index, with a market cap of approximately ₹9.5–9.7 lakh crore as of early 2026. After a decade-long NPA clean-up cycle, SBI's gross NPA stands near 2.5% and net NPA at approximately 0.39%, with a capital adequacy ratio of about 15.40%. Return on equity has recovered to an estimated 14–17% range. At approximately 1.1–1.3x book value, SBI trades at a steep discount to large private sector peers despite comparable asset quality and profitability metrics. Key risks include margin pressure from interest rate cuts, slowing credit growth, and periodic government interference in lending decisions.

NTPC Ltd

NTPC (NSE:NTPC) is India's largest power generation company, commanding approximately 24% of the country's total electricity generation. The company has a dividend yield of approximately 2.22–2.49% (verify current yield on NSE) and transferred ₹2,666 crore to the Ministry of Power as its second interim dividend for FY26. NTPC's most watched long-term catalyst is its 60 GW renewable energy target by 2032, which requires adding substantial green capacity every year through 2032. This clean energy transition involves significant capital investment but positions NTPC at the heart of India's energy security strategy. The company's regulated return model on thermal assets provides earnings stability, while the renewable ramp-up is a growth optionality.

ONGC

Oil and Natural Gas Corporation (NSE:ONGC) is India's dominant upstream explorer, with a market cap of approximately ₹3.3 lakh crore as of June 2, 2026, and a P/E ratio of approximately 8.0x — making it one of the cheapest large-cap PSUs on earnings multiples. ONGC's dividend yield stood at approximately 5.0–8.4% across different measurement periods in 2025–2026 (yields fluctuate with price; always verify on NSE). The company paid an interim dividend of ₹6.25 per share in February 2026. Key catalysts include oil price recovery, gas price revisions, and progress on the KG Basin deepwater block. Risks include crude price volatility, ageing fields, and subsidy-sharing obligations.

Hindustan Aeronautics Limited

HAL (NSE:HAL) is India's premier aerospace and defence manufacturer, with an order book of ₹1.84 lakh crore as of early 2026 — up from ₹94,129 crore the prior year. This doubling of the order book reflects accelerating indigenisation under the government's defence self-reliance programme ('Aatmanirbhar Bharat'). HAL's key products include the Tejas Light Combat Aircraft, Advanced Light Helicopters, Dhruv, and upgrades for Sukhoi fighter jets. The Union Budget FY27 has allocated ₹1.85 lakh crore for defence capital expenditure, focused on domestic procurement. HAL shares rose 3.4% to ₹4,025 on March 6, 2026, when broader defence sector optimism resurfaced. The major risk is execution — converting the large order book into recognised revenue requires manufacturing scale-up and supply chain readiness.

Coal India

Coal India (NSE:COALINDIA) is the world's largest coal mining company and holds a near-monopoly on coal production in India. The company's market cap was approximately ₹2.77 lakh crore as of January 2026, and it has been one of the most consistent dividend payers in the PSU universe (detailed in the companion PSU Dividend Stocks article). FY26 EPS stood at approximately ₹50.46, down from ₹57.37 in FY25, reflecting some pressure on volumes and realisations. However, the payout ratio remained around 52%, and Coal India has a 5-year dividend growth rate of approximately 10.6%. Risks include the long-term energy transition away from coal, environmental pressures, and government-mandated pricing policies.

Bharat Electronics Limited

BEL (NSE:BEL) is India's premier defence electronics PSU, with a government holding of approximately 52%. The stock traded at approximately ₹473 in early March 2026. BEL benefits from the defence sector's accelerating budget allocation — the defence budget for FY26 was ₹6.8 lakh crore (up 9.5% YoY) — and growing demand for radar, communication systems, electronic warfare equipment, and surveillance products. BEL has also been growing its export order book as Indian defence products gain international recognition. BDL (Bharat Dynamics Limited) and Mazagon Dock Shipbuilders are other defence PSUs with strong order visibility.

Indian Railway Finance Corporation

IRFC (NSE:IRFC) is the dedicated financial arm of Indian Railways, borrowing from capital markets and on-lending exclusively to the Ministry of Railways. The company reported its highest-ever profit of ₹7,009 crore for FY26, up 7.8% from ₹6,502 crore in FY25, with government ownership at approximately 87%. IRFC's business model is simple and low-risk: its entire loan book is to a single sovereign borrower (Indian Railways), with no credit risk. Key risks are refinancing risk and interest margin compression if spreads narrow. Railway stocks broadly fell 12–21% after the February 2025 budget on valuation concerns, but IRFC subsequently rallied more than 20% in a five-session period on improved sentiment.

Power Grid Corporation

Power Grid Corporation of India (NSE:POWERGRID) is the dominant electricity transmission utility, operating on a regulated return model that provides earnings visibility over multi-year periods. The company reported PAT of ₹4,160 crore in Q3 FY26 and declared a dividend of ₹3.25 for the period. Power Grid has announced a five-year capital expenditure plan of ₹1.2 lakh crore, driven by the need to expand and upgrade India's transmission network to handle rising renewable energy generation. The dividend yield on Power Grid has historically ranged between 3% and 4% (verify current yield). As a regulated utility, earnings growth is measured but predictable, making it suitable for conservative long-term investors.

Recent News & Market Triggers

- Union Budget FY27 set public capex at ₹12.2 lakh crore — up ~10% YoY — directly benefiting defence, railway, and power PSUs.

- PFC-REC merger: In February 2026, PFC and REC gave in-principle approval for a proposed merger. The combined entity would have a loan book of ~₹11.5 lakh crore, creating India's largest infrastructure NBFC.

- HAL order book doubles to ₹1.84 lakh crore — a testament to the government's Aatmanirbhar defence procurement push, with Tejas Mk-2 and helicopter orders driving growth.

- Nifty PSU Bank Index rallied ~33% in FY25, as PSU banks reported multi-year highs in profitability and asset quality; momentum has continued selectively into 2026.

- IRFC records highest-ever PAT of ₹7,009 crore in FY26, up 7.8% YoY, anchored by Indian Railways' record capital expenditure programme.

- GAIL profit falls 38% to ₹6,968 crore in FY26 amid global LNG price headwinds and higher trading losses — a reminder of commodity exposure even for pipeline PSUs.

- CPSEs hit 99% of FY26 capex target — marking the fourth straight year of near-full execution, boosting confidence in PSU delivery on government infrastructure programmes.

Growth Drivers

- Aatmanirbhar Bharat in Defence: Mandatory domestic procurement lists and rising indigenisation targets drive multi-year revenue visibility for HAL, BEL, BDL, Mazagon Dock, BEML.

- Energy Transition Capex: NTPC's 60 GW renewable target by 2032 and Power Grid's ₹1.2 lakh crore transmission capex plan create long-term volume growth for power PSUs.

- Indian Railways Modernisation: The ₹2.80 lakh crore railway allocation in FY27 Budget — covering high-speed corridors and rolling stock — sustains IRFC, RVNL, IRCON, and RailTel revenue pipelines.

- PSU Bank Earnings Recovery: Gross NPAs down to 2.5–5% range from 10–15% in FY19; return on equity above 12% across the sector; dividend payouts have resumed and grown.

- Dividend Income to the Exchequer: The government's reliance on PSU dividends as non-tax revenue creates a structural incentive for high payout ratios, supporting investor income.

- Commodity Cycle & Pricing Power: Iron ore (NMDC), coal (Coal India), and aluminium (NALCO) benefit from domestic demand growth even if global prices remain volatile.

- Natural Gas Infrastructure: GAIL's commissioning of ~2,000 km of new pipelines in FY26, including the Mumbai-Nagpur-Jharsuguda corridor, underpins India's gas grid expansion.

- Valuation Gap vs. Private Peers: PSU stocks continue to trade at P/E and P/B discounts to private-sector counterparts — providing a re-rating margin of safety for patient investors.

Risks Investors Should Know

- Government Policy Interference: PSUs may be directed to pursue social or strategic objectives that do not maximise shareholder returns — e.g., oil marketing companies absorbing fuel subsidies, PSU banks directed to lend to priority sectors.

- Disinvestment / Stake Sale Overhang: Government stake sales (OFS, FPO) can create near-term selling pressure and price dilution. India has historically underperformed its disinvestment targets; FY26 revised estimate was cut to ₹33,837 crore from ₹47,000 crore.

- Earnings Cyclicality: Oil PSUs (ONGC, IOC, BPCL) are highly sensitive to crude oil prices and refining margins. Metals PSUs (NMDC, SAIL, NALCO) are exposed to commodity price cycles. GAIL's PAT fell 38% in FY26.

- Dividend Sustainability: Dividends depend on annual profitability and board approval — they are not guaranteed. Government pressure for high payouts can sometimes reduce reinvestment capacity.

- Valuation Traps: Some PSU stocks may appear cheap on P/E but face structural decline (e.g., coal mining faces long-term energy transition headwinds). Low multiples do not automatically mean upside.

- Project Execution Risk: Large capex programmes (NTPC renewables, Power Grid transmission, HAL production scale-up) face execution delays, cost overruns, and regulatory hurdles.

- Interest Rate Sensitivity: Financial PSUs (IRFC, REC, PFC) borrow from capital markets; rising interest rates compress spreads and can reduce profitability.

- Concentration Risk: BSE PSU Index is heavily concentrated in oil and gas, power, and banking — limited diversification benefit within the PSU universe.

Valuation Considerations

As of March 31, 2026, the Nifty PSE's P/E and P/B ratios remain below those of the Nifty 50, indicating that PSU stocks as a group continue to trade at a benchmark-level discount. This discount reflects genuine concerns about governance, dividend sustainability, and government policy risk — but also represents a potential margin of safety for investors willing to do stock-specific due diligence.

Key valuation data points to verify on NSE/BSE: ONGC P/E ~8.0x (June 2026); SBI P/B ~1.1–1.3x; PSU banks broadly at 40–70% discount to private bank P/B multiples. RVNL was trading at 4.84x book value — an elevated multiple for a project-execution company, suggesting that not all PSU stocks are uniformly cheap.

Investors should assess each PSU on a sector-appropriate metric: P/B for banks, EV/EBITDA for commodity companies, P/E for regulated utilities, and order-book-to-revenue for capital goods and defence names. A blanket 'PSU discount' argument is not sufficient justification for any single stock purchase.

Long-Term Outlook

The long-term case for select PSU stocks rests on India's structural growth story: a $5-trillion GDP ambition, energy security imperatives, indigenous defence manufacturing, and one of the world's largest infrastructure buildout programmes. PSUs sit at the intersection of all these themes. Aggregate CPSE profits grew at 36% CAGR from FY20 to FY25, a track record that has attracted both domestic and foreign institutional investors.

However, the easy re-rating phase — where PSU stocks simply re-rated from multi-year lows — may be largely behind us for several sub-sectors. Future returns will increasingly depend on earnings growth, capital allocation discipline, and execution quality rather than pure valuation expansion. Investors with a 5–10 year horizon may find value in PSUs that combine genuine earnings growth (defence, power infra, railways finance) with high dividend payouts (coal, oil, metals). Shorter-term investors should be aware that PSU stocks can underperform during risk-off periods when government policy uncertainty rises.

Frequently Asked Questions

Q: What is a PSU stock in India?

A: A PSU (Public Sector Undertaking) stock is a share in a company where the central or a state government holds more than 51% of the equity. Examples include SBI, NTPC, ONGC, Coal India, HAL, and Power Grid. These companies are listed on NSE and BSE and can be bought and sold like any other stock.

Q: Are PSU stocks safe investments?

A: Government ownership provides a degree of stability — PSUs are unlikely to go bankrupt in the traditional sense. However, 'safe' does not mean risk-free. PSU stocks can and do fall in price; earnings can decline (as seen with GAIL in FY26); dividends can be cut; and government interference can harm shareholder returns. Conduct your own research or consult a SEBI-registered investment adviser.

Q: Which is the best PSU stock for 2026?

A: There is no single 'best' PSU stock — the right choice depends on your investment horizon, risk appetite, income vs. growth preference, and sector views. SBI may suit investors looking for large-cap banking exposure; NTPC or Power Grid for regulated utility income; HAL or BEL for defence growth; Coal India for high dividend yield. This article is educational and not a recommendation to buy or sell any specific stock.

Q: What is the Nifty PSE Index?

A: The Nifty PSE (Public Sector Enterprises) Index is a stock market index of NSE-listed public sector companies. It includes major PSUs across sectors and is used as a benchmark for PSU-focused funds. As of March 2026, its dividend yield (2.96%) was nearly double that of the Nifty 50 (1.39%), reflecting the higher income profile of the PSU universe.

Q: How does disinvestment affect PSU stocks?

A: Government disinvestment — selling a portion of its stake in a PSU through OFS (Offer for Sale), FPO, or strategic sale — can create near-term supply pressure and share price volatility. However, a reduced government holding can also improve governance and market float, which may be positive long-term. India's FY27 disinvestment target is ₹80,000 crore; historically, actual receipts have been below target.

Q: Can PSU stocks be good for long-term investing?

A: Select PSU stocks have delivered strong long-term returns — PSUs added approximately ₹57 lakh crore in market cap from March 2020 to June 2025. However, returns have been uneven: some PSUs are strong compounders while others have been value traps. Long-term investing in PSUs requires conviction in the specific company's earnings trajectory and sector tailwinds, not just reliance on government ownership.

Q: What is the difference between Maharatna, Navratna, and Miniratna PSUs?

A: These are government-designated status categories for CPSEs (Central Public Sector Enterprises) based on financial size and operational autonomy. Maharatna companies (14 as of 2026, including SBI, NTPC, ONGC, Coal India, IOC, HAL, Power Grid) have the highest financial powers and operational independence. Navratna companies have intermediate powers, and Miniratna companies have limited operational autonomy. Maharatna status generally signals a more established and financially strong company.

Conclusion

Identifying the best PSU stocks for 2026 requires looking beyond the label of 'government-owned' and examining each company's earnings trajectory, sector tailwinds, dividend history, valuation, and governance track record. SBI leads PSU banking with a strengthened balance sheet; NTPC anchors the power sector through thermal operations and a renewable pivot; HAL and BEL represent the defence indigenisation opportunity; Coal India and ONGC are the income workhorses of the PSU universe; and IRFC offers near-sovereign credit quality in railway financing.

The PSU universe collectively trades at a discount to broader market multiples, and the government capex cycle — with FY27 spending guided at ₹12.2 lakh crore — continues to underpin PSU earnings across infrastructure-linked sectors. But risk management is essential: dividends are not guaranteed, disinvestment overhangs are real, and commodity-exposed PSUs face earnings cyclicality. This article is educational only. Please verify all data on NSE/BSE and consult a SEBI-registered financial adviser before making investment decisions.