Finding the best railway stocks for long-term investment in India requires more than picking PSU names — it demands understanding order books, government capex cycles, technological transitions, and valuation discipline. India's railway sector is undergoing its most ambitious modernisation in decades, spanning Vande Bharat trainsets, Kavach automatic train protection, 99.6% broad-gauge electrification, station redevelopment, Dedicated Freight Corridors, and an accelerating metro network across 20+ cities.

The Union Budget FY27 (February 2026) allocated ₹2.78 lakh crore to the Ministry of Railways — the highest ever — up from ₹2.52 lakh crore in FY26. Sub-allocations include ₹52,108 crore for rolling stock, ₹36,721 crore for new lines, and ₹22,853 crore for track renewal. For listed companies that execute, supply, finance, or operate within this ecosystem, multi-year earnings visibility is compelling.

This guide analyses seven of the most-discussed railway stocks on NSE and BSE, covering fundamentals, competitive moats, recent triggers, and risks — giving Indian retail investors a structured framework to research further.

Sector Overview

India's railway universe on listed exchanges spans at least half a dozen sub-sectors: infrastructure execution (RVNL, IRCON), financing (IRFC), passenger services and ticketing (IRCTC), rolling stock and wagons (Titagarh Rail Systems, Jupiter Wagons, BEML, Texmaco Rail), ICT and telecom (RailTel), and logistics (CONCOR). Each business model responds differently to government spending cycles and competitive shifts.

Rail passenger traffic has recovered strongly post-pandemic, while freight tonne-kilometres continue to climb, aided by the Eastern and Western Dedicated Freight Corridors now in operation. Indian Railways aims to carry 3 billion tonnes of freight annually by 2030, up from roughly 1.7 billion tonnes in FY25 — a structural tailwind for wagon manufacturers, logistics operators, and corridor builders alike.

Why Railway Stocks Matter in 2026

The investment case for railway equities in 2026 rests on three pillars. First, government capex at record levels — ₹2.78 lakh crore in FY27 — directly funds project pipelines for construction PSUs and equipment suppliers. Second, technology-led demand: Kavach Version 4.0 has been commissioned on 1,452 km of key routes and will cover 18,000 km of high-density track, generating multi-year procurement orders. Third, premiumisation of travel: the Vande Bharat Sleeper, Metro Rail expansion in 20+ cities, and 1,337 stations being upgraded under the Amrit Bharat Station Scheme (ABSS) are long-duration contracts for listed suppliers and operators.

A note of caution: a 2025 Kotak Institutional Equities report flagged a 'large disconnect' between fundamentals and valuations in PSU railway stocks. Many of these names fell 40–55% from their 2024 peaks by early 2026 as earnings growth disappointed, budget allocations underwhelmed expectations, and the broader PSU re-rating cycle reversed. Long-term investors may find better entry points today, but valuation diligence remains essential. Please verify current prices on NSE/BSE before making any decision.

Company-by-Company Analysis

IRCTC — The Monopoly Marketplace

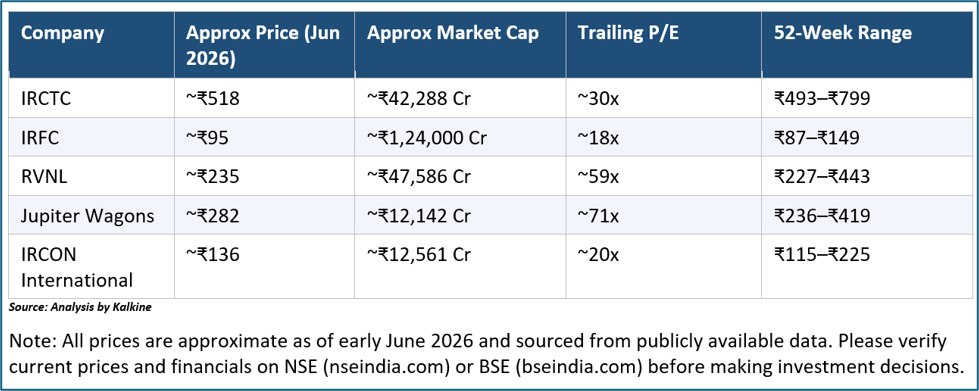

Indian Railway Catering and Tourism Corporation (NSE:IRCTC) is unique among railway stocks in that it holds a government-granted monopoly over online rail ticketing, catering on trains, and Rail Neer packaged water. As of June 2026, IRCTC trades near ₹517 with a market cap of approximately ₹42,288 crore, a P/E of ~30x, and a 52-week range of ₹492–₹799. Revenue stands at ₹5,215 crore with a profit of ₹1,393 crore. The promoter holds 62.4% equity, and the company is nearly debt-free with a 3-year average ROE of 37%.

The core investment thesis is its internet-ticketing and convenience-fee stream, which grows with rail passenger traffic and rising digital adoption. Tourism and premium travel packages add optionality. Risks include government policy changes on ticketing fees (happened once before), competition from third-party booking portals, and valuation premium typical of monopoly PSUs. Verify the latest stock price and dividend history on the NSE website.

IRFC — The AAA-Rated Financing Powerhouse

Indian Railway Finance Corporation (NSE:IRFC) is a dedicated NBFC that raises market borrowings and on-lends them to Indian Railways for rolling stock and infrastructure assets. In March 2025, IRFC was elevated to Navaratna PSU status by the Government of India. As of June 9, 2026, IRFC trades around ₹94–95 (52-week range: ₹87–₹149), with a market cap of ₹1.24 lakh crore, P/E near 17.7x, and a dividend yield of approximately 2.6%. FY25 revenue was ₹27,285 crore with net profit of ₹7,009 crore.

IRFC's near-zero credit risk (MoR is the sole borrower), AAA rating, and stable spread income make it a quasi-bond substitute with equity upside. Key risk: any restructuring of its funding relationship with MoR, spread compression in a rising interest-rate environment, or policy shifts could affect earnings. The stock has corrected significantly from its 2024 high; investors should independently assess current valuations on NSE before acting.

RVNL — The Execution Giant

Rail Vikas Nigam Limited (NSE:RVNL) is a Schedule-A Navaratna PSU that executes railway projects — electrification, new lines, gauge conversion, bridges, signalling — on behalf of Indian Railways. Its order book stands at approximately ₹90,000 crore, providing 3–4 years of revenue visibility. However, FY25 revenue declined 8.9% year-on-year to ₹19,923 crore, and net profit fell 17% to ₹1,281 crore. FY26's Q4 net profit reportedly declined ~59% year-on-year amid margin pressure.

Management has guided for ₹21,000–22,000 crore revenue in FY26 and 15–20% growth in FY27. RVNL trades around ₹234 as of June 2026 (52-week range: ₹227–₹443), down 47% over the past year, with a P/E near 59x — still elevated given recent earnings pressure. RVNL's scale and government backing remain advantages, but execution risks, margin compression, and receivables from KRCL (₹1,190 crore) are concerns to monitor.

BEML — Metro, Rolling Stock and Defence in One

BEML Limited (NSE:BEML) is a Schedule-A Ministry of Defence enterprise operating across rail and metro, mining and construction, and defence and aerospace. Its March 2026 order book stood at ₹15,896 crore; management is targeting over ₹31,000 crore in orders in FY27, with rail and metro comprising ~70% of the target mix. BEML trades around ₹1,747 as of June 2026 with a market cap of ₹14,504 crore. Revenue and profit data should be verified on NSE; the stock is above ₹500 and appeals to investors seeking diversified railway and defence exposure.

BEML manufactures metro coaches, Vande Bharat components, high-capacity coaches, and maintenance machinery. As India's metro network expands (20+ cities, multiple lines under construction), BEML stands as a key domestic supplier. Risks include execution delays, defence tender uncertainty, and competition from global rolling-stock suppliers.

Titagarh Rail Systems — From Wagons to Passenger Cars

Titagarh Rail Systems (NSE:TITAGARH) was once purely a freight-wagon manufacturer but has pivoted aggressively into metro coaches and passenger railcars. Its consolidated order book stood at ₹27,540 crore as of recent filings. In Q3 FY26, standalone revenue dipped 7.8% year-on-year to ₹832 crore, and profit before tax fell 26%, reflecting the transition-phase lumpiness of passenger railcar deliveries. The company targets scaling to 200 passenger cars in FY27

The long-term thesis is that India's massive rolling-stock replacement cycle — 5,000+ wagons and hundreds of passenger cars annually — creates a durable revenue stream. Key risks include order-execution delays, competition from state-owned BEML, and reliance on government procurement cycles. Always verify the latest order-book disclosures in quarterly filings.

Jupiter Wagons — Wagon and Container Growth Story

Jupiter Wagons Limited (NSE:JWL) has emerged as a significant private-sector wagon and container manufacturer. In Q3 FY26, revenue reached ₹899 crore with a 13% sequential increase. Jupiter Wagons reported an EBITDA margin of 14.6% in H1 FY25 — higher than Titagarh's 11.8% — and profit-after-tax growth of 25.1% year-on-year in H1 FY25. The company targets ₹8,000–10,000 crore revenue by FY28. As of June 2026, JWL trades near ₹282 (52-week range: ₹236–₹419), with a P/E of ~71x and market cap of ₹12,142 crore.

IRCON International — Domestic and Export EPC

IRCON International (NSE:IRCON) is an EPC contractor under the Ministry of Railways, executing rail, highway, and urban-infra projects domestically and internationally (Sri Lanka, Malaysia, Nepal, and others). In June 2025, IRCON received an EPC order worth ₹1,068 crore from East Central Railway, and shares rallied 15% on the news. The stock trades around ₹136 as of June 2026 (52-week range: ₹115–₹225), down ~39% year-on-year. Market cap is ₹12,561 crore at a P/E of ~20x — making it one of the more attractively priced PSU EPC plays on a headline basis, though earnings momentum needs monitoring.

Recent News & Market Triggers

- Union Budget FY27 (February 2026) allocated ₹2.78 lakh crore to Railways — highest ever — with ₹52,108 crore for rolling stock alone.

- Kavach Version 4.0 commissioned on 1,452 route km of key corridors; Indian Railways plans coverage of 18,000 km of high-density routes.

- Indian Railways achieved 99.6% broad-gauge electrification by early 2026, with just 269 km remaining — a near-complete milestone.

- Vande Bharat Sleeper launched in January 2026 (Howrah–Guwahati); 164 Vande Bharat services operating across the network as of December 2025.

- IRFC granted Navaratna status in March 2025, raising its operational autonomy and institutional investor attention.

- IRCON International won ₹1,068 crore EPC order from East Central Railway in June 2025.

- Station redevelopment capex for FY26: ₹12,120 crore allocated; ₹9,660 crore spent by December 2025, covering over 200 stations under ABSS.

- Multiple PSU railway stocks fell 40–55% from 2024 peaks by early 2026, prompting valuation reset discussions among institutional analysts.

Growth Drivers

- Record Government Capex: ₹2.78 lakh crore in FY27, sustaining multi-year order pipelines for EPC companies, wagon makers, and technology providers.

- Kavach Deployment: Safety spending on Indian Railways has reportedly tripled; Kavach coverage expansion to 24,400 km still in progress, benefiting system integrators and OEMs.

- Dedicated Freight Corridors (DFC): Fully operational Eastern and Western DFCs driving demand for high-capacity wagons and container-train operators like CONCOR.

- 100% Electrification: Near-complete broad-gauge electrification reduces fuel costs for Indian Railways, improving the economics of rail versus road freight.

- Station Redevelopment: 1,337 stations under ABSS; commercial development rights create revenue diversification for RLDA-linked and construction-sector participants.

- Export Orders: IRCON and RITES expanding international footprint in South Asia and Africa, adding revenue diversity beyond domestic capex cycles.

Risks Investors Should Know

- Valuation Premium: Many railway PSUs trade at P/E multiples well above historical averages even after 2024–25 corrections; earnings need to catch up to justify prices.

- Earnings Disappointment: RVNL, Titagarh, and others saw revenue/profit declines in FY25–FY26 quarters, indicating execution challenges or lumpy order recognition.

- Budget Dependency: Capex cycles are government-driven; any reduction in allocation (as seen in FY25 when the budget was flat at ₹2.55 lakh crore) can sharply derate stocks.

- Execution Delays: Monsoons, land acquisition, elections, and contractor shortages routinely delay railway projects, affecting quarterly revenue recognition.

- Policy and Regulatory Risk: IRCTC's ticketing-fee structure, IRFC's lending mandate, and CONCOR's haulage charges are all subject to government decisions.

- Competition: Private operators in container trains and wagon manufacturing are increasing market share (CONCOR market share fell from 74% in FY20 to 54% in FY26 in EXIM segment).

- Interest Rate Risk: IRFC's spread income can narrow if borrowing costs rise faster than its fixed-rate income stream from Indian Railways.

- PSU Governance: Management changes, government directives, and dividend policy uncertainty are inherent risks for all PSU-linked railway stocks.

Valuation Considerations

As of June 2026, railway stocks present a wide valuation spectrum. IRFC trades at ~17.7x P/E, IRCON at ~20x, and Texmaco Rail at ~22x — relatively modest for the sector. At the other end, RVNL (~59x P/E) and Jupiter Wagons (~71x P/E) remain expensive on a trailing earnings basis. IRCTC at ~30x commands a premium consistent with its monopoly franchise and zero-debt balance sheet.

Investors comparing these stocks should look beyond P/E to return on equity (IRCTC leads at ~37%), order-book-to-revenue ratios (RVNL at ~4.5x, Titagarh at ~3.3x consolidated), interest-coverage ratios, and free-cash-flow generation. All data points should be verified from the latest quarterly filings on NSE/BSE or BSE India's public disclosure portal.

Long-Term Outlook

India's 'Vision 2047' for railways envisages a world-class network with high-speed corridors, zero-emission operations, and fully automated safety systems. The National Rail Plan targets 200 kmph average freight speed and 160 kmph passenger speed. With Indian Railways spending ₹2.78 lakh crore annually and cumulative multi-year capex potentially exceeding ₹15 lakh crore by FY30, the revenue pool available to listed railway companies is substantial.

Long-term investors may find the best railway stocks for long-term investment among companies that combine strong order books with improving execution discipline and reasonable valuations. IRCTC's monopoly moat, IRFC's AAA financing franchise, and select execution PSUs with improving margins could merit positions in a diversified infrastructure portfolio — subject to a careful review of current prices, which have corrected meaningfully since 2024. The risk is that capex can be lumpy, political priorities can shift, and PSU stocks can remain range-bound for years despite strong sector narratives.

Frequently Asked Questions

Q: Which is the best railway stock for long-term investment in India?

A: There is no single 'best' answer as it depends on your risk appetite and investment horizon. IRCTC is often cited for its monopoly franchise and strong ROE, while IRFC appeals to income-oriented investors seeking quasi-bond stability. RVNL and BEML suit those seeking direct exposure to capex execution. Compare fundamentals on NSE/BSE and consult a SEBI-registered investment adviser before deciding.

Q: Is IRFC a good long-term investment?

A: IRFC's AAA rating, Navaratna PSU status (granted March 2025), and captive borrower (Indian Railways) make it a relatively low-risk financing institution. FY25 profit stood at ₹7,009 crore on revenue of ₹27,285 crore. However, the stock has fallen from its 2024 high of ~₹229 to around ₹95 in June 2026, reflecting earnings growth slowdown and broader PSU de-rating. Whether current prices represent value depends on your personal cost of capital and alternatives. This is not investment advice — please verify on NSE and consult an adviser.

Q: What is the impact of the Union Budget FY27 on railway stocks?

A: The FY27 budget allocated a record ₹2.78 lakh crore to railways, up ~10% from ₹2.52 lakh crore in FY26. Sub-segments include ₹52,108 crore for rolling stock, ₹36,721 crore for new rail lines, and large allocations for safety (Kavach). In February 2026, railway stocks rallied 3–4% on budget day before trimming gains, suggesting the market partially anticipated the allocation. Sustained order execution — not just allocation — ultimately drives earnings for listed companies.

Q: What is Kavach, and which stocks benefit?

A: Kavach is India's indigenously developed Automatic Train Protection (ATP) system that prevents signal-passing accidents and rear-end collisions. Version 4.0 has been commissioned on 1,452 route km as of early 2026, with plans to extend to 18,000 km on high-density routes. BEML, Siemens India, Kernex Microsystems (not individually analysed here), and various system integrators benefit from Kavach rollout contracts. Investors should track quarterly order disclosures for actual contract wins.

Q: How does Vande Bharat affect listed railway companies?

A: Vande Bharat trainsets — now 164 services running as of December 2025 — represent a premium rolling-stock segment. BEML manufactures coaches for Vande Bharat variants, while BHEL supplies traction systems. Titagarh Rail Systems is targeting passenger-car production scale-up. The Vande Bharat Sleeper (launched January 2026) and planned Vande Bharat Metro could expand the procurement pipeline further. Check each company's latest quarterly results for confirmed contract details.

Q: Are railway stocks PSUs or private companies?

A: The Indian railway stock universe includes both. PSUs include IRCTC, IRFC, RVNL, BEML, IRCON, RailTel, and CONCOR — all government-controlled with the Ministry of Railways or other ministries as the dominant shareholder. Private-sector companies include Titagarh Rail Systems and Jupiter Wagons. PSUs typically carry policy risk but benefit from guaranteed order flows; private players may have better capital efficiency but depend on competitive bidding.

Conclusion

India's railway sector is in the midst of a generational transformation — from Kavach-enabled safety to Vande Bharat premium travel and Dedicated Freight Corridors reshaping logistics economics. The best railway stocks for long-term investment in 2026 are those combining durable competitive advantages, visible order books, sound balance sheets, and reasonable entry valuations. IRCTC's ticketing monopoly, IRFC's AAA-rated financing franchise, RVNL's massive order pipeline, BEML's metro and rolling-stock positioning, and Titagarh's passenger-car pivot all represent distinct opportunities within this theme.

However, the 2024 PSU re-rating cycle served as a reminder that narrative alone does not sustain stock prices — earnings delivery does. Investors are encouraged to study the latest quarterly results, verify current valuations on NSE/BSE, diversify across sub-segments, and obtain advice from a SEBI-registered investment adviser tailored to their individual financial situation.