Finding the best renewable energy stocks in India has become one of the most-searched investment queries of 2025-2026, as the country's clean-energy build-out accelerates at a pace that few anticipated. India achieved its target of 50% installed non-fossil fuel capacity in June 2025 — five years ahead of schedule — and is now targeting 500 GW of non-fossil capacity by 2030, with solar alone expected to contribute nearly 300 GW of that figure.

By April 2026, India's cumulative renewable energy capacity stood at approximately 279 GW, comprising over 154 GW of solar and more than 56 GW of wind. Record capacity additions in FY26 — 34,955 MW of solar and 4,613 MW of wind — have given the sector strong momentum. Yet the investment opportunity is nuanced: while the macro story is compelling, several renewable energy stocks trade at significantly elevated valuations after years of outperformance, and execution, policy, and grid-integration risks are real.

Sector Overview

India's renewable energy ecosystem spans multiple sub-sectors, each with distinct business models and risk profiles. Utility-scale renewable generators convert sunlight and wind into electricity under long-term Power Purchase Agreements (PPAs). Solar PV module and cell manufacturers benefit from both domestic and export demand, buoyed by the Production Linked Incentive (PLI) scheme. Wind turbine manufacturers supply equipment to project developers. Hydro power PSUs provide stable, base-load generation. Transmission and power-finance companies are the enabling infrastructure.

The Union Budget 2026 allocated ₹600 crore to the Green Energy Corridor for 6,000 km of intra-state transmission, improving evacuation of renewable power. The government's VGF scheme has been expanded to support 30 GWh of standalone BESS (battery energy storage systems) by 2028, with ₹5,400 crore in funding expected to mobilise ₹33,000 crore in investment. Co-location mandates now require a minimum 10% BESS capacity alongside new solar installations — structurally linking storage deployment to every new solar tender.

The National Green Hydrogen Mission targets 5 million tonnes of annual green hydrogen production by 2030, with incentives under the SIGHT programme for both hydrogen production and electrolyser manufacturing — creating a downstream demand pipeline for renewable electricity.

Why This Theme Matters in 2026

India added a record 52,537 MW of total generation capacity in FY26, with nearly 75% from renewables. The government has committed to adding 50 GW of renewable capacity annually for the next five years. Meanwhile, peak power demand hit a record 270.82 GW in May 2026, creating an insatiable need for more generation. Both demand-side and supply-side dynamics are working in favour of the sector.

- India's renewable capacity reached ~279 GW by April 2026 — up from ~120 GW three years ago

- FY26 solar capacity addition: 34,955 MW — an all-time record

- PLI scheme: By June 2025, 18.5 GW of operational solar module capacity and 9.7 GW of cell manufacturing capacity established

- ALMM List-II for solar cells made mandatory from June 1, 2026 — boosting domestic manufacturers

- VGF scheme expanded for 30 GWh of BESS by 2028

- National Green Hydrogen Mission: 5 million tonne annual target by 2030

- India met 50% non-fossil installed capacity target in June 2025 — five years early

- ₹600 crore Budget 2026 allocation for Green Energy Corridor intra-state transmission

Key Stocks to Watch

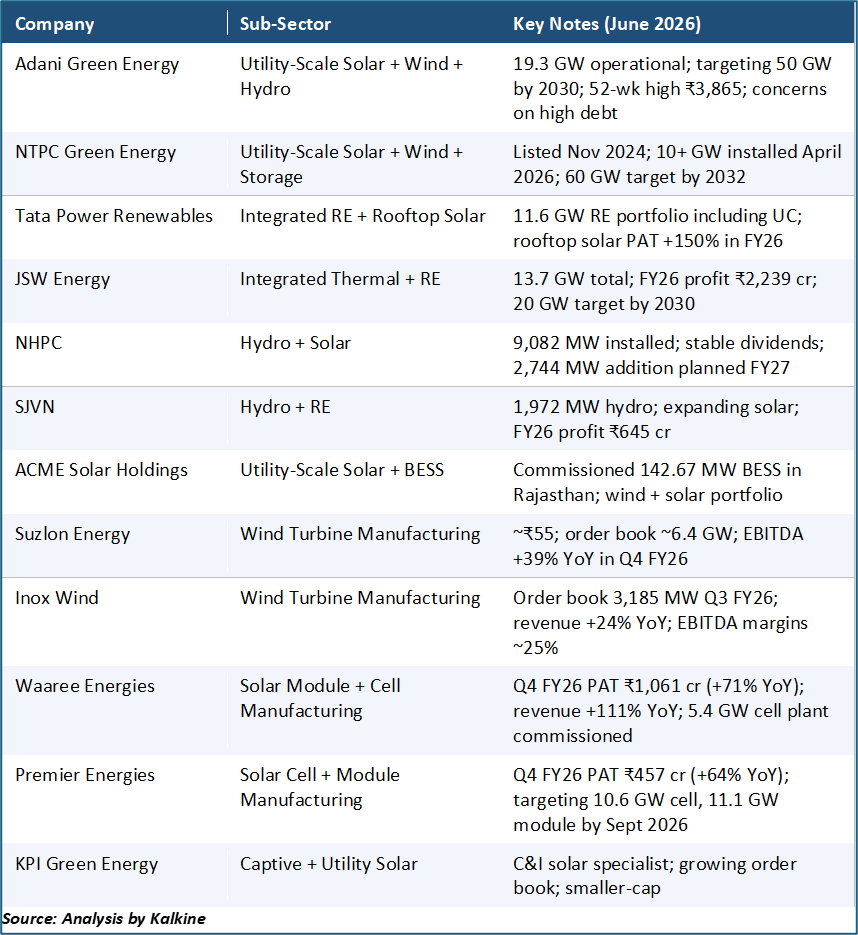

The table below lists major renewable energy stocks on Indian exchanges as of June 2026. Market cap and price data are indicative — verify current figures on NSE/BSE before transacting.

Company-by-Company Analysis

Adani Green Energy — India's Largest Renewable IPP

Adani Green Energy (NSE:ADANIGREEN) is India's largest utility-scale renewable independent power producer, with 19.3 GW of operational capacity at the end of FY26 — an addition of over 5 GW in FY26 alone, the highest single-year addition for any Indian renewable company. The company targets 50 GW by 2030, including a 5 GW pumped storage project. The stock hit a 52-week high of ₹3,865 in September 2025, before correcting to a 52-week low of ₹2,403 in January 2026. By mid-May 2026 the stock had gained approximately 29.7% year-to-date.

Waaree Energies — Solar Manufacturing Champion

Waaree Energies (NSE:WAAREEENER) is India's largest solar module manufacturer by capacity, and one of the clearest beneficiaries of the PLI scheme and the ALMM List-II mandate. In Q4 FY26, the company reported consolidated PAT of ₹1,061 crore (+71.4% YoY) on revenue from operations of ₹8,480 crore (+111.8% YoY) — outstanding growth driven by both domestic and export demand. The company inaugurated a 5.4 GW solar cell manufacturing facility in Gujarat in March 2025, and has also announced a 1.6 GW module line in the US. Waaree is now also raising funds to build a 20 GWh energy storage factory, indicating diversification into BESS. Valuation risk is significant; the stock has re-rated sharply. Retail investors should check current P/E and P/Sales multiples before entry.

Suzlon Energy — India's Wind Turbine Market Leader

Suzlon Energy (NSE:SUZLON) is India's dominant wind turbine manufacturer, with a current order book of approximately 6.4 GW (as of January 2026) — providing strong earnings visibility for the next two to three years. The company's Q4 FY26 EBITDA grew 39% YoY to ₹964 crore, though net profit dipped 5.7% to ₹1,114 crore due to higher depreciation. The stock was trading near ₹55 in June 2026, with a market cap of approximately ₹74,175 crore. Suzlon's order book has a healthy 66% mix of PSU and commercial & industrial clients.

Premier Energies — Solar Cell and Module Manufacturer

Premier Energies (NSE:PREMIERENE) is a vertically integrated solar manufacturer — one of six companies on the ALMM List-II approved for solar cells, with a combined approved capacity of 13 GW across the initial list. The company targets 10.6 GW of solar cell capacity and 11.1 GW of module capacity by September 2026. In Q4 FY26, consolidated PAT rose 64.4% YoY to ₹457 crore. Despite a ~32% stock correction in 2025, the company has shown fundamental improvement. The stock's premium valuation relative to earnings still warrants caution for fresh buyers.

NTPC Green Energy — The PSU Renewable Giant

NTPC Green Energy (NSE:NTPCGREEN) listed on BSE and NSE in November 2024 following a ₹10,000 crore IPO. By April 2026, the company surpassed 10 GW of installed renewable capacity — adding 4,175 MW in FY26 alone. The company aims to reach 60 GW by 2032, representing approximately 15% of India's total projected capacity. Being a subsidiary of NTPC gives it preferred access to land, grid connectivity, and government support. ACME Solar, another listed renewable player, commissioned 142.67 MW of BESS in Rajasthan — positioning it early in the energy storage cycle.

NHPC and SJVN — Hydro Power's Steady Foundation

NHPC (NSE:NHPC) and SJVN (NSE:SJVN) provide the green baseload that solar and wind cannot yet supply consistently. NHPC's 9,082 MW of installed capacity includes 24 hydropower stations and several solar and wind projects. FY26 profit was approximately ₹4,218 crore on revenue of ₹12,686 crore. The company plans to add 2,744 MW in FY27. SJVN operates 1,972 MW of hydro and is constructing 1,558 MW more, posting FY26 profit of ₹645 crore. Both are PSUs with dividend-paying histories, offering relatively lower risk profiles within the clean-energy space. New hydro project delays due to geological and regulatory factors remain the primary risk.

Inox Wind and Inox Green — Wind's Emerging Competitors

Inox Wind (NSE: INOXWIND) is Suzlon's primary domestic competitor in wind turbine manufacturing, with an order book of 3,185 MW in Q3 FY26. Revenue grew 24% YoY to ₹1,238 crore in Q3 FY26, with EBITDA rising 39% to ₹313 crore and EBITDA margins at ~25.2%. The stock was near ₹105-108 in early 2026 with a market cap of approximately ₹18,224 crore. Inox Green Energy Services (NSE: INOXGREEN) is the O&M (operations and maintenance) arm, offering a different risk-return profile. Both trade at elevated valuations relative to near-term earnings, reflecting growth expectations.

Recent News and Market Triggers

- June 2026: ALMM List-II for solar PV cells became mandatory on June 1, 2026 — direct benefit for domestic cell makers including Premier Energies and Waaree

- April 2026: NTPC Green Energy crosses 10 GW installed renewable capacity milestone

- April 2026: ACME Solar commissions 142.67 MW BESS in Rajasthan — one of India's largest standalone battery storage projects

- March 2025: Waaree Energies inaugurates 5.4 GW solar cell manufacturing facility in Gujarat

- Q4 FY26: Waaree PAT surges 71% YoY; Premier Energies PAT up 64% YoY — solar manufacturing boom continues

- FY26: India solar capacity addition hits 34,955 MW — a new annual record

- Budget 2026: ₹600 crore allocated for Green Energy Corridor; VGF scheme expanded for 30 GWh of BESS

- Suzlon secures 248.5 MW wind order from ArcelorMittal — industrial/C&I segment driving demand

Growth Drivers

- India's 500 GW non-fossil capacity target by 2030 requires 40-50 GW of annual additions from current 279 GW base

- PLI scheme for solar manufacturing has already established 18.5 GW of module and 9.7 GW of cell capacity by mid-2025

- ALMM List-II mandate (June 2026) channels Discom procurement to certified domestic cell manufacturers

- BESS co-location mandate with solar tenders creates structural demand for battery storage

- National Green Hydrogen Mission: 5 million tonne annual target by 2030 requires dedicated renewable generation

- C&I (commercial and industrial) captive renewable power demand growing rapidly as corporates set net-zero targets

- Green Energy Corridor and ₹9.15 lakh crore transmission investment reducing evacuation bottlenecks

- India achieved 42-fold increase in solar capacity since 2014 (from 2.82 GW to 154+ GW)

- Wind capacity expanding from 52 GW toward 100 GW target by 2029-30

- Pumped storage and BESS projects gaining policy momentum for grid stabilisation

Risks Investors Should Know

- Valuation risk: Many solar manufacturers and renewable IPPs trade at very high P/E and P/Sales multiples — even modest earnings misses can cause sharp corrections

- Adani Group-specific risks: Ongoing regulatory scrutiny and SEC probe create headline risk for Adani Green Energy investors

- Grid integration risk: Rapid renewable additions are outpacing grid evacuation capacity, leading to curtailment in some states

- Land acquisition and connectivity delays: Both factors have caused execution slippage for developers including JSW Energy and Tata Power

- Solar module price volatility: A global collapse in module prices (driven by Chinese overcapacity) can squeeze manufacturer margins

- Currency and import risk: Some solar inputs are still imported; rupee depreciation raises costs

- BESS technology risk: Large-scale battery storage is still maturing; cost overruns and performance shortfalls are possible

- Regulatory risk: PPA re-negotiation, tariff disputes, and policy reversals by state governments remain live risks

- Interest rate sensitivity: High-debt renewable developers are sensitive to borrowing cost changes; a rise in rates compresses equity returns

Valuation Considerations

The renewable energy sector in India trades at a significant premium compared to traditional industries, reflecting the long-duration growth potential embedded in the 500 GW target. However, this premium also means that any macro headwind — rising interest rates, policy changes, or project execution delays — can cause disproportionate stock-price corrections.

Solar manufacturers like Waaree Energies and Premier Energies have seen revenue and profit surge on the back of PLI incentives and domestic procurement mandates — but these tailwinds are partially one-time policy boosts. Sustainable margins will depend on technology competitiveness, export market access, and the ability to manage global solar module price cycles. Investors should not extrapolate recent revenue growth rates indefinitely.

Utility-scale renewable generators like Adani Green Energy carry significant debt because they invest capital today and recover it over 25-year PPA lifetimes. High-debt companies are especially vulnerable in rising-rate environments. NHPC and SJVN, being government-backed PSUs, offer lower financial leverage and more predictable dividend income, though their growth rates are also more modest.

Always cross-check P/E, EV/EBITDA, debt-to-equity, and return on equity metrics on NSE/BSE before entry. Consult a SEBI-registered investment adviser for personalised guidance.

Long-Term Outlook

The long-term structural case for India's renewable energy sector is among the strongest across all emerging market economies. India needs to more than double its current ~279 GW renewable base to reach 500 GW by 2030. Beyond 2030, the National Electricity Plan projects peak demand of 458 GW by 2032 and requires a total installed capacity well above 900 GW. Renewable energy, alongside storage and grid investment, must shoulder an increasing share of this.

For investors, the key question is not whether the sector will grow — it almost certainly will — but whether current stock prices already reflect too much optimism. A staggered, diversified approach covering generators, manufacturers, and power-finance companies may provide better risk-adjusted returns than concentrated bets on a single high-growth name. The green hydrogen opportunity, though early-stage, could become a significant additional revenue stream for companies with dedicated renewable generation capacity.

Frequently Asked Questions

Q: What is India's renewable energy capacity as of 2026?

A: India's cumulative renewable energy capacity reached approximately 279 GW by April 2026, including over 154 GW of solar, more than 56 GW of wind, and the balance from hydro, biomass, and small hydro. India achieved the milestone of 50% non-fossil installed capacity in June 2025, five years ahead of schedule.

Q: Which is the best renewable energy stock in India for long-term investment?

A: There is no single 'best' stock — each company carries different risk-return profiles. Adani Green Energy offers the highest scale ambition but also carries high debt and governance-related headline risk. NTPC Green Energy benefits from PSU backing and low cost of capital. Waaree Energies leads in solar manufacturing with strong recent earnings growth. NHPC provides stability and dividends. A diversified approach — across generators, manufacturers, and financiers — may be more prudent than concentrating in one name. Consult a SEBI-registered adviser.

Q: Is Suzlon Energy a good stock in 2026?

A: Suzlon Energy had an order book of approximately 6.4 GW in January 2026, providing strong earnings visibility. EBITDA grew 39% YoY in Q4 FY26 to ₹964 crore, though net profit dipped slightly due to depreciation. The wind turbine market is growing rapidly in India. However, the stock has re-rated significantly; at ~₹55 with a market cap of ₹74,175 crore, valuations price in substantial growth. Verify current fundamentals on NSE and NSE/BSE before investing.

Q: What is India's 500 GW renewable energy target?

A: India committed at COP26 in 2021 to achieving 500 GW of non-fossil fuel installed electricity capacity by 2030. Solar is projected to contribute ~300 GW, with the balance from wind, hydro, biomass, and other clean sources. To meet this target from the current ~279 GW base, India needs to add roughly 45-50 GW annually over the next four years — an enormous opportunity for equipment makers, developers, and financiers.

Q: What is the ALMM mandate and how does it affect solar stocks?

A: The Approved List of Models and Manufacturers (ALMM) List-II for solar PV cells became mandatory from June 1, 2026. This means that government-backed procurement must use cells from approved domestic manufacturers. Initially, six manufacturers including Premier Energies were approved, with a combined capacity of 13 GW. This mandate protects and benefits domestic cell manufacturers at the expense of imports, supporting stocks like Premier Energies and Waaree Energies.

Q: What are BESS and why do they matter for renewable energy stocks?

A: Battery Energy Storage Systems (BESS) store renewable electricity generated during peak production hours (daytime for solar, breezy periods for wind) and dispatch it when generation is low. India has expanded its VGF scheme to support 30 GWh of standalone BESS by 2028. Co-location mandates requiring 10% BESS alongside solar create recurring demand. ACME Solar's 142.67 MW BESS in Rajasthan is one of India's largest standalone projects. Waaree Energies is building a 20 GWh energy storage factory. This emerging segment could significantly expand the addressable market for several listed companies.

Conclusion

India's clean-energy transition is accelerating, and the best renewable energy stocks in India span a wide spectrum — from utility-scale generators like Adani Green Energy and NTPC Green Energy, to solar manufacturers like Waaree Energies and Premier Energies, to wind turbine leaders Suzlon and Inox Wind, to financing enablers REC and PFC. The country's 500 GW non-fossil target by 2030 and a record-setting pace of capacity addition provide a multi-year structural tailwind. However, many stocks already reflect rich valuations after sharp multi-year re-ratings. Investors should focus on fundamentals, compare valuations carefully, diversify across sub-sectors, and consult a SEBI-registered adviser before making any investment decision.