For income-seeking investors, PSU dividend stocks represent one of India's most reliable sources of equity-based income. Public Sector Undertakings — companies where the government holds more than 51% equity — are structurally incentivised to pay generous dividends because the Government of India itself is the largest shareholder and depends on those dividends as a meaningful source of non-tax revenue for the Union Budget. This creates a unique and durable alignment of interest between retail investors and the sovereign.

As of March 31, 2026, the Nifty PSE Index delivered a dividend yield of 2.96% — more than double the Nifty 50's 1.39% — underscoring the sector's stronger income profile. Several individual PSU stocks offer yields significantly above that aggregate, with Coal India, ONGC, IOC, BPCL, NMDC, SAIL, and the power finance NBFCs (REC, PFC) consistently among India's top dividend-paying listed companies. This article examines the mechanics, history, sustainability, and risks of PSU dividend investing in detail.

Sector Overview: Why PSUs Pay Such High Dividends

PSU dividend policy is shaped by two forces. First, government revenue dependence: the Union Budget each year includes significant non-tax revenue from dividends paid by CPSEs (Central Public Sector Enterprises). The Government of India regularly sets dividend payout guidelines for PSUs, and many Maharatna, Navratna, and Miniratna companies are required to pay minimum dividends linked to net profit or net worth. Second, cash flow abundance: companies like Coal India, ONGC, IOC, and BPCL generate enormous operating cash flows from commodity production, refining, and distribution — providing the fuel for high payouts even in moderate earnings years.

The result is a set of companies where payout ratios of 40–60% are common, multi-year dividend growth rates are positive, and interim dividends (paid during the year, before the annual final dividend) are routine. Coal India alone declared multiple interim dividends in FY26, with total declared dividends for the year reaching approximately ₹27 per share (verify final figures on NSE). Investors should note that dividend yields as quoted move inversely with share prices — a rising stock price reduces the yield even if the absolute dividend is unchanged.

Why PSU Dividend Stocks Matter in 2026

In 2026, several factors amplify the attractiveness of PSU dividend stocks for Indian retail investors. First, interest rate context: the Reserve Bank of India has been in a rate-cutting cycle, reducing returns on fixed deposits and debt instruments. PSU dividend yields of 4–8% compare favourably with bank FD rates for long-term investors (though equity involves capital risk that FDs do not). Second, dividend tax treatment: dividends are now taxable in the hands of investors at their applicable income tax slab rate — high-income investors should factor in post-tax yield when comparing income options.

Third, the government's own dividend incentive remains structurally intact. The FY27 disinvestment target was set at ₹80,000 crore — but India has historically under-delivered on disinvestment (FY26 receipts revised to ₹33,837 crore vs. ₹47,000 crore budgeted). This means the government continues to prefer regular dividend income from PSUs over asset sales, reinforcing the incentive for PSUs to maintain high payout ratios. GAIL's total dividend payout ratio for FY26 stood at 51.9% — described by the company as its highest ever — even as PAT fell 38% in a difficult year.

Company-by-Company Analysis

Coal India — The Dividend King of Maharatnas

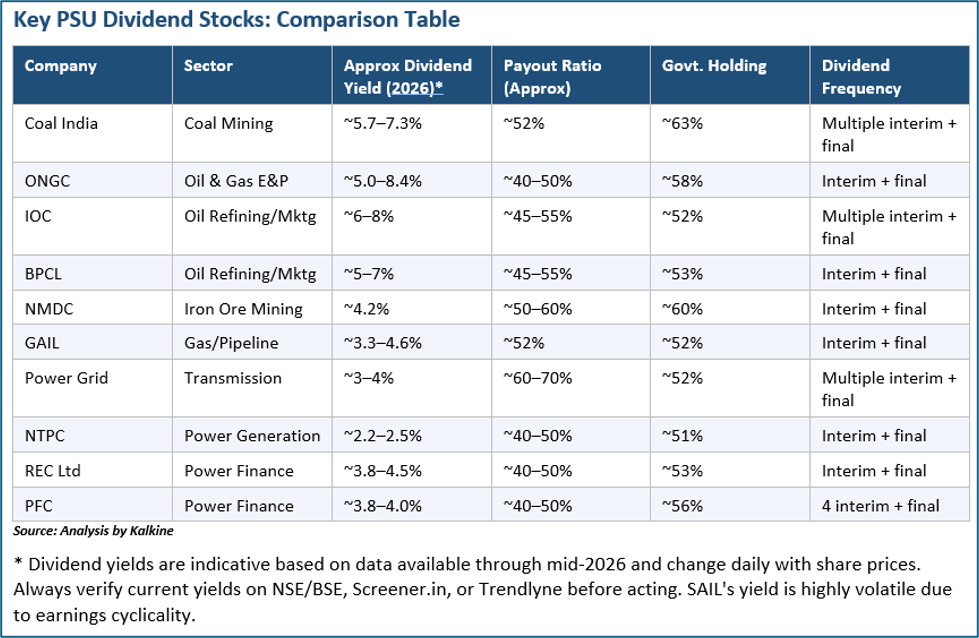

Coal India (NSE:COALINDIA) is widely regarded as the dividend king of India's PSU universe. It is the world's largest coal mining company and holds a near-monopoly on coal production in India, giving it pricing power and cash-generative assets. In FY26, Coal India declared total dividends per share of approximately ₹27 (TTM), with the most recent interim dividend of ₹5.50 per share declared with a record date in February 2026. The trailing twelve-month dividend yield has ranged between approximately 5.7% and 7.3% across measurement periods in early 2026.

The payout ratio is approximately 52%, meaning roughly half of earnings are returned to shareholders — a sustainable level that leaves room for investment. Coal India has a 5-year dividend growth rate of approximately 10.6% and a 3-year rate of 11.2%. FY26 EPS was ₹50.46 (down from ₹57.37 in FY25), reflecting some volume and pricing pressure, but the company maintained its payout commitment. Government holding stands at approximately 63%, meaning the government itself receives the bulk of Coal India's dividend cash flows — a powerful incentive to maintain the policy.

Key risk: Coal India faces a long-term structural challenge as India's energy transition accelerates the adoption of solar and wind power. While domestic coal demand remains robust in the near and medium term (supporting coal-fired power plants during the energy transition), investors with 10–20 year horizons should factor in declining coal's role in India's energy mix. Dividends depend on profitability, which can be impacted by government-mandated pricing, fuel supply agreements, and cost inflation.

ONGC — Upstream Income with Commodity Risk

Oil and Natural Gas Corporation (NSE:ONGC) is India's largest upstream oil and gas explorer and one of the most consistent dividend payers in the PSU space. ONGC paid an interim dividend of ₹6.25 per share in February 2026. Its dividend yield has been cited at approximately 5.0% in one measure and as high as 8.42% in another measure from earlier in 2026 (the difference reflects share price movement — higher yield is calculated at a lower price). The company's market cap as of June 2, 2026 was approximately ₹3.32 lakh crore, and its P/E ratio stood near 8.0x.

ONGC's high payout is enabled by its massive cash generation from domestic oil and gas production and its subsidiary stakes (including HPCL). The government holds approximately 58% and is the key beneficiary of ONGC's dividend stream. Key risk: ONGC's earnings are directly tied to crude oil prices. A sustained fall in Brent crude would reduce earnings and may compress future dividends. The company also faces subsidy-sharing obligations in certain government-determined pricing scenarios. Investors should track oil price trends and ONGC's quarterly results on the NSE.

IOC (Indian Oil Corporation) — Refining Income Powerhouse

Indian Oil Corporation (NSE:IOC) is India's largest downstream oil company and one of the Fortune 500's India representatives. IOC has a dividend yield in the approximately 6–8% range in recent periods, supported by its massive refining capacity, pan-India fuel distribution network, and petrochemicals business. IOC distributes multiple interim dividends during the year and a final dividend, reflecting strong operating cash flows. The government holds approximately 52% in IOC.

IOC's dividend sustainability is closely linked to refining margins (GRMs — gross refining margins). In years when crude oil is cheap and product prices are stable, IOC generates strong profits and can afford high payouts. In years when fuel price caps suppress retail prices even as crude rises, IOC's profitability — and therefore dividend capacity — can be squeezed. The company also has significant capex requirements for refinery upgrades and capacity expansion, which competes with dividends for free cash flow.

Power Grid Corporation — Regulated Yield, Predictable Payouts

Power Grid Corporation of India (NSE:POWERGRID) operates on a regulated return on equity (RoE) model — it earns a fixed regulated return on its approved capital expenditure, providing unusually high earnings visibility for an equity investor. This predictability supports a consistent and growing dividend: Power Grid declared a dividend of ₹3.25 per share in Q3 FY26 (record date February 9, 2026) and reported PAT of ₹4,160 crore for the quarter. The dividend yield has historically ranged between 3% and 4%.

Power Grid's five-year capex plan of ₹1.2 lakh crore for transmission infrastructure is a double-edged sword for dividend investors: it funds future regulated returns and earnings growth, but high capex also means high borrowing, which creates balance sheet leverage. The payout ratio is typically 60–70% of earnings, which is high but has been sustained by the regulated return model. Government holding stands at approximately 52%.

REC Ltd & PFC — Power Finance NBFCs with High Yields

REC Limited and Power Finance Corporation (PFC) are both Navratna PSU NBFCs that lend exclusively to the power sector — generation, transmission, and distribution companies across India. Both offer dividend yields in the 3.8–4.5% range and have been growing their loan books rapidly as India's power sector capex cycle accelerates. PFC declared four interim dividends in FY26, with the 4th interim at ₹3.25 per share.

The most significant corporate event for REC and PFC investors is the proposed merger announced in February 2026, which received in-principle board approval. The merged entity would have a combined loan book of approximately ₹11.5 lakh crore, creating India's largest infrastructure NBFC. The government has indicated that the merged entity will remain a 'government company' under the Companies Act. While the merger could create operational synergies, integration complexity and potential dilution should be monitored. Dividend sustainability for both entities depends on the quality of their power-sector loan books — exposure to stressed distribution companies (discoms) is a risk.

NMDC — Iron Ore Mining with Consistent Dividends

NMDC (National Mineral Development Corporation) is a fully government-owned entity under the Ministry of Steel and India's largest iron ore producer. The company has delivered 18.83% profit growth and a return on equity of approximately 24.35% in recent periods, and crossed 53 million tonnes in FY26 production with guidance of 60 MT for FY27. NMDC's dividend yield stands at approximately 4.19% and it maintains a payout ratio of 50–60% of earnings.

NMDC's high ROE and relatively asset-light mining model (compared to steel making) allow it to pay healthy dividends while funding growth capex. The company is also in the process of expanding its NMDC Steel subsidiary (the Nagarnar steel plant), which has turned profitable (PAT of ₹58.72 crore in FY26 on revenue of ₹13,641 crore) but is not yet a dividend payer.

GAIL India — Pipeline Income Under Pressure

GAIL India (NSE:GAIL) is India's dominant natural gas transmission company, operating over 16,000 km of pipelines, and also has liquefied natural gas (LNG) trading and petrochemical businesses. In FY26, GAIL's PAT fell 38% to ₹6,968 crore due to global LNG price headwinds and higher trading losses. Despite this, the board recommended a total dividend of ₹5.50 per share (₹0.50 final + ₹5 interim), and the payout ratio for FY26 was 51.9% — the highest-ever, according to the company.

GAIL's dividend yield ranges between approximately 3.3% and 4.6% across different market price points. The company commissioned approximately 2,000 km of new pipelines in FY26, including the Mumbai-Nagpur-Jharsuguda corridor, and invested ₹9,594 crore in capex. The commitment to high payout even in a down-earnings year signals management's dividend priority — but investors should note that a sustained earnings decline would eventually compress absolute dividend amounts even if payout ratios remain high.

NTPC — Lower Yield but Growing Dividend Trajectory

NTPC's (NSE:NTPC) dividend yield (approximately 2.2–2.5%) is lower than the oil and coal PSUs because the stock has re-rated significantly on the back of its renewable energy story. The company transferred ₹2,666 crore to the Ministry of Power as its second interim dividend for FY26. NTPC's 60 GW renewable energy target by 2032 requires massive capex, which constrains the absolute growth of free cash flow available for dividends in the near term. However, the long-term regulated return model ensures earnings grow alongside the asset base, supporting gradual dividend growth.

Recent News & Market Triggers

- Coal India FY26 total dividends: Approximately ₹27 per share declared over the trailing twelve months, with 5-year dividend CAGR of ~10.6%.

- GAIL highest-ever payout ratio: Despite PAT falling 38% in FY26, GAIL maintained a 51.9% dividend payout ratio — the highest in its history.

- PFC-REC merger in-principle approval (February 2026): Combined loan book ~₹11.5 lakh crore; both retain dividend-paying Navratna status as a government company post-merger.

- Power Grid Q3 FY26: PAT of ₹4,160 crore; dividend of ₹3.25 per share declared with record date February 9, 2026.

- ONGC interim dividend ₹6.25 per share paid February 2026; dividend yield near 5–8% range depending on share price.

- Equitymaster flags 4 PSU stocks with dividend yield above 5% (April 2026), including names from oil and metals sectors.

- Business Standard lists Coal India, ONGC, BPCL, IOC among 15 PSU stocks with dividend yields up to 7% (sourced April 2025 article, data relevant to FY26 cycle).

- Nifty PSE dividend yield at 2.96% vs Nifty 50 at 1.39% as of March 31, 2026 — PSU income premium intact.

Growth Drivers for PSU Dividend Sustainability

- Government Revenue Dependence: The Union Budget relies on PSU dividends as non-tax revenue; this is a structural incentive for sustained high payout ratios across Maharatna and Navratna PSUs.

- Cash-Generative Business Models: Coal India, ONGC, IOC, BPCL, and NMDC have asset-heavy, monopoly-like or oligopoly business models with strong recurring cash flows — the foundation of multi-decade dividend histories.

- Earnings Recovery in PSU Banks: As SBI, Bank of Baroda, and Canara Bank restore profitability post-NPA clean-up, their dividend capacities have grown, though their yields remain below the oil/mining PSUs.

- Power Sector Capex and Regulated Returns: Power Grid, REC, and PFC lend into or earn regulated returns from India's power infrastructure buildout — creating a reliable earnings and dividend stream.

- NMDC Volume Growth: FY26 iron ore production of 53 MT with 60 MT guidance for FY27 supports growing absolute dividends even if per-share yield is modest.

- GAIL Pipeline Expansion: Commissioning of 2,000 km of new pipelines in FY26 creates long-term recurring revenue supporting future dividends despite near-term LNG trading headwinds.

- Mandatory Minimum Payout Guidelines: CPSE guidelines require minimum dividend payouts linked to net profit or net worth, providing a floor for PSU dividend payments.

Risks Investors Should Know

- Dividends Are Not Guaranteed: Dividends are declared at the discretion of the board of directors and subject to annual profitability, regulatory approvals, and government guidance. Even high-payout PSUs can cut or skip dividends in loss-making years.

- Earnings Cyclicality: Oil PSUs (ONGC, IOC, BPCL) are vulnerable to crude price swings and refining margin compression. GAIL's 38% PAT decline in FY26 illustrates this risk. A sustained commodity downturn reduces absolute dividend capacity.

- Government Policy Risk: Governments may instruct PSUs to absorb fuel price subsidies (as oil marketing companies have done historically), suppress commodity pricing, or prioritise capex over dividends in national interest.

- Yield Illusion: A high stated yield does not mean a safe investment. SAIL's dividend yield can appear very high when the share price falls sharply — but a low share price may reflect genuine earnings risk, not just undervaluation.

- Dividend Taxation: From FY21 onwards, dividends are taxable in the hands of investors at their applicable income tax slab rate. High-income investors in the 30% bracket will receive a significantly lower post-tax yield than the headline figure.

- Capex vs. Payout Competition: Large capex programmes (NTPC's 60 GW renewables, GAIL's pipeline expansion, NMDC Steel) compete with dividends for free cash flow. Companies growing aggressively may moderate dividends over time.

- Energy Transition Risk for Coal: Coal India's dividend sustainability faces long-term structural pressure as India accelerates solar and wind power deployment. Near-term demand is robust, but the 10-year outlook for coal carries genuine uncertainty.

- Interest Rate Risk for Power Finance NBFCs: REC and PFC borrow from capital markets and on-lend to the power sector. Rising interest rates could compress net interest margins and reduce dividend capacity.

Valuation Considerations

Valuing dividend stocks requires looking beyond the yield headline. For PSU dividend investors, the key metrics are: dividend yield (current annual dividend divided by current share price), payout ratio (dividends as a percentage of net profit — a payout ratio above 80% may be unsustainable if earnings fall), dividend growth rate (has the company grown its absolute dividend consistently?), and free cash flow coverage (does operating cash flow comfortably cover the dividend payment after capex?).

Among the PSU dividend names: Coal India's payout ratio of ~52% with a 5-year CAGR of 10.6% represents a well-covered, growing dividend. ONGC at P/E ~8.0x with a 5% yield looks attractive on income-adjusted value metrics but requires a view on oil prices. Power Grid's regulated return model makes it one of the most predictable dividend growers. GAIL's FY26 ratio of 51.9% in a poor earnings year was a positive governance signal but investors should monitor whether earnings recover in FY27.

Long-Term Outlook

The long-term case for PSU dividend stocks rests on India's fundamental economic growth trajectory and the government's structural reliance on PSU income. As long as the government requires non-tax revenue and runs large-scale enterprises in strategic sectors, the incentive to maintain high payout ratios will persist. For income investors, a diversified portfolio of PSU dividend stocks — spanning coal, oil, power infra, and metals — could provide a meaningful income stream alongside capital appreciation potential.

However, selectivity is essential. Not all PSU dividend stocks are equal in quality. Coal India and Power Grid offer the most predictable dividend trajectories. ONGC and IOC offer higher yields but with commodity-earnings volatility. SAIL offers an occasionally spectacular yield but is highly cyclical. Investors should weight holdings based on their income stability requirement, tax situation, and long-term sector conviction. Given the uncertainty around energy transition and commodity cycles, a regular review of PSU dividend portfolios — at minimum annually — is advisable.

Frequently Asked Questions

Q: Which PSU stocks have the highest dividend yield in India in 2026?

A: Based on data available through mid-2026, Coal India, ONGC, IOC, BPCL, NMDC, and SAIL feature among the highest dividend-yielding PSU stocks, with yields ranging from approximately 4% to over 7% depending on the current share price. Yields fluctuate daily; always verify current figures on NSE, BSE, Screener.in, or Trendlyne.

Q: Why do PSU stocks pay high dividends?

A: PSU stocks pay high dividends primarily because the Government of India is the largest shareholder and relies on PSU dividends as non-tax revenue for the Union Budget. CPSE guidelines mandate minimum dividend payouts tied to profitability. Additionally, companies like Coal India and ONGC generate large operating cash flows relative to their reinvestment needs, making high distribution ratios sustainable.

Q: Is Coal India the best PSU dividend stock?

A: Coal India is widely considered one of India's most consistent PSU dividend stocks, with a 5-year dividend CAGR of approximately 10.6% and a payout ratio of around 52%. However, it faces long-term structural risk from India's energy transition away from coal. Whether it is the 'best' depends on individual risk tolerance, investment horizon, and views on coal demand. This article does not recommend any specific stock — please consult a SEBI-registered adviser.

Q: Are PSU dividends taxable in India?

A: Yes. From FY2020-21 onwards, dividends received by investors are taxable in their hands at their applicable income tax slab rate, with Tax Deducted at Source (TDS) applicable above ₹5,000 per year per company. High-income investors in the 30% bracket should calculate post-tax dividend yield for accurate income comparison. Consult a tax adviser for your specific situation.

Q: What does the PFC-REC merger mean for dividend investors?

A: In February 2026, PFC and REC gave in-principle approval for a proposed merger. The merged entity is expected to remain a government company, potentially creating India's largest infrastructure NBFC with a combined loan book of ~₹11.5 lakh crore. For dividend investors, the key question is whether the merger preserves or enhances dividend capacity. Until merger terms are finalised, investors should track both companies' quarterly results and any regulatory approvals. The merger process may take 12–24 months to conclude.

Q: How do I calculate the real dividend yield of a PSU stock?

A: Dividend yield = (Annual dividend per share / Current market price per share) × 100. For example, if Coal India declares ₹27 in total dividends over a year and the current share price is ₹400, the yield is 6.75%. If the share price rises to ₹450 with the same ₹27 dividend, the yield falls to 6.0%. Always use the trailing twelve-month total dividend and the current share price for an up-to-date yield figure. Check NSE/BSE or financial portals like Trendlyne, Screener.in, or Tickertape for real-time yield data.

Q: Is GAIL still worth holding for dividends after its FY26 profit drop?

A: GAIL's PAT fell 38% in FY26 to ₹6,968 crore due to LNG trading losses and global headwinds, yet the company maintained a 51.9% payout ratio — its highest ever. This signals management commitment to dividend policy even in difficult years. However, if earnings do not recover in FY27, sustaining a high absolute dividend amount becomes more challenging. Investors should monitor GAIL's Q1 FY27 results, global LNG prices, and pipeline utilisation trends before drawing conclusions on dividend sustainability.

Conclusion

PSU dividend stocks occupy a unique position in India's equity income landscape. Backed by government ownership, mandated by CPSE payout guidelines, and fuelled by cash-generative monopoly or oligopoly business models, companies like Coal India, ONGC, IOC, Power Grid, NMDC, and GAIL offer some of the most attractive dividend yields available in India's listed equity market. The Nifty PSE's 2.96% aggregate yield — nearly double the Nifty 50 — captures only part of the story; individual high-yield names offer substantially more to income-focused investors.

That said, PSU dividends are not a substitute for fixed-income instruments in terms of capital safety. Earnings cyclicality, commodity price risk, government policy interference, energy transition challenges, and dividend taxation all need to be factored into any income strategy built around PSU stocks. A thoughtful, diversified approach — combining stable regulated dividend payers (Power Grid, NTPC, IRFC) with higher-yield but more volatile names (Coal India, ONGC, IOC) — may offer the best balance for most retail investors.