Railway stocks under ₹500 attract strong interest from Indian retail investors who want exposure to the country's infrastructure boom without committing large per-share capital. With Indian Railways receiving a record ₹2.78 lakh crore capex budget in FY27 — covering rolling stock, new lines, safety (Kavach), electrification, and station redevelopment — several listed railway companies offer entry points below the ₹500 mark as of June 2026.

However, a word of caution is warranted upfront. Many of these stocks fell 40–65% from their 2024 highs to their June 2026 prices, driven by earnings disappointments, flat FY25 budget allocations, and a broad PSU de-rating cycle. A share price below ₹500 does not automatically make a stock inexpensive in valuation terms — P/E ratios, order-book execution, and debt profiles matter far more than absolute price.

This article covers the key railway stocks currently (as of our research, early June 2026) trading below ₹500 on the NSE, their business profiles, fundamentals, and the risks involved. All prices must be independently verified on NSE/BSE as they are subject to daily movement.

Sector Overview

The Indian listed railway sector spans financiers (IRFC), execution PSUs (RVNL, IRCON), rolling stock and wagons (Texmaco Rail, Jupiter Wagons), ICT and telecom infra (RailTel), logistics (CONCOR), and passenger services (IRCTC). As of June 2026, the ₹500-and-below segment covers most of these sub-sectors except passenger services (IRCTC at ~₹518) and rolling-stock specialists like BEML (~₹1,747) and Titagarh Rail Systems (~₹865).

After a spectacular multi-year rally in 2022–2024 driven by government capex enthusiasm and PSU re-rating, the sector corrected sharply in 2024–2025. A flat railway budget in FY25 (held at ₹2.55 lakh crore), combined with weak Q3/Q4 FY25 and Q1/Q2 FY26 earnings across multiple names, triggered the correction. The FY27 budget resumption of growth — rising to ₹2.78 lakh crore — has provided a partial recovery catalyst in select names.

Why Railway Stocks Matter in 2026

India's railways are undergoing their most ambitious upgrade in history. The network electrification rate has hit 99.6% on broad gauge — with just 269 km remaining. Kavach Automatic Train Protection Version 4.0 has been commissioned on 1,452 route km, with 18,000 km of high-density routes targeted for coverage. The Vande Bharat Sleeper was launched in January 2026, and 164 Vande Bharat services operated as of December 2025. Over 1,337 stations are being redeveloped under the Amrit Bharat Station Scheme.

For retail investors with limited per-share budgets, railway stocks under ₹500 offer a meaningful entry into this structural theme. The key is to focus on balance-sheet strength, order-book visibility, management track record, and reasonable entry valuations — rather than solely on the per-share price tag.

Company-by-Company Analysis

IRFC — AAA-Rated Financier at Decade-Low Valuations

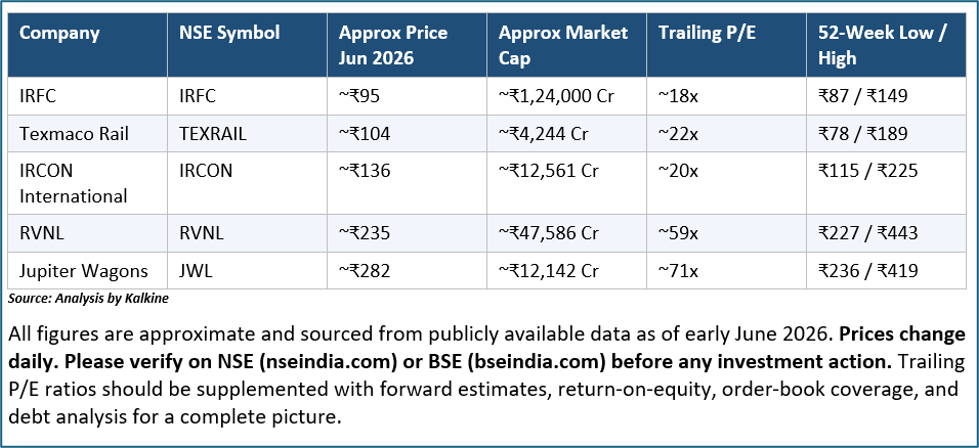

Indian Railway Finance Corporation (NSE:IRFC) is a dedicated NBFC that borrows from capital markets and on-lends exclusively to Indian Railways for rolling stock and infrastructure. Elevated to Navaratna PSU status in March 2025, IRFC holds an AAA credit rating — the highest possible — reflecting the near-zero credit risk of its sole borrower (the Ministry of Railways). As of June 9, 2026, IRFC trades near ₹94–95, down from its all-time high of ₹229 — a correction of roughly 58%. The 52-week range is ₹87–₹149.

FY25 revenue was ₹27,285 crore and net profit ₹7,009 crore. The P/E ratio is approximately 17.7x, and the dividend yield stands near 2.6% (dividend declared at ₹1.05/share in March 2026). Total assets in FY25 crossed ₹4.88 lakh crore — a figure that underscores the scale of this institution. The primary risk is spread compression: if IRFC's borrowing costs rise faster than its fixed-income spread from Indian Railways, margin could shrink. Also note that IRFC's business model is essentially a pass-through; it doesn't generate operating leverage the way an equity business does.

Texmaco Rail & Engineering — Wagon Manufacturer at Trough Valuation

Texmaco Rail & Engineering (NSE:TEXRAIL) manufactures railway wagons, freight bogies, and steel castings, and is one of India's oldest private wagon makers. As of June 2, 2026, the stock trades at approximately ₹104 — down from its 52-week high of ₹189 and a peak of ~₹296 in July 2024, implying a 65% correction from peak. Market cap is ~₹4,244 crore and trailing P/E is ~22x. The 52-week low was ₹78. The company has given a 3-year return of about 20%, indicating long-term appreciation despite recent volatility.

Texmaco benefits from India's wagon-procurement cycle: Indian Railways orders tens of thousands of wagons annually to meet freight targets. The Dedicated Freight Corridors require specialised high-capacity wagons, for which Texmaco is a key domestic supplier. Risks include competition from Titagarh, Jupiter Wagons, and new entrants; lumpy quarterly revenue tied to dispatch schedules; and dependence on government tender pricing. Verify current order book disclosures in quarterly filings on NSE.

IRCON International — Value-Priced EPC with Global Reach

IRCON International (NSE:IRCON) is a Ministry of Railways EPC contractor executing rail, road, and urban-infrastructure projects in India and abroad. As of June 9, 2026, IRCON trades at approximately ₹136 (52-week range: ₹115–₹225), down ~39% year-on-year. Market cap is ₹12,561 crore and trailing P/E is ~20x — one of the more moderate valuations in the railway PSU space. In June 2025, IRCON bagged an EPC contract worth ₹1,068 crore from East Central Railway.

IRCON's international presence (Sri Lanka, Malaysia, Nepal, Mozambique, Algeria) provides revenue diversification beyond domestic budget cycles. FY25 and FY26 earnings data should be verified from the company's quarterly filings on NSE. Risks include project execution delays, geopolitical risks in international markets, and working-capital intensiveness typical of large EPC contracts. At ~20x P/E, it is relatively attractively valued compared to RVNL (~59x), though absolute value depends on earnings trajectory.

RVNL — Massive Order Book, Compressed Margins

Rail Vikas Nigam Limited (NSE:RVNL) is a Navaratna Schedule-A PSU and the largest railway project execution entity in India. Its order book stands at approximately ₹90,000 crore, providing 4–5 years of revenue visibility at FY25 run-rate. However, FY25 revenue declined 8.9% to ₹19,923 crore and net profit fell 17% to ₹1,281 crore. Q4 FY26 net profit reportedly declined ~59% year-on-year, raising concerns about margins and execution pace.

As of June 9, 2026, RVNL trades near ₹235 (52-week range: ₹227–₹443), down 47% in one year. Despite the correction, the trailing P/E remains ~59x — high given the earnings trajectory. RVNL has guided for ₹21,000–22,000 crore revenue in FY26 and 15–20% growth in FY27. The receivables issue from KRCL (₹1,190 crore) and competitive pressure on margins from private bids are near-term risks. Long-term investors should monitor quarterly execution pace against order book, margin recovery, and dividend history.

Jupiter Wagons — High-Growth Wagon Maker with Premium Valuation

Jupiter Wagons Limited (NSE:JWL) is a private-sector manufacturer of freight wagons and containers that has scaled rapidly in the past three years. Q3 FY26 revenue reached ₹899 crore (13% sequential growth), and H1 FY25 EBITDA margin was 14.6%. The company targets ₹8,000–10,000 crore in revenue by FY28. As of June 2026, JWL trades near ₹282 (52-week range: ₹236–₹419), with a P/E of ~71x and market cap of ₹12,142 crore.

RailTel Corporation — Digital Backbone of Indian Railways

RailTel Corporation of India (NSE:RAILTEL) is a 'Mini Ratna' (Category-I) PSU that operates India's largest neutral telecom infrastructure along railway routes. It provides broadband, data centre, and managed ICT services to Indian Railways, government entities, enterprises, and consumers. In Q3 FY26, revenue rose 19% year-on-year to ₹913 crore, though standalone net profit dipped 4% to ₹62 crore. Market cap as of June 8, 2026 is approximately ₹10,053 crore, with the stock at ~₹313, P/E ~70x.

RailTel's unique positioning along the entire rail right-of-way — spanning 60,000+ route km of optical fibre — makes it a critical digital-infrastructure play beyond pure railway capex. Revenue diversification into data centres and smart city projects adds resilience. Risks include revenue concentration in government customers, high P/E relative to profit growth, and competition from private telecom providers in enterprise ICT. The stock fell from a peak of ~₹618 to ~₹313 — a 49% decline — by mid-2026, partly resetting the valuation.

Recent News & Market Triggers

- Union Budget FY27 raised railway capex to a record ₹2.78 lakh crore (vs ₹2.52 lakh crore in FY26), triggering a 3–4% single-day rally in IRFC, RVNL, RailTel, and IRCON on February 1, 2026.

- Railway stocks fell 40–65% from 2024 peaks by early 2026.

- IRFC granted Navaratna PSU status in March 2025, expanding operational and financial autonomy.

- Kavach Version 4.0 commissioned on 1,452 route km in January 2026; the government aims to cover 18,000 km of high-density rail routes.

- Vande Bharat Sleeper launched January 2026 (Howrah–Guwahati); 164 Vande Bharat services running as of December 2025.

- IRCON received EPC order worth ₹1,068 crore from East Central Railway in June 2025; stock rallied 15% on the news.

- RVNL Q4 FY26 net profit reportedly declined ~59% year-on-year, raising investor concerns about margin recovery.

- Texmaco Rail & Engineering stock at ~₹104, down 65% from its ₹296 peak in July 2024.

- RailTel Q3 FY26 revenue grew 19% YoY to ₹913 crore, though profit growth lagged due to higher execution costs.

- Indian Railways achieved 99.6% broad-gauge electrification by early 2026, with just 269 km remaining.

Growth Drivers

- Record Capex at ₹2.78 Lakh Crore: Highest-ever FY27 budget allocation ensures sustained order intake for execution PSUs like RVNL and IRCON.

- Rolling Stock Replacement Cycle: ₹52,108 crore allocated in FY27 for rolling stock — benefiting wagon makers (Texmaco, Jupiter Wagons) and coach manufacturers (BEML, Titagarh).

- Kavach Safety Network: Large-scale ATP deployment contract pipeline benefits system suppliers and integrators over FY26–FY30.

- Freight Growth via DFCs: Eastern and Western Dedicated Freight Corridors operational; India targeting 3 billion tonnes annual freight by 2030, driving wagon demand.

- Digital Railways (RailTel): Optical fibre, data centres, smart stations, and digital ticketing represent growing revenue streams for RailTel beyond core telecom.

- International Expansion (IRCON, RVNL): South Asian and African rail infrastructure contracts provide revenue diversification for EPC PSUs.

- Metro Rail Expansion: 20+ city metro network expansion creates sustained demand for rolling stock, signalling, and ICT infrastructure.

- Electrification Completion: Near-100% electrification reduces Indian Railways' energy cost, improving its ability to invest in further capex and rolling stock upgrades.

Risks Investors Should Know

- Lower Price ≠ Better Value: RVNL at ₹235 trades at ~59x trailing P/E; Jupiter Wagons at ₹282 trades at ~71x. Absolute price is not a measure of cheapness — always evaluate P/E, P/B, and earnings growth.

- Sustained Earnings Weakness: Multiple names (RVNL, Titagarh, IRCON) have reported earnings declines in FY25–FY26 quarters. Recovery timing is uncertain.

- Budget and Policy Risk: Any reduction in railway capex (as happened in FY25 when allocation stayed flat) can sharply de-rate stocks and reduce order inflow for EPC companies.

- Execution Delays: Monsoons, land acquisition disputes, contractor availability, and elections regularly push project timelines, delaying revenue recognition.

- Interest Rate Risk for IRFC: A rising interest-rate environment could compress IRFC's net spread, the primary driver of its earnings.

- Competition in Wagons: Texmaco Rail and Jupiter Wagons face competition from each other and from Titagarh, creating pricing pressure in tender bids.

- CONCOR Market Share Erosion: CONCOR's market share in container logistics fell from 74% (FY20) to ~54% (9M FY26) due to private container operators — a structural risk.

- PSU Governance Risks: Management changes, government directives on dividends, and policy mandates can affect PSU profitability and shareholder returns unpredictably.

Valuation Considerations

Among railway stocks under ₹500, the valuation picture varies dramatically. IRFC at ~18x P/E and IRCON at ~20x look the most modestly priced on trailing earnings, while RVNL at ~59x and Jupiter Wagons at ~71x still trade at premium multiples despite significant stock-price corrections. This paradox occurs because earnings — the denominator — also declined sharply, keeping the P/E ratio elevated even as the share price fell.

Long-Term Outlook

The case for railway stocks under ₹500 as long-term holdings depends on whether the earnings correction of 2025–2026 is temporary or structural. For companies like IRFC (where the earnings model is formulaic and government-backed), IRCON (where order wins are picking up), and RVNL (where order-book visibility remains strong despite near-term margin pressure), the correction may represent a better entry opportunity than the frothy 2023–2024 period.

For Texmaco Rail and Jupiter Wagons, the outlook hinges on the wagon-procurement cycle and execution of the DFC freight growth thesis. RailTel's digital-infrastructure revenue stream adds resilience but its earnings growth must accelerate to justify the current premium multiple. CONCOR faces structural competition pressure even as its logistics network remains strategically vital.

Retail investors are advised to dollar-cost-average into preferred names rather than timing the market, diversify across at least two or three sub-segments (e.g., financing + execution + rolling stock), and maintain a 3–5 year investment horizon consistent with government capex cycles.

Frequently Asked Questions

Q: Which railway stocks are currently under ₹500 on NSE?

A: As of early June 2026, IRFC (~₹95), Texmaco Rail (~₹104), IRCON International (~₹136), RVNL (~₹235), Jupiter Wagons (~₹282), RailTel (~₹313), and CONCOR (~₹476) were all trading below ₹500 on the NSE. These prices are approximate and subject to daily change. Please verify current prices on nseindia.com or bseindia.com before making any investment decision.

Q: Is a railway stock under ₹500 the same as a cheap or undervalued stock?

A: No. Absolute share price has no direct relation to valuation. RVNL at ₹235 trades at ~59x trailing earnings — that is not cheap by conventional metrics. Jupiter Wagons at ₹282 has a P/E of ~71x. A stock's value depends on its earnings growth, order-book quality, balance-sheet strength, and price relative to those fundamentals — not its nominal rupee price. Always calculate the P/E, P/B, and return on equity before judging affordability.

Q: Why have most railway stocks fallen 40–65% from their 2024 highs?

A: The 2022–2024 rally in railway PSUs was driven by a re-rating of government capex beneficiaries; stocks often ran far ahead of actual earnings delivery. When the FY25 Union Budget kept railway capex flat at ₹2.55 lakh crore (below expectations), earnings disappointments at RVNL, IRCON, Titagarh, and others compounded the de-rating. The resulting 40–65% corrections brought valuations down — but some stocks remain expensive on a trailing-earnings basis even after the fall.

Q: Is IRFC a safe investment for conservative investors?

A: IRFC's AAA rating, monopoly borrower (Indian Railways / MoR), and Navaratna PSU status make it one of the lower-risk equity instruments within the railway sector. Its FY25 net profit of ₹7,009 crore is stable and predictable. However, no equity is completely 'safe' — the stock has fallen from ₹229 to ~₹95, and interest-rate and policy risks remain. Dividends (yield ~2.6%) provide some income. This is not a recommendation; investors should verify on NSE and consult an adviser.

Q: What is CONCOR's business and why is it just under ₹500?

A: Container Corporation of India (CONCOR, NSE: CONCOR) is the dominant rail-based container logistics operator, managing 54.35% of the overall container-freight market. It operates Inland Container Depots (ICDs) and port-linked terminals. The stock traded near ₹476 in late May 2026, reflecting a 30%+ decline from its 52-week high of ₹652. Its market share in EXIM containers has fallen from 74% (FY20) to ~54% (9M FY26) due to private competition. Verify the current price on NSE before any transaction as it may move above or below ₹500.

Q: Does a stock split affect railway stocks' ₹500 status?

A: Yes. Stock splits reduce the face value and share price while increasing share count proportionally. Some railway stocks that are above ₹500 today could fall below ₹500 after a split without any change in the company's underlying value or market cap. Always verify whether a recent split explains the current price level, and adjust your per-share analysis accordingly.

Q: What is the best railway stock under ₹500 to invest in today?

A: This article cannot recommend any specific stock as 'best' because the answer depends on your personal risk tolerance, investment horizon, portfolio diversification, and financial goals. IRFC may suit income-seeking conservative investors; IRCON may appeal to value-oriented investors comfortable with EPC execution risk; RVNL suits those with high conviction in long-duration order-book execution. Please consult a SEBI-registered investment adviser and verify current figures on NSE/BSE before investing.

Conclusion

India's railway sector offers one of the most visible government capex themes for the next five years, and several compelling railway stocks under ₹500 — including IRFC, IRCON, RVNL, Texmaco Rail, Jupiter Wagons, and RailTel — provide accessible entry points for retail investors as of June 2026. The sector's record FY27 budget, Kavach deployment, Vande Bharat expansion, near-complete electrification, and metro network build-out create multi-year demand for listed railway companies.

That said, the 2024–2026 correction is a reminder that even well-supported sectors can generate large drawdowns when earnings disappoint or valuations run ahead of fundamentals. Investors should focus on earnings quality, order-book coverage, balance-sheet strength, and entry valuations — not just share price. Verify all prices and financials on NSE/BSE, diversify across sub-segments, and consult a SEBI-registered investment adviser before committing capital.