Finding the Adani stock with maximum growth potential has become one of the most searched questions among Indian retail investors in 2026. With over ten companies listed on NSE and BSE under the Adani banner — spanning thermal power, renewable energy, port logistics, transmission, city gas, cement, agri-foods, and media — the group presents both compelling opportunities and concentrated risks.

This article provides a structured, data-driven comparison of the major listed Adani Group companies as of June 2026. We examine each company's business model, recent financial performance, expansion plans, debt position, valuation, and key risks — giving Indian retail investors the framework to make an informed decision. Nothing here constitutes investment advice; always verify data on NSE/BSE and consult a qualified financial adviser.

Sector Overview: The Adani Group in 2026

The Adani Group, led by Gautam Adani, is India's largest infrastructure and energy conglomerate by market capitalisation. In FY2026, the group reported record capital expenditure of approximately Rs 1.53 lakh crore — the highest ever by any Indian corporate in a single year. Its businesses span ports, airports, power generation, renewable energy, power transmission, smart metering, city gas distribution, cement, edible oils, and media.

Why This Matters in 2026

India's infrastructure cycle is in full swing. The government's National Infrastructure Pipeline, push for 500 GW of renewable energy by 2030, expansion of port capacity, smart grid modernisation, and rapid urbanisation all create structural tailwinds that directly benefit multiple Adani subsidiaries. With the legal overhang partially resolved and credit ratings stabilising, institutional and retail investor interest in Adani stocks has revived sharply in 2026.

- India targets 500 GW renewable energy capacity by 2030 — Adani Green is a primary beneficiary.

- Power deficit concerns and industrial growth are driving thermal power demand — supporting Adani Power.

- Container traffic growth of 20% YoY at APSEZ reflects India's export competitiveness.

- Smart metering rollout (300+ million meters mandated nationally) gives AESL a multi-year order runway.

- Cement consolidation underway as Ambuja absorbs ACC and Orient Cement into a single platform targeting 155 MTPA.

Company-by-Company Analysis

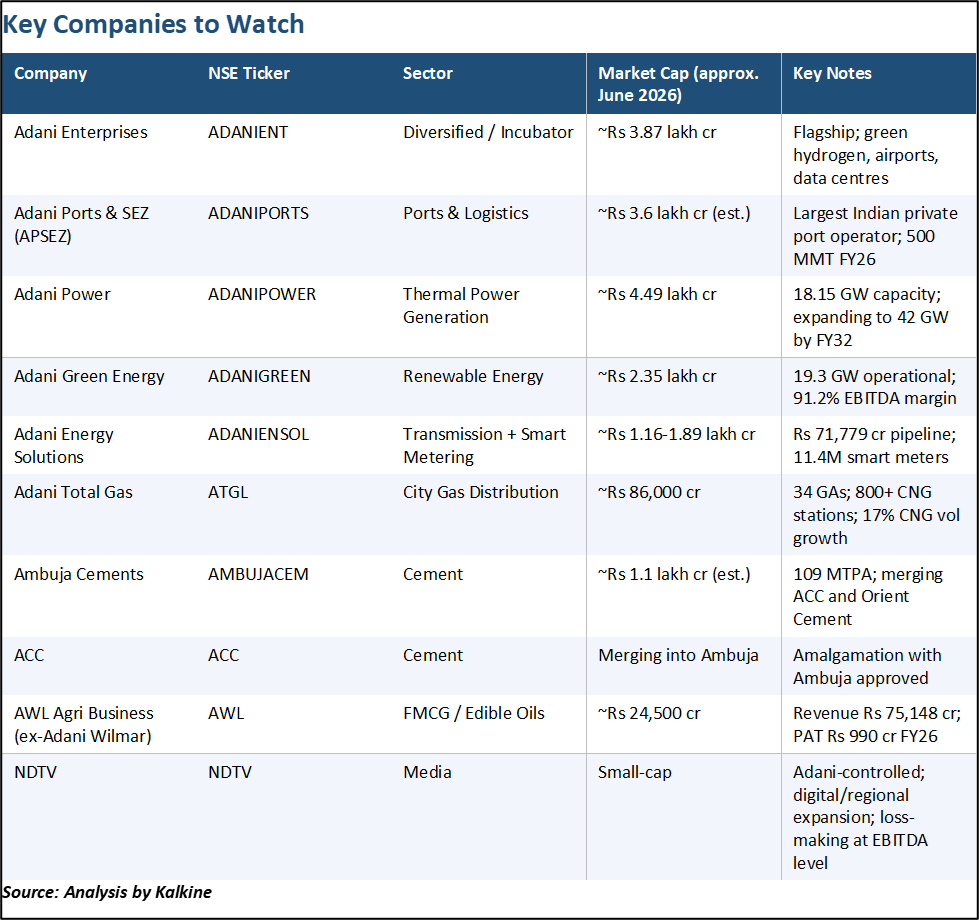

Adani Enterprises Limited (ADANIENT)

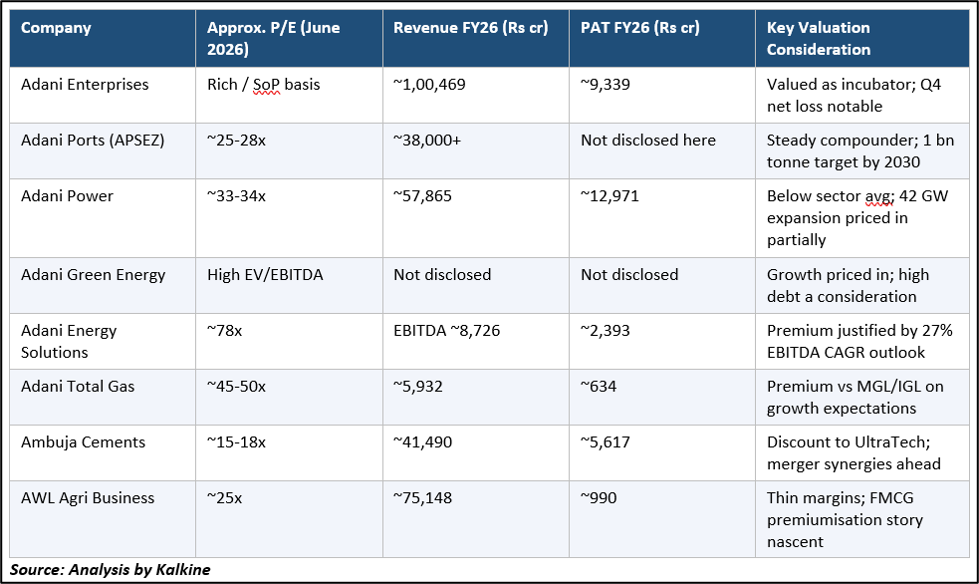

Adani Enterprises (AEL) (NSE:ADANIENT) is the group's flagship incubator, nurturing new businesses until they are spun off or scaled. Its current focus areas include green hydrogen production, data centres, airports (through Adani Airport Holdings), roads, and defence. FY26 revenue was approximately Rs 1,00,469 crore (up ~2.6% YoY) and full-year net profit rose 31.5% to approximately Rs 9,339 crore. The company did report a Q4 FY26 consolidated net loss of Rs 220 crore amid higher capex-linked charges.

The stock trades at around Rs 3,048 (as of early June 2026) with a market cap of approximately Rs 3.87 lakh crore. AEL is best viewed as a portfolio of emerging ventures — its value creation thesis depends on successful monetisation of new businesses. The valuation is accordingly rich. The company announced a dividend of Rs 1.30 per share for FY26 (ex-date June 12, 2026).

Adani Ports & SEZ — APSEZ (ADANIPORTS)

APSEZ (NSE:ADANIPORTS) is India's largest private port operator and is increasingly a pan-India logistics platform. In FY26, it crossed the milestone of 500 million metric tonnes (MMT) of cargo handled — a first for any Indian port operator. Full-year revenue surpassed the Rs 38,000 crore guidance, and Q4 FY26 revenue rose 26.5% YoY to Rs 10,738 crore. Net profit for Q4 grew 10.4% YoY.

The company's medium-term roadmap targets one billion tonnes of cargo by 2030, doubling current volumes. International acquisitions including the Colombo West Terminal and the North Queensland Export Terminal are diversifying its revenue mix. The net debt-to-EBITDA stands at approximately 1.8x — among the most conservative in the Adani portfolio. Cargo volumes in May 2026 rose 16% YoY, signalling continued momentum.

Adani Power Limited (ADANIPOWER)

Adani Power (NSE:ADANIPOWER) is the group's thermal power generation arm and India's largest private thermal power producer with 18,150 MW of operational capacity across 13 plants in 8 states. FY26 revenue was approximately Rs 57,865 crore and net profit approximately Rs 12,971 crore, supported by a 23% quarter-on-quarter revenue improvement in Q4. The stock hit a record high of Rs 254.15 on May 29, 2026.

The company has a bold expansion plan to reach 42 GW by FY32 — a 2.3x increase — backed by Rs 2 lakh crore of investment. It raised Rs 7,500 crore through AA-rated NCDs in January 2026 to fund this capex.

Adani Green Energy Limited (ADANIGREEN)

Adani Green Energy (NSE:ADANIGREEN) is India's largest renewable energy company by operational capacity. As of early June 2026, it had an operational capacity of 19.3 GW (solar, wind, and hybrid), adding 5.1 GW in FY26. The company reported an exceptional EBITDA margin of 91.2% and commissioned India's first significant Battery Energy Storage System (BESS) of 3.37 GWh. Market capitalisation stood at approximately Rs 2.35 lakh crore.

The company's long-term target remains 50 GW by 2030, a target that aligns directly with India's national renewable energy ambition. Leverage is high given the capital-intensive nature of renewable projects, but the predominantly long-term PPA-backed revenue model provides cash flow predictability. Investor risk to note: high debt levels and possible equity dilution as it funds expansion.

Adani Energy Solutions Limited (ADANIENSOL)

Adani Energy Solutions (AESL) (NSE:ADANIENSOL) operates India's largest private power transmission network and is rapidly building a smart metering and distribution business. FY26 PAT surged 160% YoY to Rs 2,393 crore, while EBITDA rose 12.7% to Rs 8,726 crore. The company has a transmission project pipeline of Rs 71,779 crore under construction, and a broader tendering opportunity of approximately Rs 1.5 lakh crore.

Adani Total Gas Limited (ATGL)

ATGL (NSE:ATGL) is India's leading private City Gas Distribution (CGD) company, operating across 34 geographical areas with over 800 CNG stations. FY26 CNG volumes grew 17% YoY to 207 MMSCM and PNG volumes grew 5%. Q4 FY26 EBITDA rose 13% YoY to Rs 310 crore. Stock price around Rs 778 in June 2026. The sector faces regulatory risk from gas pricing policies and competition from electric vehicles, which could erode CNG demand over the medium term.

Ambuja Cements / ACC (AMBUJACEM / ACC)

Since the Adani Group acquired Ambuja and ACC from Holcim in 2022 for ~$6.4 billion, these have been consolidated into a One Cement Platform. Ambuja reached 109 MTPA capacity in FY26, targets 155 MTPA by FY28, and is in the process of merging ACC and Orient Cement. FY26 revenue was approximately Rs 41,490 crore with a profit of Rs 5,617 crore. Analyst consensus targets approximately Rs 620-650 for Ambuja. The cement sector offers steady volume growth but thin margins; oversupply remains a risk.

AWL Agri Business (ex-Adani Wilmar) — AWL

Following the Wilmar exit from the joint venture, the company rebranded as AWL Agri Business. FY26 revenue was approximately Rs 75,148 crore (largely a commodities-driven FMCG business in edible oils, food, and feed). PAT was approximately Rs 990 crore. The stock has declined ~28% over the past year and trades around Rs 189. Growth prospects depend on branded FMCG premiumisation, but commodity price volatility is a persistent risk.

NDTV (NDTV)

NDTV is the smallest listed entity in the Adani stable by market cap. Under Adani ownership, it has expanded into NDTV Marathi, NDTV World, and digital platforms. Revenue for Q1 FY26 was Rs 108 crore (+15% YoY), but EBITDA remained negative at approximately -Rs 57.6 crore. The stock trades around Rs 144-174. It is primarily a strategic media asset for the group; its investment appeal as a standalone financial opportunity is limited given ongoing operating losses.

Recent News and Market Triggers

- Adani Power record high (May 29, 2026): Stock hit Rs 254.15, gaining significantly from year-ago levels, driven by expansion news and FY26 earnings.

- AESL stock up 61% in 6 months: Fuelled by record smart metering installations and transmission order wins.

- APSEZ 500 MMT milestone: Cargo throughput crossed 500 MMT in FY26; May 2026 cargo up 16% YoY.

- Adani Group capex record: Rs 1.53 lakh crore capex in FY26 — the highest by any Indian corporate in a single year.

- Ambuja cement merger: Board approved amalgamation of ACC and Orient Cement with Ambuja, creating a unified cement platform.

- Adani Ports Argentina LNG contract: Secured a contract related to Argentina's first LNG export project, expanding international presence.

Growth Drivers Across the Portfolio

- India's energy transition: Renewable capacity mandate, power grid upgrades, and thermal backup needs all benefit Adani's energy cluster.

- Infrastructure build-out: Government capex on ports, airports, roads, and logistics directly supports APSEZ and AEL.

- Smart metering mandate: Government directive for 300+ million smart meters nationally creates a decade-long order runway for AESL.

- City gas expansion: PM Ujjwala, CNG fleet conversion, and new geographical area allocations benefit ATGL.

- Cement demand: Housing, infrastructure, and industrial construction support Ambuja's capacity ramp-up.

- Green hydrogen opportunity: AEL's Rs 1.97 lakh crore green hydrogen project (Khavda, Gujarat) could be transformational if commercialised at scale.

- International diversification: APSEZ's overseas port acquisitions reduce single-country revenue concentration.

- Battery storage: AGEL's 3.37 GWh BESS positions it for emerging grid-stabilisation opportunities.

Risks Investors Should Know

- Group concentration risk: Over-reliance on a single promoter group; cross-holding structures increase systemic risk across listed entities.

- High leverage at some entities: Adani Green and Adani Power carry significant project-level debt; any delay in project execution or PPA renegotiation could strain cash flows.

- Regulatory risk: Power tariff orders, gas pricing changes, port concession renewals, and environmental clearances remain key regulatory variables.

- Valuation risk: Several Adani stocks trade at significant premiums to sector peers; a correction in broader markets or negative news flow could lead to sharp de-rating.

- Merchant power risk: A portion of Adani Power's capacity operates under short-term or merchant rates, exposing it to electricity price volatility.

- Competition: In renewables (NTPC Green, Torrent, ReNew), transmission (Power Grid, Sterlite), and ports (DP World, JSW Infra), competition is intensifying.

- CNG demand substitution risk: EV adoption over the medium term could erode CNG vehicle volumes, affecting ATGL growth.

- Currency and commodity risk: Adani Enterprises (green hydrogen, airports) and AWL are exposed to global commodity and currency movements.

Valuation Considerations

Adani stocks span a wide valuation range. Adani Power trades at a P/E of approximately 33-34x (trailing twelve months as of June 2026), below the utility sector average of ~39x, suggesting potential relative value. Adani Energy Solutions trades at a P/E of approximately 55x, a premium to sector peers like Power Grid Corp (~20x), though this premium has compressed significantly from prior highs as earnings growth has caught up. Adani Green commands a very high EV/EBITDA given its renewable asset base, while APSEZ typically trades at 25-30x earnings. Adani Enterprises is valued on a sum-of-parts basis, making a simple P/E comparison less meaningful.

Ambuja Cements trades at a meaningful discount to UltraTech Cement, which may offer value given the capacity and consolidation narrative. AWL trades at roughly 25x P/E despite thin margins. Investors should verify current prices and ratios directly on NSE or BSE, as valuations shift daily.

Long-Term Outlook

Over a three-to-five year horizon, the group's energy cluster — Adani Power, Adani Green Energy, and Adani Energy Solutions — may offer the most direct exposure to India's energy infrastructure supercycle.

Adani Ports is a more defensive compounder with visible revenue and EBITDA growth tied to India's trade volumes and logistics modernisation. It offers arguably the most predictable earnings trajectory with less governance and leverage risk than some other group entities. Ambuja Cements could surprise positively if the consolidated cement platform achieves cost and volume synergies from the ACC and Orient Cement mergers.

Adani Enterprises remains a long-duration bet on green hydrogen and new airport infrastructure — high risk, high potential reward, with a longer gestation period. AWL and NDTV are smaller, niche plays with less clear growth catalysts in the near term.

Frequently Asked Questions

Q: Is Adani Ports a safer investment compared to other Adani stocks?

A: Adani Ports (APSEZ) is generally seen as having a more stable, cash-generating business model compared to capital-intensive expansion plays like AGEL or Adani Power. Its net debt-to-EBITDA of approximately 1.8x is the lowest in the portfolio. However, 'safer' is relative — all Adani stocks carry group concentration and governance risks that investors must weigh.

Q: Does any Adani Group company pay regular dividends?

A: Adani Enterprises declared a dividend of Rs 1.30 per share for FY26 (ex-date June 12, 2026). Adani Power currently does not pay dividends, with profits retained for expansion. Adani Ports has periodically paid dividends. For current dividend schedules, check the NSE/BSE corporate actions section.

Q: How does Adani Group's debt compare to industry peers?

A: At the portfolio level, Adani Group's net debt-to-EBITDA was approximately 2.5x in FY26 — a decade low. APSEZ is at 1.8x. Adani Power's leverage is expected to peak at 3.4x in FY27 before declining to ~2x by FY30. Individual entities carry varying leverage; Adani Green Energy has higher project-level debt given renewable capex. Always check the latest balance sheets on NSE/BSE.

Q: What is Adani Enterprises' green hydrogen project?

A: Adani Enterprises is developing a large-scale green hydrogen production project at Khavda, Gujarat, as part of its New Energy business. The project is intended to produce green hydrogen using renewable electricity. While the scale could be transformational, green hydrogen remains a nascent and capital-intensive sector with significant cost and demand uncertainties. Commercial monetisation timelines have not been fully confirmed.

Q: Should I buy all Adani stocks or focus on one?

A: Concentrating a portfolio in a single promoter group, regardless of the quality of underlying businesses, introduces group-level risk. A diversified approach — if you choose to invest in Adani stocks — may involve selecting one or two companies with the best risk-reward fit for your financial goals. This article is for educational purposes; it is not personalised advice. Consult a SEBI-registered investment adviser.

Conclusion

Determining the Adani stock with maximum growth potential is not a one-size-fits-all answer — it depends on an investor's time horizon, risk tolerance, and sector preference. Based on publicly available data as of June 2026, Adani Power, Adani Green Energy, and Adani Energy Solutions may have strong potential tied to India's energy infrastructure expansion, with multiple brokerages projecting 20-27% EBITDA CAGRs through FY30. Adani Ports offers a more balanced risk-reward as a logistics compounder. Adani Enterprises is the long-duration bet on new industries.

Every Adani stock carries group-level risks: high leverage at certain entities, governance concerns (though the US legal case is moving towards resolution), and valuation premiums that leave limited room for earnings disappointment. Diversification within the group and across other sectors is prudent. Verify all financial data on NSE/BSE before acting. This article does not constitute investment advice.