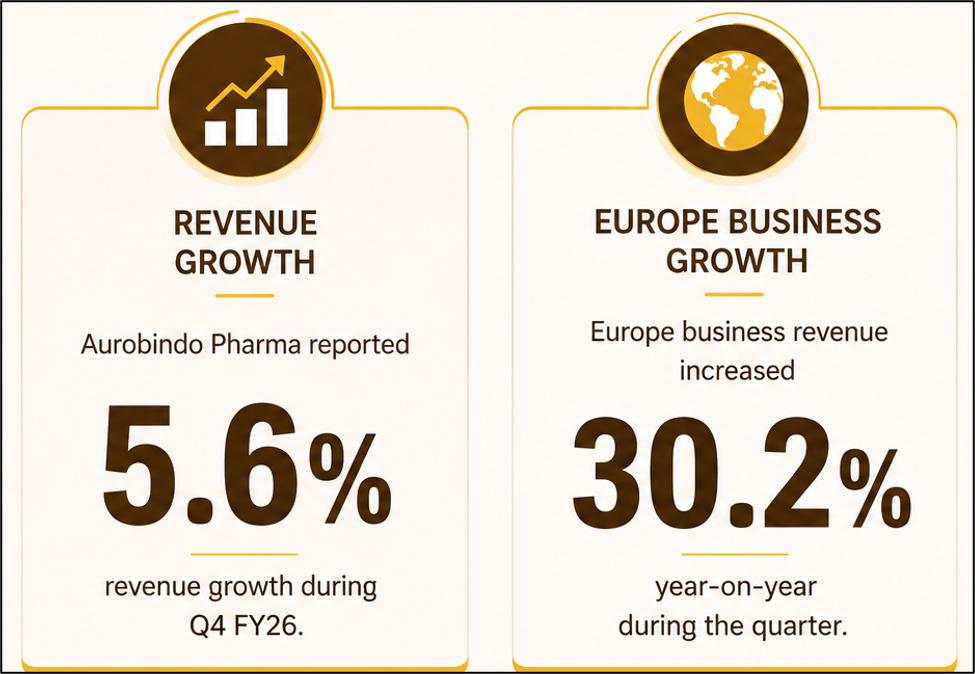

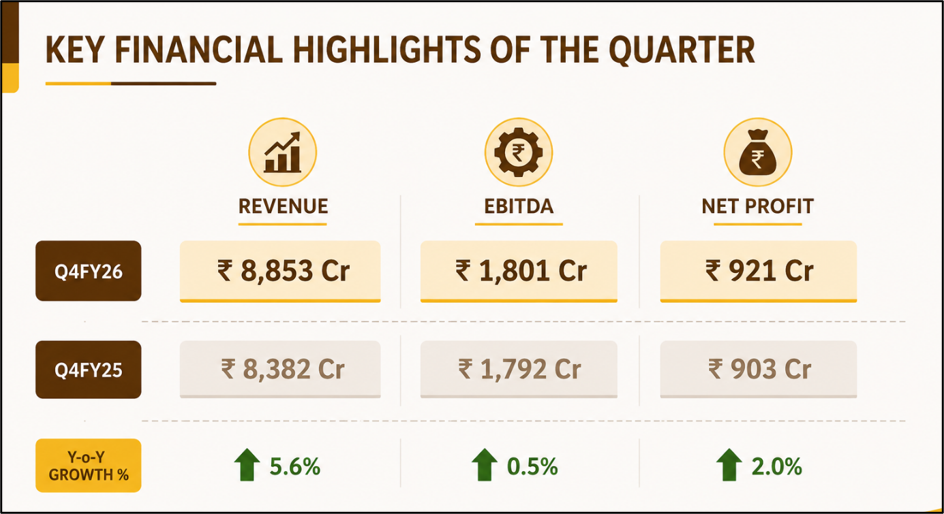

Aurobindo Pharma Limited (NSE:AUROPHARMA) reported consolidated revenue from operations of INR 8,853 crore during Q4 FY26 compared with INR 8,382 crore in Q4 FY25, reflecting year-on-year growth of 5.6 percent.

The company stated that revenue growth was driven by Europe business performance and stable US operations despite absence of transient product sales. For FY26, consolidated revenue increased 6.1 percent to INR 33,653 crore from INR 31,724 crore during FY25.

Source: Analysis by Kalkine

EBITDA and Profit Remain Stable

Quarterly EBITDA stood at INR 1,801 crore during Q4 FY26 compared with INR 1,792 crore in the corresponding quarter last year. EBITDA margin declined to 20.3 percent from 21.4 percent. Net profit for Q4 FY26 increased 2 percent to INR 921 crore compared with INR 903 crore in Q4 FY25.

For FY26, EBITDA increased 3.8 percent to INR 6,856 crore, while profit after tax rose marginally to INR 3,505 crore from INR 3,486 crore in FY25. The company reported total R&D expenditure of INR 400 crore during the quarter, accounting for 4.5 percent of sales, mainly toward biosimilars and specialty products development.

Europe and Growth Markets Support Business Performance

US formulations revenue declined 13 percent year-on-year to INR 3,543 crore during Q4 FY26. The company stated that the decline was linked to seasonality impact, while the base business remained stable. Europe business revenue rose 30.2 percent year-on-year to INR 2,795 crore, supported by performance across key markets.

Growth markets revenue increased 24.7 percent to INR 980 crore, while API revenue rose 12.9 percent to INR 1,208 crore due to volume growth in the non-antibiotics segment. The company received approval for nine products and launched 12 products in the US market during the quarter.

Biosimilars Pipeline Expands Across Markets

The company’s biosimilars business under CuraTeQ advanced approvals and regulatory filings across Europe, the UK, and Canada. Products including Zefylti, Dyrupeg, Dazublys, and Bevqolva received approvals in regulated markets. The company also highlighted planned filings for Denosumab and Omalizumab biosimilars during 2026.

Aurobindo Pharma stated that partnerships were executed with STADA for distribution of two EMA-approved biosimilars in select European territories including France and Germany. The company also initiated supplies for products in Mexico and completed four product filings in Brazil.

Biologics Manufacturing Expansion Continues

The company’s biologics contract manufacturing business, TheraNym, continued expansion during FY26. Aurobindo Pharma announced that commissioning of a 60 kL mammalian cell culture facility is expected to complete by end-2026.

The company also expanded collaboration with Merck Sharp & Dohme Singapore Trading for biologics manufacturing and supply operations. A dedicated drug substance facility under Unit 2 is expected to involve capital expenditure of approximately USD 150 million to USD 175 million.

Cash Position and Debt Profile

Net cash including investments stood at approximately USD 317 million as of March 31, 2026, after payment related to the Khandelwal Labs acquisition. Cash balance and investments increased to INR 10,676 crore as of March 2026 from INR 8,307 crore a year earlier. The company generated free cash flow of USD 35 million during Q4 FY26.

Source: Company Filing

Key Risks

- US formulations revenue pressure may affect future quarterly growth performance.

- Higher R&D spending may impact profitability and operating margins.

- Regulatory delays could affect biosimilar approvals and product launches.

- Large biologics manufacturing capex may increase execution and financial risks.

Summary

Aurobindo Pharma (NSE:AUROPHARMA) reported revenue growth during Q4 FY26 supported by Europe, growth markets, and API business performance. EBITDA and net profit remained relatively stable despite margin pressure. The company continued expanding its biosimilars pipeline, biologics manufacturing capabilities, and regulatory filings across global markets while maintaining a net cash position and positive free cash flow generation.

FAQs

Q: What drove Aurobindo Pharma’s Q4 FY26 revenue growth?

A: Europe business growth, API sales, and growth markets performance supported quarterly revenue expansion during Q4 FY26.

Q: How did the US formulations business perform during Q4 FY26?

A: US formulations revenue declined due to seasonality and lower transient product sales during the quarter.

Q: What biosimilars developments were highlighted by Aurobindo Pharma?

A: The company expanded approvals, filings, partnerships, and manufacturing capacity across Europe, Canada, and other global markets.