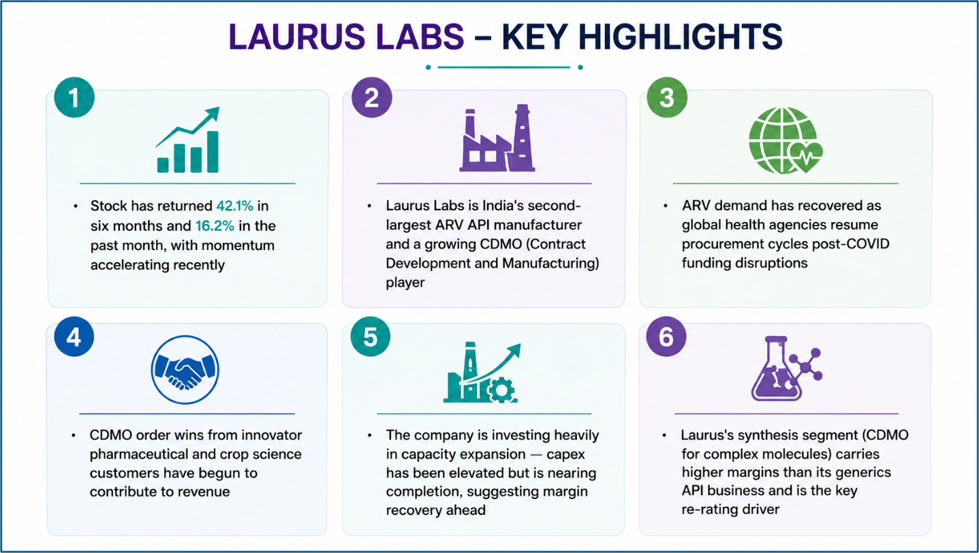

At Rs 1,426.8, Laurus Labs has staged a sharp recovery from its multi-year lows. A revival in CDMO orders, ARV (antiretroviral) demand, and new synthesis contracts are rebuilding the earnings story — but the path back to peak margins is still in progress.

9 June 2026 | Kalkine Media

CDMO: The Structural Growth Engine

The Contract Development and Manufacturing Organisation (CDMO) business — where a company manufactures complex molecules on behalf of global pharma innovators — has been one of the most sought-after sub-sectors in global pharma investing. Post-COVID, innovator pharma companies have accelerated outsourcing of manufacturing to reduce capital intensity, and CDMO players with high chemistry skills have been the beneficiaries.

India's CDMO sector has attracted particular attention because Indian companies offer a combination of high chemistry capability, experienced scientific talent, and significantly lower costs than Western counterparts. Laurus Labs, through its synthesis (CDMO) segment and its investments in biologics and fermentation, is positioning itself at the higher-value end of the CDMO spectrum rather than competing purely on commodity generics API manufacturing.

India's CDMO market is projected to grow at approximately 15-18% CAGR over the next five years, and Laurus Labs is among the handful of domestic companies with the chemistry capability to address the higher-complexity, higher-margin end of this market.

ARV Demand Recovery

Antiretroviral drugs for HIV/AIDS treatment remain one of Laurus Labs' largest revenue segments. ARV demand had faced headwinds as global health agencies — primarily PEPFAR and the Global Fund — faced funding uncertainty in the post-COVID budget environment. That uncertainty has largely resolved, and procurement volumes have recovered, restoring a segment that had been a drag on Laurus's revenue growth in FY2024-25.

The ARV segment is unlikely to be a high-growth driver going forward — it is a mature market with competitive pricing dynamics. However, its recovery removes a major headwind and allows the CDMO and formulations segments to drive the overall growth narrative.

Capacity Expansion Nearing Completion

Laurus Labs has been in the middle of a large multi-year capacity expansion programme across its API, synthesis, and biologics facilities. This capex cycle has suppressed free cash flow and margins in recent years — a period during which the market punished the stock heavily. As new facilities come onstream and utilisation ramps up, fixed cost absorption should improve significantly, driving operating leverage and margin recovery.

Sector Insights: Indian Pharma's CDMO Moment

Indian pharmaceutical companies have historically been valued primarily as generic drug manufacturers — a business model based on manufacturing off-patent drugs efficiently. The CDMO opportunity represents a structural upgrade of that model: instead of competing on price for commodity generics, companies develop long-term manufacturing partnerships with innovators, earning higher margins and more predictable revenue streams.

The China-plus-one strategy being adopted by global pharma companies — reducing supply chain dependence on Chinese API and CDMO suppliers — has created a significant incremental opportunity for Indian CDMO players. Laurus Labs, with its chemistry capabilities and expanding capacity, is well-positioned to capture a share of this diversion of business away from China.

Technical View

Laurus Labs has been in a powerful recovery phase from its multi-year low near Rs 300-350, touched during the worst of the post-COVID CDMO order drought period. The 42% six-month gain and 16% monthly gain indicate accelerating momentum. The stock is now approaching a significant resistance zone at Rs 1,500-1,600, which coincides with prior support levels from 2022-23 that are now acting as resistance.

A sustained break above Rs 1,600 on strong volume would signal the next leg higher, with technical targets at Rs 1,800-2,000. Support on pullbacks is at Rs 1,200-1,300. The 998,500 shares traded on 9 June represents healthy institutional-level liquidity. The recent acceleration in monthly returns (16.2% in one month versus 42.1% over six months) suggests momentum is building rather than fading.

The technical picture suggests the stock is entering the later stages of its initial recovery phase and approaching a breakout decision zone. The next quarterly result will be critical in determining whether the stock has the fundamental support to clear the Rs 1,600 resistance.

Bull, Base, and Bear Case

Bull Case — Rs 1,900-2,200

CDMO order wins accelerate significantly, ARV demand remains stable, and capacity utilisation ramps ahead of expectations. Synthesis segment margins recover toward 20%+ EBITDA. Multiple re-rates to 35-40x forward FY27 earnings. Target: Rs 1,900-2,200.

Base Case — Rs 1,300-1,600

Steady recovery in CDMO and ARV segments, gradual margin improvement as capex cycle ends. Market gives partial credit for the recovery story. Consolidation near current levels pending stronger evidence of CDMO revenue scale.

Bear Case — Rs 900-1,100

CDMO order wins fail to materialise at meaningful scale, ARV procurement faces fresh headwinds from global health funding cuts, and margin recovery is delayed. Valuation compresses to 20-22x forward earnings as the recovery thesis loses credibility.

What Next?

The Q1 FY27 result is the most important near-term data point. Watch for CDMO segment revenue growth, synthesis order disclosures, and commentary on ARV volume trends. Any announcement of a significant new CDMO partnership with an innovator pharma company would be a major catalyst. Laurus Labs is a multi-year recovery and rerating story — investors with a 2-3 year horizon and tolerance for quarterly earnings volatility may find the current valuation interesting.

The stock has rebounded strongly but has not yet broken out to new highs. For Laurus to become a Rs 2,000+ stock, it needs to demonstrate that the CDMO segment can scale to 30-40% of total revenues at higher margins — a plausible but not yet proven outcome.