Company Overview

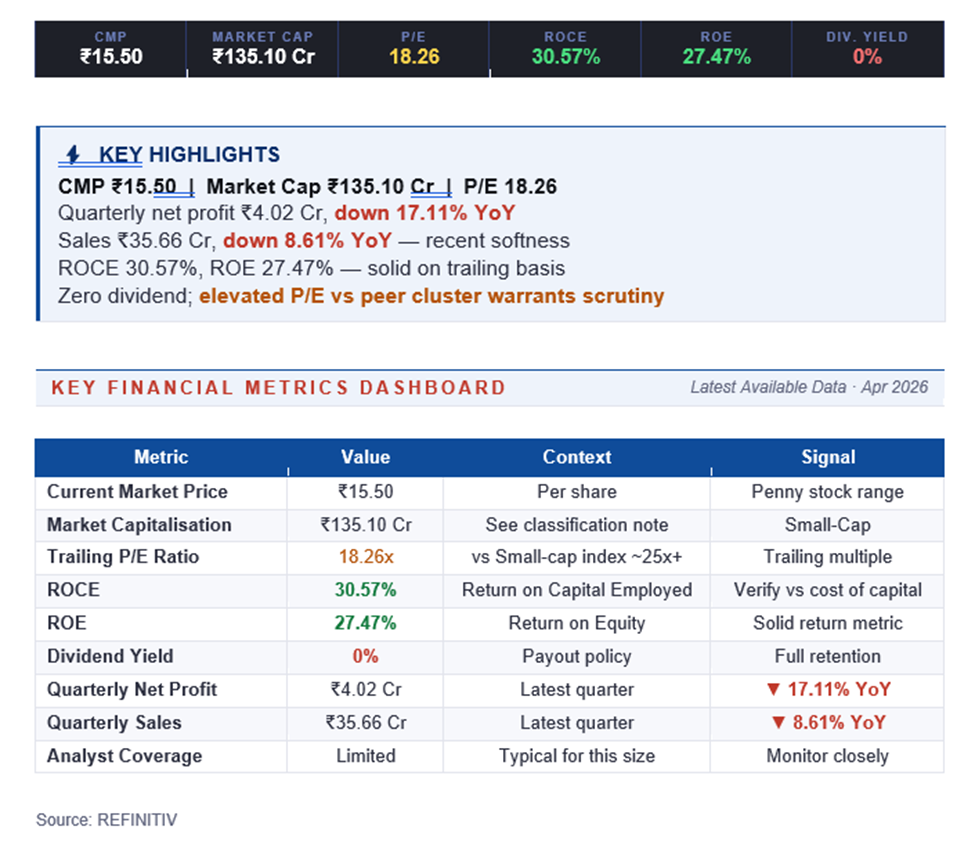

Enser is a small-cap Indian listed entity operating in the communications and technology services segment. With a market capitalisation of ₹135.10 crore and a share price of ₹15.50, Enser is larger than most nano-cap penny stocks but still firmly in small-cap territory. Indian communications and tech-services companies in this size bracket typically operate in B2B domains — providing communication infrastructure, IT services, or specialised technology solutions to enterprise and government customers.

The financial signature — trailing ROCE of 30.57% and ROE of 27.47% — suggests the business has a capital-efficient model. The P/E of 18.26 is the highest-priced trailing multiple in the mid-ROCE cluster, indicating the market has historically assigned a growth premium to Enser, though recent quarterly softness may test that premium.

Price Performance

At ₹15.50 and ₹135 crore market cap, Enser has better liquidity than nano-cap peers but remains a small-cap where price swings on earnings and sector flows can be pronounced. The stock is likely to respond to quarterly results, enterprise-contract announcements, and broader small-cap sentiment.

Investors should pay attention to whether the recent sales softness reverses in upcoming quarters — a sustained decline could compress the premium P/E multiple.

Shareholder Returns

Enser offers no dividend (0% yield). For a business with 30%+ ROCE, retaining earnings is the economically rational choice — assuming those earnings can be profitably reinvested.

With quarterly profit and sales both softening, investors should be alert to whether retained capital is translating into growth investments or idle cash. Total shareholder return depends on earnings recovery and a continued premium multiple.

Financials

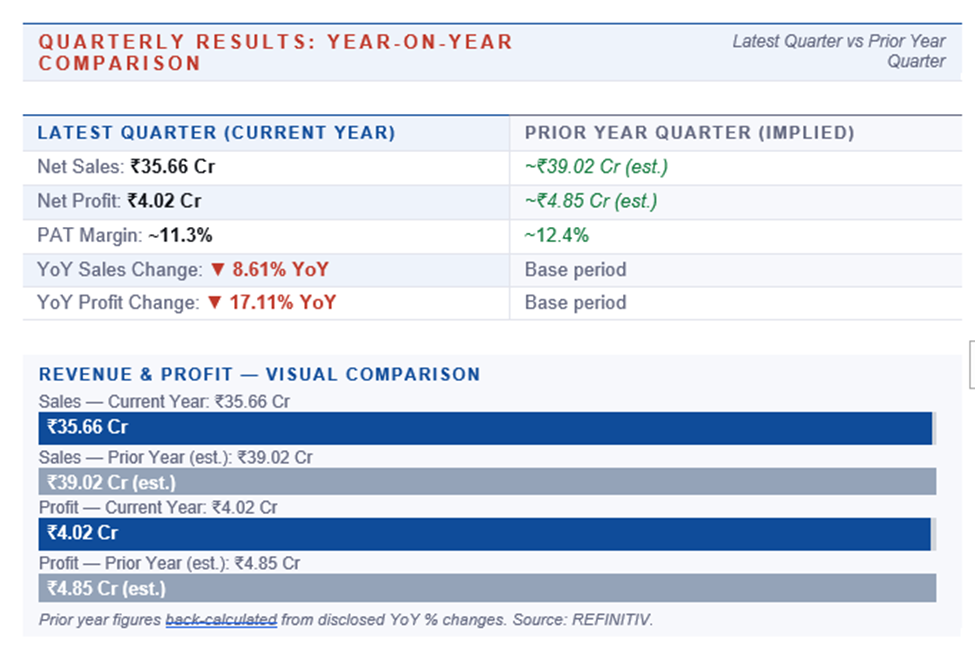

Enser's latest quarter reflects a period of operational softness. Quarterly net profit declined 17.11% YoY to ₹4.02 crore, while quarterly sales fell 8.61% to ₹35.66 crore. Despite the decline, trailing return ratios remain strong — ROCE of 30.57% and ROE of 27.47% — which suggests the structural business model is healthy even if recent quarters have slowed.

The P/E of 18.26 reflects this tension: the market is paying a premium multiple on return ratios while accepting a short-term earnings dip. If results stabilise and then recover, the current multiple is defensible. If the decline continues, P/E compression is a real risk.

Risks

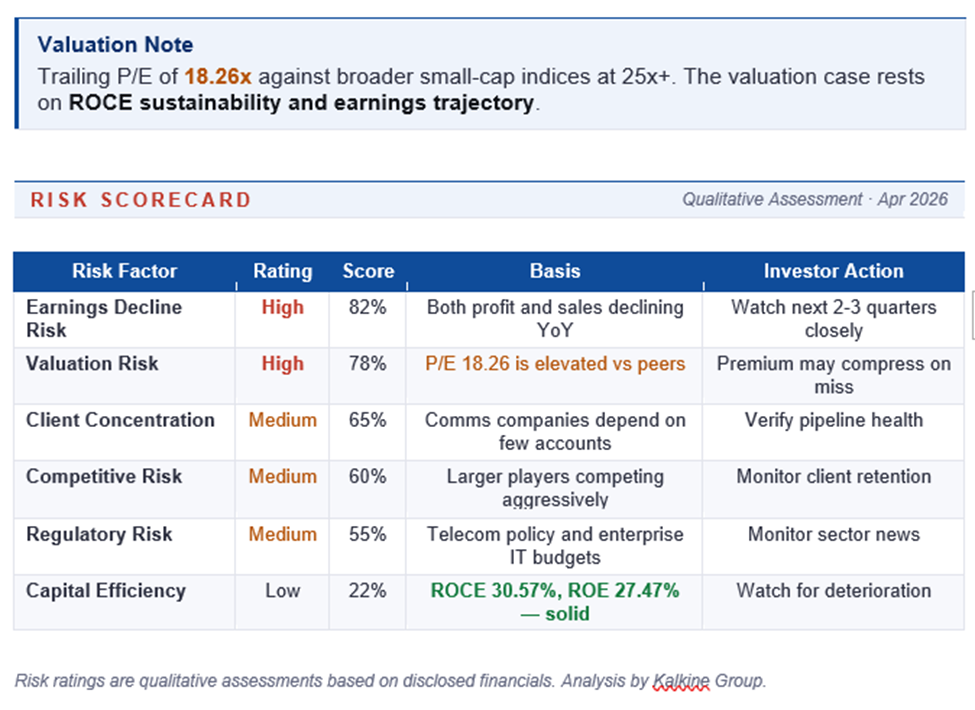

- Earnings-decline risk: The recent drop in both profit and sales, if sustained over multiple quarters, will weigh on the stock significantly.

- Valuation risk: A P/E of 18.26 is notably higher than peers in this cluster; any disappointment has disproportionate downside.

- Client-concentration risk: Communications and IT services companies at this size often depend on a small number of large accounts.

- Regulatory and sector risk: Communications-adjacent businesses can be affected by telecom policy, spectrum decisions, and enterprise-IT budget cycles.

Business Strategy

Enser's strategy is premised on maintaining a high-ROE services business with growth layered on top. The recent softness suggests either a temporary slowdown with existing clients, a competitive setback, or a transitional period as the business repositions.

Strategic credibility will come from: (1) clarity on whether the decline is demand-led or execution-led, (2) disclosure on client concentration and pipeline health, and (3) evidence of investment in new capabilities or client additions.

Valuation

At P/E 18.26, Enser trades at a meaningful premium to most names in this ROCE cluster. The current challenge is that the earnings trajectory has turned down while the multiple remains elevated. Investors must decide whether to underwrite the thesis that recent softness is transient, or wait for multiple compression before committing capital.

On market-cap-to-sales (~0.9x on annualised current-quarter revenue), the stock is not egregiously priced, but the P/E lens remains the most relevant near-term valuation anchor. The next one or two quarterly results will likely determine whether the current multiple holds.

Frequently Asked Questions

What does Enser do?

Enser operates in the communications and technology services segment. Specific business lines and customer verticals should be verified from the company's annual report.

Why did Enser's profit fall?

Quarterly profit declined 17.11% YoY on an 8.61% sales decline. Specific drivers — contract timing, client-mix shifts, or cost pressures — should be confirmed from quarterly filings.

Does Enser pay dividends?

No. The dividend yield is 0%.

What's the market cap?

Approximately ₹135.10 crore, placing Enser in the small-cap category.