Company Overview

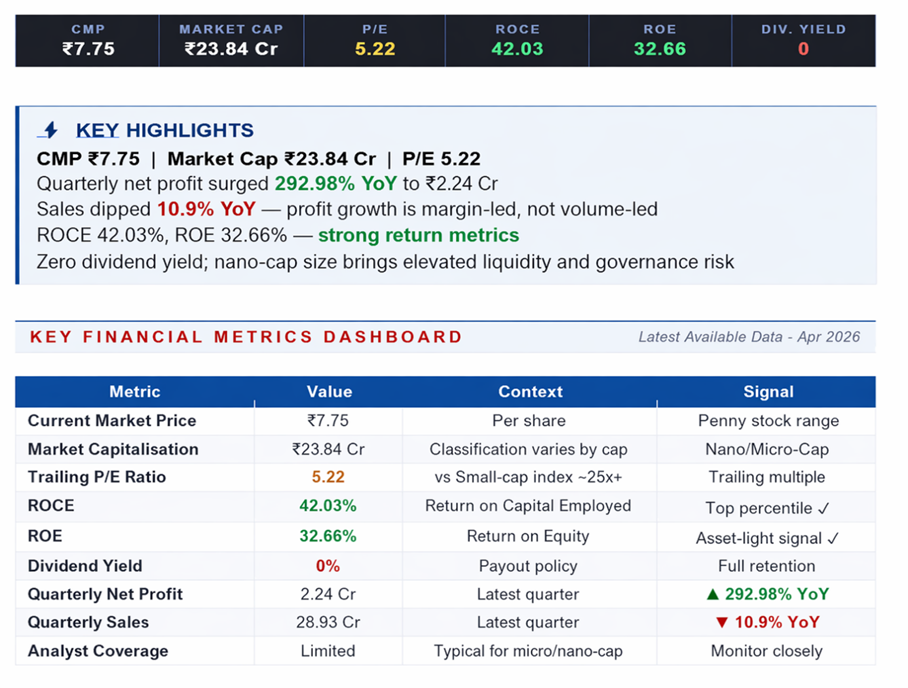

Onesource Industries (BSE:OIVL) is a nano-cap listed company with a market capitalisation of ₹23.84 crore and a share price of ₹7.75. As a business at this size, Onesource operates in a segment of the market that receives very limited coverage, leaving most investor understanding dependent on self-sourced reading of the annual report and exchange filings.

The sheet data suggests a lean, capital-efficient operation: trailing ROCE of 42.03% and ROE of 32.66% are comfortably above the cost of capital for Indian small-caps, indicating that the business model is generating healthy returns on the capital deployed. Companies of this size typically operate as niche-specialty manufacturers, regional traders, or services businesses with low fixed-asset intensity. Investors interested in the stock should make their first task a careful read of the company's business description in its latest annual report.

Price Performance

At ₹7.75 and a ₹23.84 crore market cap, Onesource is an illiquid nano-cap where daily volumes are likely thin and price discovery is episodic rather than continuous. Price moves in such stocks are often driven by small numbers of buyers and sellers, which means both appreciation and depreciation can be sharp and non-linear.

For investors considering an entry, the practical challenges are significant: limit orders may take days or weeks to fill, stop-losses may not execute at intended prices, and exit during a downturn may be constrained. These are reasons to size positions modestly and treat the investment as illiquid.

Shareholder Returns

Onesource pays no dividend (0% yield). This is consistent with the typical posture of a small, high-ROE business: retained earnings at 32% ROE, if reinvested productively, generate more shareholder value than dividends.

However, as with all nano-caps, the practical question is whether management has a credible pipeline of reinvestment opportunities. Ongoing monitoring of cash balances, capex trends, and promoter communication is essential to form a view on whether the no-dividend policy is creating value.

Financials

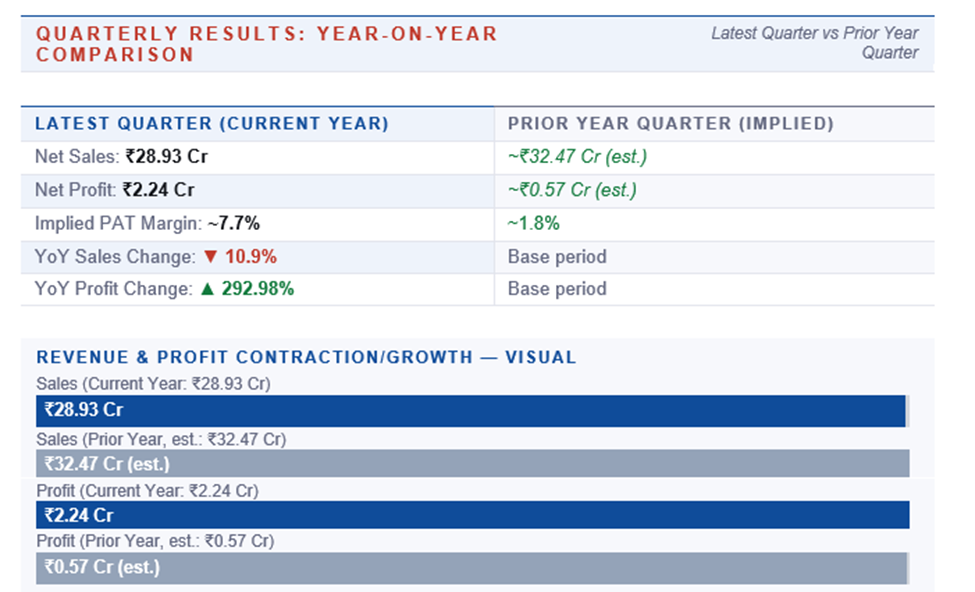

Onesource's latest quarter is striking on the profit line. Quarterly net profit rose 292.98% YoY to ₹2.24 crore, even as quarterly sales fell 10.9% to ₹28.93 crore. The combination of declining revenue and sharply rising profit is an unusual pattern that typically signals one of three things: (1) a one-off gain such as an asset sale, insurance recovery, or tax write-back; (2) meaningful cost restructuring that has dramatically lowered the expense base; or (3) a product-mix shift toward higher-margin categories.

Each of these has very different implications for sustainability. A one-off gain will not repeat; a cost restructuring may be durable; a mix shift is the most valuable if it persists. Trailing ROCE of 42.03% and ROE of 32.66% suggest the underlying business is healthy; the P/E of 5.22 is low on a trailing basis but may re-rate significantly if the profit jump proves sustainable.

Risks

- Earnings-repeatability risk: The 293% YoY profit jump needs to be understood — if it is one-off, forward earnings will revert and the P/E will look less cheap.

- Revenue-trend risk: Sales declined 10.9% YoY; without top-line growth, profit growth is difficult to sustain beyond a restructuring cycle.

- Liquidity risk: The ₹24 crore market cap means institutional buying is unlikely, keeping the stock retail-dominated and volatile.

- Governance risk: Disclosure quality, auditor tenure, and related-party dealings all warrant independent verification.

- Surveillance risk: Nano-caps are frequently subject to ASM/GSM frameworks that can restrict trading.

- Concentration risk: At small scale, the business is likely dependent on a handful of customers — loss of any one could be material.

Business Strategy

Onesource's financial signature — high ROE, moderate size, volatile revenues but rising profitability — suggests a strategy centred on selective order-taking and margin discipline rather than volume maximisation. Small, high-ROE businesses often succeed by focusing on a defensible niche and refusing to chase low-margin work.

If this characterisation is accurate, Onesource's next strategic frontier is typically capacity-light scaling: adding product SKUs, expanding geographic coverage, or moving up the value chain without commensurate fixed-asset investment. Investors should watch management commentary for evidence of disciplined capital allocation.

Valuation

The P/E of 5.22 against a market cap of ₹23.84 crore makes Onesource appear very cheap on trailing multiples. The valuation case, however, depends entirely on the interpretation of the recent quarter. If the 293% profit jump is sustainable — driven by genuine margin expansion or a durable mix shift — the stock could re-rate toward a double-digit P/E, implying meaningful upside.

If the profit jump is one-off, the trailing P/E will normalise to a higher level as earnings revert. For most investors, Onesource is best treated as a small-size, speculative position. The key monitoring items are: quarterly profit consistency over the next two to three quarters, resumption of revenue growth, and management commentary explaining the source of the margin expansion.

Frequently Asked Questions

What does Onesource Industries do?

Onesource is a nano-cap Indian listed company. Specific business details should be verified from the company's annual report given limited public coverage at this size.

Is Onesource Industries a good penny stock buy?

On trailing numbers, the stock looks cheap (P/E 5.22, ROCE 42%, ROE 32%). However, nano-cap liquidity, declining sales, and the need to confirm earnings repeatability make this a speculative rather than conservative opportunity.

Does Onesource pay dividends?

No. The dividend yield is 0%; earnings are being retained.