Company Overview

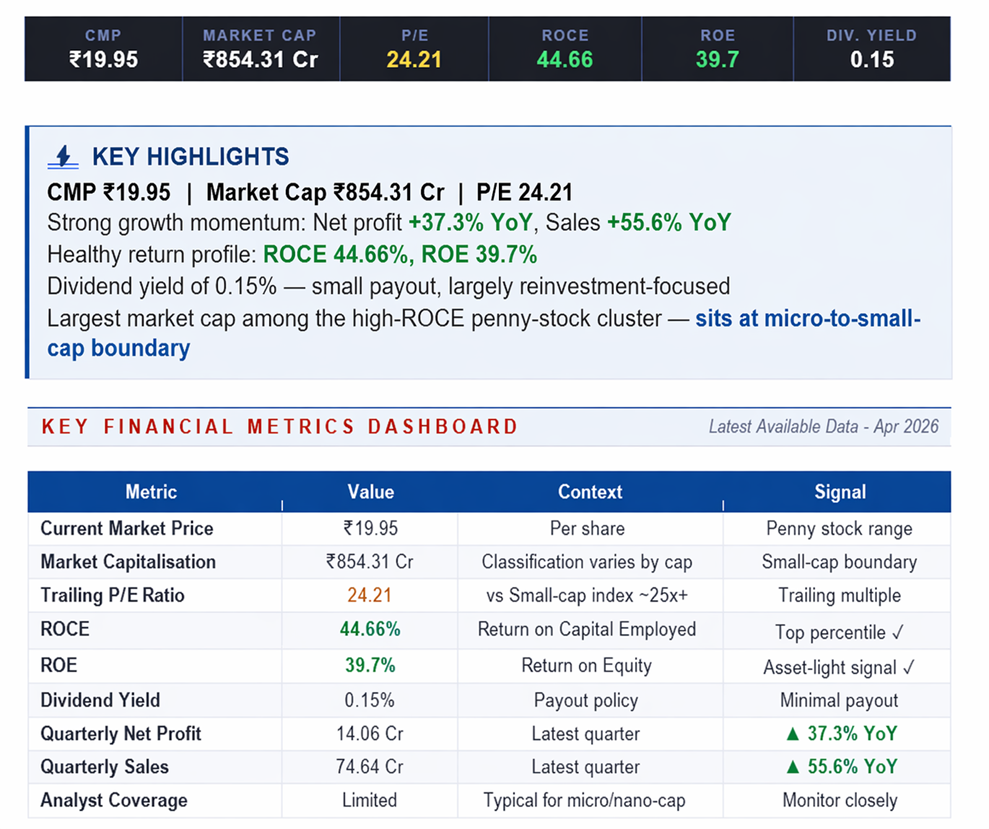

R M Drip & Sprinklers (NSE:RMDRIP) operates in India's micro-irrigation industry — a segment that has emerged as one of the most strategically important beneficiaries of agricultural modernisation and government-led water conservation initiatives. The company manufactures and supplies drip irrigation and sprinkler systems used extensively across horticulture, field crops, orchards, and protected cultivation. With a market capitalisation of ₹854.31 crore and a current share price of ₹19.95, R M Drip is the largest of the penny stocks in this cluster — sitting at the boundary between micro-cap and small-cap territory.

The business sits squarely within the India growth story: rising input costs, declining water tables, and government subsidy programmes under PMKSY (Pradhan Mantri Krishi Sinchayee Yojana) and state-level per-drop-more-crop schemes are structural tailwinds. Micro-irrigation penetration in India remains well below global benchmarks, leaving a long runway for organised players. R M Drip's return ratios and recent growth rates suggest it is capturing a meaningful share of this structural demand.

Price Performance

At ₹19.95, R M Drip trades at a price point that qualifies as a penny stock by nominal price but, given the ₹854 crore market cap, the free float and liquidity dynamics are closer to a small-cap than a typical micro-cap. This matters because the risk of exaggerated price swings on thin volumes is somewhat lower than for most names in the penny-stock screen.

Even so, the stock's volatility will remain correlated with broader small-cap sentiment, monsoon outlook, and news flow on subsidy disbursement. Investors should track delivery percentages and institutional participation over time as a proxy for improving quality of holders.

Shareholder Returns

R M Drip currently offers a dividend yield of 0.15% — a token payout that signals the company does distribute some cash to shareholders but prefers to retain the majority for reinvestment. For a business in a structurally growing industry with ROCE above 44% and ROE near 40%, a low payout ratio is economically rational: every rupee of retained earnings compounded at 40%+ is more valuable to shareholders than the same rupee distributed as dividend.

Total shareholder return for R M Drip is therefore expected to come overwhelmingly from capital appreciation driven by earnings growth and potential re-rating, not from yield.

Financials

The latest quarter shows a company firing on both cylinders. Quarterly net profit rose 37.3% YoY to ₹14.06 crore, and quarterly sales jumped 55.6% to ₹74.64 crore. The fact that revenue growth exceeds profit growth by roughly 18 percentage points suggests the company is either absorbing some input cost pressure or investing ahead of demand — a reasonable posture in a growth industry.

Return ratios are robust: ROCE of 44.66% and ROE of 39.7% indicate strong capital productivity, well above the cost of equity for Indian small-caps (typically 13–15%). This spread between ROE and cost of equity is the core driver of intrinsic value creation. The P/E of 24.21 is the highest of the penny-stock cluster, but is justified by the growth profile and return ratios.

Risks

- Monsoon dependency: Demand for drip and sprinkler systems is closely tied to rainfall patterns, sowing decisions, and farmer cash flows.

- Subsidy risk: A significant portion of micro-irrigation sales is linked to government subsidies; any policy change or delay can create receivables pressure and working capital strain.

- Competition: The industry has large, well-capitalised peers including Jain Irrigation and Netafim; R M Drip's growth will need to be defended against pricing pressure.

- Commodity risk: Polyethylene and other input costs can be volatile.

- Working capital intensity: Long receivable cycles, particularly from government channels, remain a structural feature of the industry.

Business Strategy

R M Drip's strategy appears anchored in three pillars. First, capacity and distribution expansion: to capitalise on the low penetration of micro-irrigation across India's ~160 million hectares of arable land, the company likely needs to expand manufacturing footprint and dealer networks into tier-2 and tier-3 agricultural districts.

Second, subsidy-channel leverage: aligning sales with state-level subsidy schemes and becoming an empanelled supplier in multiple states is a faster path to scale than pure retail selling. Third, capital-light compounding: with ROCE above 44%, the company can fund growth largely from internal accruals. If execution continues at the current pace, R M Drip has a credible path to compounding earnings at a double-digit CAGR over the medium term.

Valuation

At a trailing P/E of 24.21, R M Drip is not a deep-value stock — it is priced for continued growth. However, in the context of its 37% profit growth and 55% sales growth, the PEG ratio is well below 1, which many growth investors consider attractive. On a market-cap-to-sales basis, the valuation looks reasonable given the scalability of the business.

The key valuation anchor is sustainability: if ROCE remains above 35% and growth stays in the double digits, the stock can sustain or even expand its multiple. The primary downside risk is a cyclical revenue disappointment tied to monsoon or subsidy delays.

Frequently Asked Questions

What does R M Drip & Sprinklers do?

The company operates in micro-irrigation, manufacturing drip irrigation and sprinkler systems used primarily in Indian agriculture and horticulture.

Is R M Drip a penny stock?

The share price of ₹19.95 places it in the penny-stock price band, but its ₹854 crore market cap puts it closer to the small-cap category than a typical micro-cap penny stock.

How strong is R M Drip's financial performance?

The latest quarter shows net profit up 37.3% YoY to ₹14.06 Cr and sales up 55.6% to ₹74.64 Cr, with ROCE of 44.66% and ROE of 39.7%.

Does R M Drip pay dividends?

Yes, though modestly. The current dividend yield is 0.15%, suggesting the company retains most earnings for reinvestment.

What are the key risks for R M Drip investors?

Monsoon dependency, subsidy policy changes, receivables risk from government channels, competition from larger players, and raw material cost volatility.