Company Overview

Padam Cotton Yarns is a small-cap Indian listed entity in the textile industry, specifically focused on cotton yarn manufacturing or trading. With a market capitalisation of ₹27.21 crore and a share price of ₹1.24, the company is in the ultra-penny-stock category by nominal price. The Indian textile industry is cyclical, cost-competitive, and exposed to multiple factors — cotton prices, currency movements, export demand, and domestic consumption.

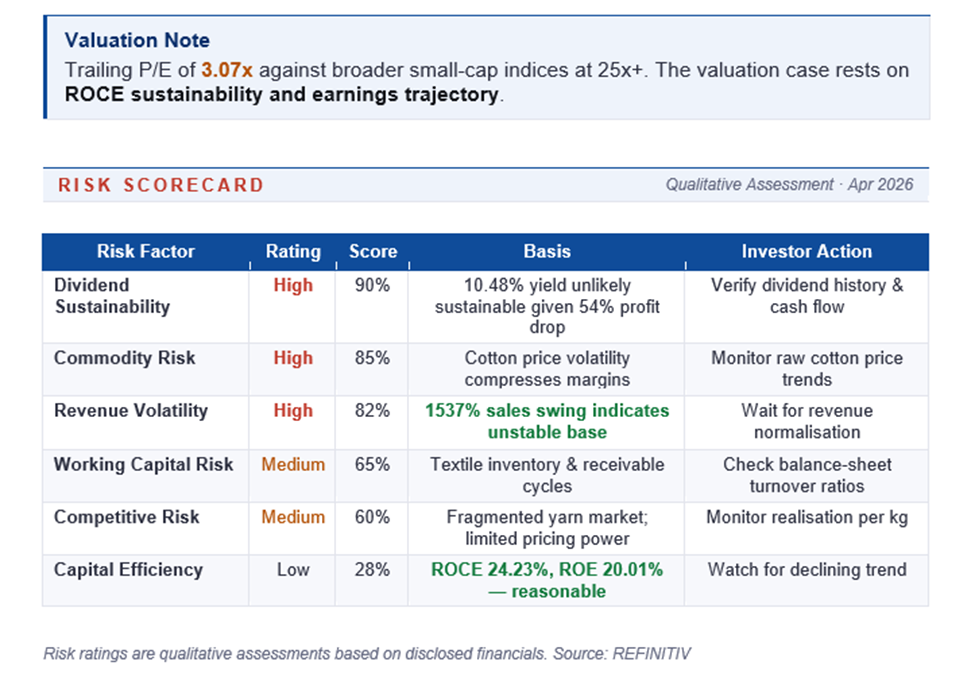

The most unusual feature of Padam Cotton's profile is the 10.48% dividend yield — remarkably high for any Indian listed company and virtually unique in the penny-stock universe. Such yields can arise from a one-off special dividend, capital return from asset sales, or a business deliberately distributing a large share of earnings. Investors must verify which of these applies before assuming the yield is sustainable.

Price Performance

At ₹1.24 per share, Padam Cotton trades at one of the lowest nominal prices in the Indian listed universe. Percentage volatility is extreme: every 5 paise is approximately 4% of the share price. The stock is almost certainly subject to circuit filters and periodic surveillance.

Price behaviour will be driven more by technical factors — retail flows, circuit limits, delivery vs intraday dynamics — than by fundamentals on a day-to-day basis. Investors should recognise this and avoid reading short-term moves as fundamental signal.

Shareholder Returns

Padam Cotton's 10.48% dividend yield is a headline feature worth careful analysis. On the face of it, this is an extraordinarily attractive yield. The critical question is sustainability: if the yield is based on a special or one-off dividend, forward yield will be dramatically lower.

Given the 54% decline in quarterly profit, a sustained high payout ratio is difficult. Investors should check the company's dividend history over the past five years and confirm whether the distribution is interim, final, or special.

Financials

The numbers tell a complicated story. Quarterly net profit of ₹2.33 crore is down 54.31% YoY — a sharp decline. However, quarterly sales of ₹18.18 crore represent an extraordinary 1537.84% YoY increase — almost certainly a low-base effect from a prior-year quarter with near-zero revenue, perhaps due to a plant shutdown or restructuring.

Taken together, these numbers suggest the business is in a transitional phase: revenue has resumed dramatically, but profit margins have compressed significantly. Trailing ROCE of 24.23% and ROE of 20.01% are reasonable but will normalise if profit continues to decline.

Risks

- Commodity risk: Cotton-yarn manufacturers are exposed to raw cotton price volatility, which can compress margins rapidly.

- Dividend-sustainability risk: A 10.48% yield is unlikely to be durable given the 54% profit decline; any dividend cut would likely trigger sharp price impact.

- Revenue-volatility risk: The extreme swing in sales (+1537%) suggests a business without a stable, predictable revenue base.

- Ultra-penny-stock risks: Liquidity, volatility, and exchange surveillance measures all apply at the ₹1.24 price level.

Business Strategy

Padam Cotton's strategy appears to be in a phase of either recovery from a prior disruption or scaling up after a restructuring. The sharp rebound in sales with compressed margins suggests the company is prioritising volume restoration, possibly accepting thinner margins to rebuild customer relationships and capacity utilisation.

For the strategy to translate into durable value creation, Padam needs to show stabilisation of revenue at the new higher base, margin recovery to historical norms as operations normalise, and a clear dividend policy supported by sustainable cash flow.

Valuation

At P/E 3.07 and a 10.48% dividend yield, Padam Cotton screens as extraordinarily cheap on both metrics. However, both ratios are heavily influenced by trailing data that may not repeat. Forward P/E will be higher if profit remains compressed; forward dividend yield will be dramatically lower if the payout is cut.

For investors, the practical question is: what is the normalised earnings power of this business? Without clarity from management on both the revenue trajectory and dividend policy, estimating fair value with confidence is difficult.

Frequently Asked Questions

Is Padam Cotton's 10.48% dividend yield sustainable?

Unlikely to be sustained at this level given the 54% quarterly profit decline. Investors should verify whether the dividend reflects a one-off special distribution or a regular policy before relying on the yield.

What does Padam Cotton do?

The company operates in the textile industry, specifically in cotton yarn manufacturing or trading.

What's the market cap?

Approximately ₹27.21 crore — small-cap / ultra-penny-stock category.