Company Overview

Computer Age Management Services Ltd (CAMS) is India's largest registrar and transfer agent (RTA) for mutual funds, managing approximately 70% of the country's mutual fund asset servicing by AUM handled. The company provides critical back-office infrastructure for mutual fund houses including investor registration, transaction processing, account servicing, KYC management, and regulatory reporting — functions that are essential but non-core for fund managers, creating a natural outsourcing relationship.

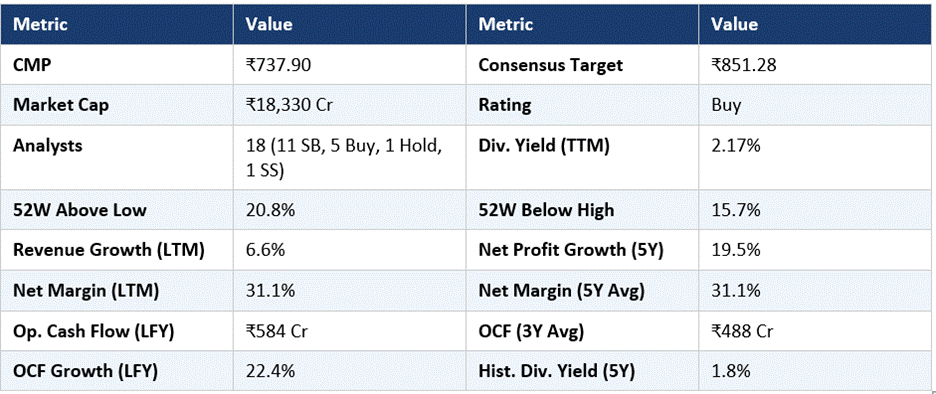

CAMS serves 16 of India's 24 registered mutual fund houses as its AMC (asset management company) clients, handling over 9 crore investor folios and processing millions of transactions daily. The company's business model is inherently linked to the growth of India's mutual fund industry — as investor folios and assets under management (AUM) grow, the transactional volumes processed by CAMS increase proportionally, driving revenue without requiring capital reinvestment in the traditional sense.

Beyond mutual fund RTA services, CAMS has been diversifying into adjacent financial infrastructure segments including insurance repository services (CAMSRep), alternative investment fund (AIF) servicing, and KYC compliance services for the broader financial sector. This diversification reduces single-industry dependency and opens additional growth vectors as India's overall financial services ecosystem deepens. The 18-analyst coverage panel — the largest in this peer group — reflects CAMS's institutional importance and earnings predictability.

Fundamental Insights

CAMS's financial metrics reflect a high-quality, capital-light financial services platform. Revenue grew 6.6% year-on-year in the latest period — modest compared to some peers in this analysis, but important context is that CAMS's revenue is tied to mutual fund transaction volumes and AUM, which have grown steadily rather than explosively. Net profit margin of 31.1% — identical to the five-year average — demonstrates the exceptional stability and consistency of the business model's economics.

The five-year net profit CAGR of 19.5% is a reliable compounding track record, confirming CAMS as a steady-growth, high-quality earnings generator. Operating cash flow of ₹584 crore in the latest year, growing 22.4% year-on-year, with a three-year average of ₹488 crore, confirms robust and growing cash generation. The 1.6% current dividend yield and 1.8% five-year average indicate a consistent dividend policy that grows broadly in line with earnings.

What makes CAMS particularly notable fundamentally is the permanence of its competitive position — as India's dominant RTA with deep integration into fund house systems and millions of investor folios, switching costs are extremely high. This gives CAMS pricing power and revenue visibility that are difficult to replicate in most businesses.

Broker Views and Analyst Consensus

CAMS has the most constructive analyst consensus in this peer group. Of 18 covering analysts, 11 carry Strong Buy ratings — an unusually high number — alongside 5 Buy, 1 Hold, and 1 Strong Sell. The consensus target of ₹851.28 implies 15.4% upside from the current ₹737.90. The dominant Strong Buy skew signals exceptional conviction in the business quality and growth trajectory.

The bull case is straightforward and compelling: India's mutual fund industry is in a sustained structural growth phase, with monthly SIP (Systematic Investment Plan) inflows regularly exceeding ₹20,000 crore, total AUM approaching ₹70 lakh crore, and investor folios growing by tens of millions annually. As the dominant RTA, CAMS is a high-margin toll road on this growth, and the organic volume leverage means earnings growth can significantly outpace headline revenue growth.

The single Strong Sell reflects a minority view that CAMS's growth rate is insufficient to justify its premium valuation and that regulatory risk from potential SEBI-mandated fee compression or mandatory RTA diversification could pressure margins. The 1 Hold rating is similarly cautious on near-term valuation grounds.

Technical Analysis

CAMS at ₹737.90 is 20.8% above its 52-week low — a solid recovery that reflects sustained institutional buying — and 15.7% below its 52-week high, indicating the stock is near the upper portion of its annual range. This positioning is consistent with a quality compounder that has maintained its upward trajectory without the speculative excess seen in some high-momentum names.

The analyst consensus target of ₹851.28 provides a clear fundamental reference, with 7.6% implied upside from current levels. Near-term support is expected around ₹750-₹760 (recent consolidation), with stronger support at the 52-week low zone around ₹611.40. Resistance at the 52-week high and then the consensus target are the sequential upside markers.

RSI is likely in a moderately elevated zone given the proximity to the 52-week high, but quality businesses with genuine earnings growth can sustain this for extended periods. The 22.4% OCF growth provides a fundamental anchor for the stock's premium valuation.

Key Metrics to Monitor

CAMS is a premier Indian financial infrastructure holding with exceptional fundamental quality — dominant market position, stable 31% net margins, consistent double-digit cash flow growth, and the structural tailwind of India's mutual fund industry growth. Investors monitoring CAMS should track monthly AMFI data on SIP inflows, total AUM, and new folio additions, as these are the direct volume drivers of CAMS's revenue and the key metrics for assessing whether the business is growing in line with or ahead of analyst expectations. The 11 Strong Buy ratings from 18 analysts make this one of the highest-conviction names in this analysis.

Frequently Asked Questions

Q1: What does CAMS do?

A: CAMS is India's largest registrar and transfer agent for mutual funds, managing approximately 70% of the country's mutual fund AUM servicing. It handles investor registration, transaction processing, account servicing, KYC management, and regulatory reporting for 16 major AMCs.

Q2: Why does CAMS have 11 Strong Buy ratings?

A: The 11 Strong Buy ratings reflect exceptional conviction in CAMS's structural growth tied to India's mutual fund industry expansion, its dominant and near-unassailable market position with 70% RTA market share, and the high-margin capital-light business model that generates consistent earnings and cash flow growth.

Q3: How is CAMS linked to India's mutual fund growth?

A: CAMS processes mutual fund transactions on behalf of AMC clients. As investor folios and AUM grow, transaction volumes increase proportionally, driving CAMS's revenue without requiring significant additional capital investment. India's mutual fund industry has been growing at ~25% annually, creating structural tailwinds.

Q4: What is the regulatory risk for CAMS?

A: SEBI could potentially mandate fee compression for RTA services, require AMCs to diversify their RTA relationships, or alter the mutual fund industry structure in ways that affect CAMS's pricing or market share. These are low-probability but high-impact risks that the minority bear thesis focuses on.

Q5: What is CAMS's dividend history?

A: CAMS has consistently paid dividends with a five-year average yield of 1.8% and current yield of 1.6%, reflecting a policy of distributing a meaningful portion of earnings while retaining capital for growth and technology investment.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Investors should conduct independent due diligence and consult a SEBI-registered investment adviser before making any financial decisions.