Company Overview

Engineers India Ltd (EIL) is a Government of India enterprise providing engineering consultancy and turnkey project services for the hydrocarbon, fertiliser, petrochemical, and infrastructure sectors. Established in 1965 and headquartered in New Delhi, EIL has been a cornerstone of India's public sector engineering capability for six decades, executing hundreds of refinery, pipeline, fertiliser, and industrial projects for Indian and international clients.

EIL's service offerings span the full project lifecycle — from front-end engineering and design (FEED), through detailed engineering, procurement assistance, and construction management, to project commissioning and startup. The company operates in two business segments: consultancy and engineering services (C&E), which provides high-margin intellectual services, and turnkey projects, which executes complete projects on behalf of clients including major PSU oil companies.

The company has emerged as a significant beneficiary of India's energy sector investment cycle, with major Indian refineries undertaking capacity expansion, secondary processing upgrades, and petrochemical integration projects. EIL is also well-positioned for the energy transition — it has been building expertise in green hydrogen, renewable energy infrastructure, and carbon capture projects, aligning its capabilities with India's stated net-zero commitments. The Government of India's holding through the Ministry of Petroleum and Natural Gas provides EIL with privileged access to PSU energy sector mandates.

Fundamental Insights

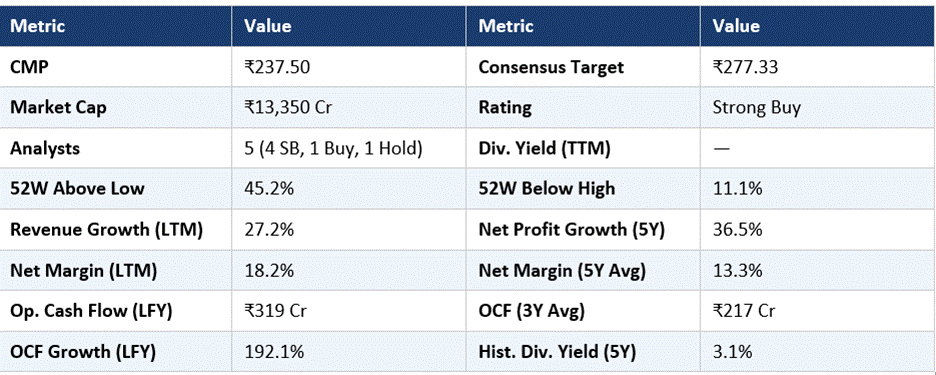

Engineers India's financial metrics show a business in a meaningful earnings upgrade cycle. Revenue grew 27.2% year-on-year — a strong acceleration reflecting the surge in Indian energy sector project activity and EIL's successful order book buildup. Net profit margin of 18.2% compares favourably to the five-year average of 13.3%, confirming genuine margin expansion driven by a higher mix of consultancy services (higher margin) versus turnkey execution.

The five-year net profit CAGR of 36.5% is exceptional and reflects both the recovery from a trough in engineering project activity and the accelerating energy infrastructure spend cycle. Operating cash flow grew 192.1% year-on-year to ₹319 crore — a dramatic improvement from the three-year average of ₹217 crore — confirming that earnings quality is high and cash conversion is improving.

The 2.2% current dividend yield and five-year average of 3.1% reflect EIL's policy as a government enterprise of distributing meaningful income to shareholders, including the government itself. The historical average yield being above current yield suggests the dividend per share has grown, with the stock price appreciation outpacing the dividend increase over the period.

Broker Views and Analyst Consensus

Five analysts cover Engineers India with a heavily bullish consensus — 4 Strong Buy and 1 Buy, with 1 additional Hold. The weighted average is a clear Strong Buy, and the consensus target of ₹277.33 implies 16.8% upside from the current ₹237.50 — one of the more compelling upside targets in this peer group.

Broker research emphasises several key value drivers: EIL's structural exposure to India's energy sector capex upcycle, including refinery upgrades, petrochemical integration, and the emerging green hydrogen opportunity; the margin expansion story as consultancy revenues (which carry 30-40% EBITDA margins) grow as a proportion of the business mix; and the company's status as a government-backed entity with protected access to PSU mandates.

Analysts also highlight the potential for EIL's international business to generate incremental revenue as Middle Eastern and African energy companies expand their refinery and petrochemical capacity. EIL has a track record of executing overseas projects and has the technical capability to compete for international mandates that many Indian engineering firms cannot.

Technical Analysis

Engineers India has appreciated 45.2% above its 52-week low and sits 11.1% below its 52-week high — a moderate recovery position suggesting the stock has meaningful room to recover toward its recent peak before approaching technical resistance. The price of ₹237.50 versus a consensus target of ₹277.33 creates a clear 16.8% fundamental upside reference.

The 192.1% operating cash flow growth is one of the most impressive metrics in this analysis and is likely to attract increasing institutional interest as earnings visibility improves through a growing order backlog. Near-term support sits around ₹220-₹225 (recent consolidation zone) and resistance at ₹255 (prior highs). A sustained move above ₹260 would open the path toward the analyst consensus target of ₹277.

RSI appears moderate given the 11.1% gap from the 52-week high, leaving technical room for appreciation. The PSU status provides a degree of stability to the price in periods of broader market weakness.

Key Metrics to Monitor

Engineers India is a high-conviction industrial pick anchored by India's energy sector investment cycle and the company's government-backed market positioning. The 4 Strong Buy plus 1 Buy consensus from 5 analysts, combined with 16.8% upside to target and the extraordinary 192.1% OCF growth, creates a compelling multi-factor case. Investors following EIL should monitor the company's quarterly order intake figures — the order backlog is the leading indicator of future revenue visibility and the primary catalyst for analyst estimate upgrades. News around green hydrogen project mandates represents a potential additional re-rating catalyst as this segment evolves from concept to commercial execution.

Frequently Asked Questions

Q1: What does Engineers India Ltd do?

A: EIL is a government-owned engineering consultancy providing project services across the full lifecycle for hydrocarbon, petrochemical, fertiliser, and infrastructure sectors. Services range from front-end design and engineering through procurement management to project commissioning.

Q2: Why does EIL have a Strong Buy consensus?

A: Four of five analysts rate EIL as Strong Buy, driven by India's energy sector capex upcycle, EIL's government-backed access to PSU mandates, significant margin expansion from rising consultancy revenue mix, and 16.8% upside to the consensus target price of ₹277.33.

Q3: What is Engineers India's exposure to green energy?

A: EIL has been developing capabilities in green hydrogen engineering, renewable energy infrastructure, and carbon capture technology — aligning with India's energy transition goals. This creates a potential long-term growth avenue beyond its traditional hydrocarbon project base.

Q4: What is the dividend track record for ENGINERSIN?

A: EIL has a five-year average dividend yield of 3.1%, higher than the current 2.2%, reflecting a consistent distribution policy as a government enterprise. The yield difference indicates the stock price has appreciated faster than dividend growth over the period.

Q5: What are the key risks for Engineers India?

A: Primary risks include slowdown in government PSU capex allocation for energy projects, execution risk on large turnkey contracts, and the longer-term challenge of redeploying skills from traditional hydrocarbon engineering to renewable energy as India's energy mix shifts.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Investors should conduct independent due diligence and consult a SEBI-registered investment adviser before making any financial decisions.