Company Overview

Gujarat Pipavav Port Ltd (GPPL) operates the Pipavav Port on the Gujarat coastline, one of India's first private sector ports and the country's first container terminal to be developed as a public-private partnership. Located approximately 150 kilometres from Rajkot in the Saurashtra region of Gujarat, Pipavav serves as a gateway port for trade flows to and from India's northwestern hinterland, which encompasses parts of Gujarat, Rajasthan, Punjab, and Haryana.

The port handles container traffic, bulk cargo, liquid cargo, and roll-on-roll-off (RoRo) cargo. Its deepwater berths can accommodate large post-Panamax container vessels, giving it a capacity advantage over shallower ports. GPPL is a subsidiary of the A.P. Moller-Maersk group, with the Danish shipping conglomerate's involvement providing global customer relationships, operational expertise, and management credibility that smaller Indian port operators cannot match.

GPPL's geographic location on India's western coast positions it well for trade with the Middle East, East Africa, and Europe — trade corridors that are benefiting from India's growing merchandise export agenda and the restructuring of global supply chains. The port's direct rail connectivity to major hinterland centres reduces road freight dependency and makes it competitive for time-sensitive containerised cargo.

Fundamental Insights

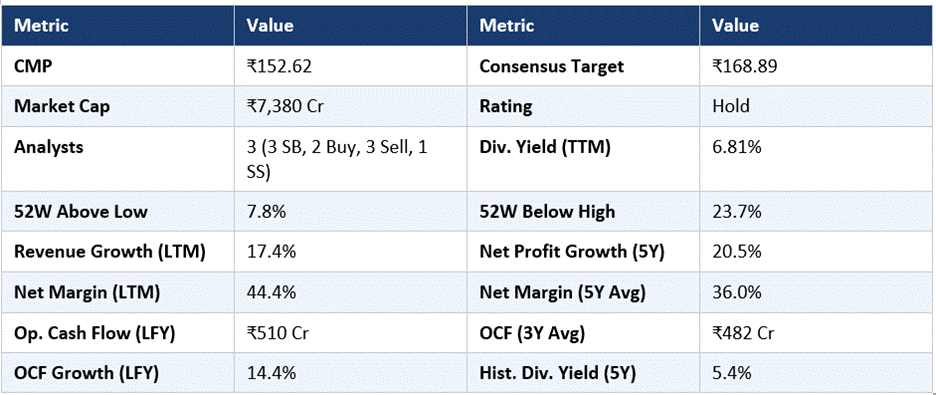

GPPL delivers financial metrics characteristic of a high-quality, asset-heavy port infrastructure business. Revenue grew 17.4% year-on-year in the latest reporting period, driven by higher container volumes and improved cargo mix. Net profit margin of 44.4% is exceptional for a port operator and reflects the high operating leverage of infrastructure assets once fixed costs are covered by baseline cargo volumes. The five-year average margin of 36.0% confirms that the current margin improvement is building on an already-strong base.

Five-year average net profit growth of 20.5% is solid and consistent, confirming that GPPL has been a reliable earnings compounder over the medium term despite the cyclical nature of shipping volumes. Operating cash flow of ₹510 crore in the latest year represents 14.4% growth, and the three-year average of ₹482 crore demonstrates consistent cash generation that underpins the generous dividend policy.

The current dividend yield of 6.6% is the highest in this peer group and is supported by strong and growing operating cash flows. The five-year average dividend yield of 5.4% confirms a sustained and growing income stream. For income-focused investors, GPPL's ability to combine meaningful capital appreciation potential with a 6.6% yield makes it a distinctive proposition within Indian industrials.

Broker Views and Analyst Consensus

The analyst community is notably divided on GPPL — among the 9 analysts covering the stock, the data shows 3 Strong Buy, 2 Buy, 0 Hold, 3 Sell, and 1 Strong Sell. This produces an overall mean rating that is broadly neutral (Hold), with a consensus target of ₹168.89 implying 10.7% upside from the current ₹152.62. The wide dispersion of views makes GPPL one of the more analytically contested stocks in this peer group.

The bull case from the Strong Buy and Buy analysts focuses on the port's deepwater infrastructure advantage, Maersk's management backing, India's structural trade growth story, the generous dividend yield, and the stock's relatively low valuation relative to its infrastructure peers. Bulls argue that GPPL's geographic positioning for Middle East and European trade routes is underappreciated.

The Sell-side bears focus on competition from new private and government port projects along the western coastline, the risk of volume diversion to JNPT and Mundra Port as shippers consolidate routes, limited growth in the port's throughput capacity without significant capital expenditure, and the stock's premium valuation relative to its volume growth trajectory.

Technical Analysis

GPPL is in a technically subdued position — only 7.8% above its 52-week low and 23.7% below its 52-week high, indicating the stock is well off its peak and has not participated in the broader market recovery to the same degree as its peers in this analysis. This underperformance relative to 52-week high levels is consistent with the divided analyst community and lack of a clear near-term catalyst narrative.

The price of ₹152.62 against a consensus target of ₹168.89 suggests the stock is broadly fairly valued on average broker estimates. Support is expected around ₹145-₹150 (recent lows zone) and resistance at ₹175-₹180 (prior consolidation highs). The 6.6% dividend yield provides an income cushion that moderates total return downside risk for holders.

Key Metrics to Monitor

GPPL presents an unusual combination of high income and contested growth prospects. The 6.6% dividend yield, strong operating cash flow, and Maersk association make it a defensible infrastructure holding. However, the near-equal split between bullish and bearish analysts signals genuine fundamental uncertainty about the port's volume trajectory and competitive dynamics. Investors evaluating GPPL should pay close attention to quarterly container volume throughput data and tariff revision news, as these are the primary drivers of revenue and the key variables where bull and bear scenarios diverge. The income characteristics are the strongest near-term investment argument.

Frequently Asked Questions

Q1: What is Gujarat Pipavav Port and who owns it?

A: GPPL operates the Pipavav deep-sea port on Gujarat's western coastline, handling container, bulk, liquid, and RoRo cargo. It is majority-owned by the A.P. Moller-Maersk group — the world's largest container shipping company — which provides global commercial relationships and operational expertise.

Q2: Why does GPPL pay such a high dividend?

A: GPPL's 6.6% dividend yield is supported by strong and consistent operating cash flows (₹482 crore three-year average) and a mature infrastructure asset base that requires limited maintenance capex relative to its cash generation. The five-year average yield of 5.4% confirms a sustained dividend history.

Q3: Why are analyst views on GPPL so divided?

A: The divergence between Strong Buy and Sell-rated analysts reflects differing views on GPPL's long-term volume growth trajectory, competition from expanding Indian port infrastructure, and the stock's valuation relative to growth prospects. The Maersk association is a positive for bulls but does not resolve competitive concerns for bears.

Q4: What cargo does Pipavav Port handle?

A: GPPL handles containerised cargo, bulk commodities, liquid cargo, and RoRo (vehicle) cargo. The container segment is the primary revenue driver, and the port's deepwater berths accommodate large post-Panamax vessels that cannot call at shallower Indian ports.

Q5: What is the main risk for GPPL investors?

A: The primary risk is volume competition from expanding port capacity at Mundra (Adani Ports), JNPT, and new government port projects along the western coastline. GPPL's relatively limited ability to expand throughput without major capex constrains its volume growth ceiling.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Investors should conduct independent due diligence and consult a SEBI-registered investment adviser before making any financial decisions.