Company Overview

Zensar Technologies Ltd is an Indian mid-tier IT services and solutions company, part of the RPG Group, providing digital transformation, application development, infrastructure management, and analytics services to clients globally. Headquartered in Pune, Zensar serves clients across the United States, Europe, the United Kingdom, and South Africa across industries including manufacturing, retail, consumer, and hi-tech.

The company has undergone significant strategic repositioning over the past several years under new leadership, focusing on digital and cloud transformation services for its client base while pruning lower-margin legacy infrastructure work. This strategic pivot — accelerating the shift toward higher-value advisory, digital, and cloud services — has been the key narrative driving analyst optimism about margin expansion and growth reacceleration.

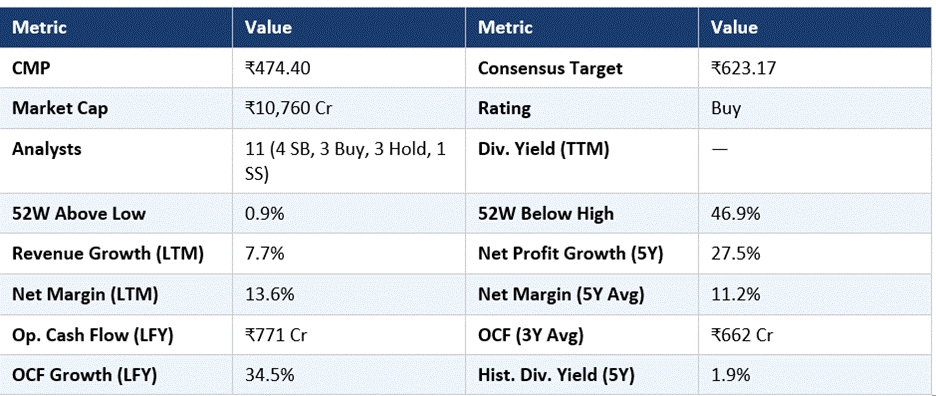

Zensar competes in the mid-tier IT services space, where it faces competition from peers including Mphasis, Persistent Systems, Coforge, and larger players. The RPG Group parentage provides financial stability and brand credibility in client acquisition. With 11 analysts covering the stock and a Buy consensus, Zensar attracts active institutional research interest as a potential turnaround and re-rating story within the Indian IT sector.

Fundamental Insights

Zensar's financial metrics reflect a company in a gradual improvement trajectory rather than explosive growth. Revenue grew 7.7% year-on-year — modest by Indian IT sector standards, reflecting the client-specific headwinds the company has navigated while restructuring toward higher-value services. Net profit margin of 13.6% is above the five-year average of 11.2%, confirming that the strategic pivot toward digital services is delivering margin improvement even as revenue growth has been subdued.

The five-year net profit CAGR of 27.5% is strong and reflects both margin expansion and earnings recovery from a trough period. Operating cash flow of ₹771 crore in the latest year — growing 34.5% year-on-year — is a notably strong cash generation metric, and the three-year average of ₹662 crore confirms consistent cash conversion quality. The 3.0% dividend yield is the second-highest in this peer group and is well-supported by the strong OCF generation.

The most striking technical observation in Zensar's data is the positioning — only 0.9% above the 52-week low and 44.7% below the 52-week high. This is a stock that has underperformed significantly from its recent peak, creating the valuation opportunity that is driving the Strong Buy and Buy thesis from the more bullish analysts.

Broker Views and Analyst Consensus

Eleven analysts cover Zensar with 4 Strong Buy, 3 Buy, 3 Hold, and 1 Strong Sell — a broadly positive but moderately contested consensus. The mean target of ₹623.17 implies 31.4% upside from the current ₹474.40, one of the wider analyst-to-price gaps in this peer group and reflecting the underperformance from the 52-week high.

The bull case from Strong Buy and Buy analysts centres on the valuation opportunity created by the sharp pullback from highs, the ongoing margin improvement story, Zensar's cash generation quality, and the expectation that revenue growth will reaccelerate as the IT services sector recovers from the demand softness seen in recent quarters. The 3.0% dividend yield provides a floor return while investors wait for the growth recovery.

The 3 Hold ratings reflect scepticism that revenue growth will reaccelerate materially in the near term, given client spending caution in key markets including the United States and Europe. The 1 Strong Sell rating represents concern that Zensar's competitive positioning within mid-tier IT is structurally disadvantaged relative to peers with stronger domain specialisation or larger scale.

Technical Analysis

Zensar's technical picture is the most distinctive in this peer group — the stock sits just 0.9% above its 52-week low and 46.9% below its 52-week high. This means the stock has lost nearly half its value from its peak, creating the value setup that bulls are exploiting. From a technical recovery standpoint, the magnitude of the decline means any positive fundamental catalyst could drive a sharp recovery, as short positions unwind and value buyers enter.

Near-term resistance sits at ₹550-₹560 (prior consolidation zone), and a break above that level would signal the beginning of a meaningful recovery toward the ₹600 zone. Support at the 52-week low zone around ₹470 is the critical near-term floor — a breach would signal further technical deterioration. RSI is likely near oversold levels given the depth of the pullback, creating a potential technical setup for a mean reversion bounce.

Key Metrics to Monitor

Zensar represents the most contrarian setup in this peer group — a stock trading at its 52-week low while the majority of analysts carry Buy or Strong Buy ratings with 26% upside to consensus target. The 3.0% dividend yield cushions the downside while the market waits for growth signals. Investors evaluating Zensar should closely monitor quarterly revenue growth (particularly in constant currency terms), client mining metrics, and deal win announcements — these will be the primary indicators of whether the revenue reacceleration thesis is materialising. The IT sector demand environment in the US and Europe is the key macro variable.

Frequently Asked Questions

Q1: What does Zensar Technologies do?

A: Zensar is an Indian mid-tier IT services company providing digital transformation, application development, infrastructure management, and analytics services to US, European, and South African clients across manufacturing, retail, consumer, and hi-tech industries.

Q2: Why is ZENSARTECH stock near its 52-week low?

A: Zensar has experienced a sharp pullback from its 52-week high, driven by subdued revenue growth amid IT services demand softness in key markets. The 46.9% decline from the 52-week high has created the valuation opportunity that underpins the Buy and Strong Buy ratings from most analysts.

Q3: What is the analyst view on Zensar?

A: 11 analysts cover ZENSARTECH with 4 Strong Buy, 3 Buy, 3 Hold, and 1 Strong Sell. The consensus target of ₹623.17 implies 31.4% upside from the current price — the widest analyst-to-price gap in this peer group.

Q4: Does Zensar pay good dividends?

A: Yes, Zensar's 3.0% current dividend yield is one of the highest among Indian IT mid-caps and is supported by strong operating cash flow of ₹771 crore in the latest year. The five-year average yield of 1.9% shows the absolute dividend has been growing over time.

Q5: What would be the catalyst for Zensar's recovery?

A: The primary catalysts would be a reacceleration in quarterly revenue growth in constant currency terms, large deal wins demonstrating competitive strength, and a broad recovery in IT services demand from US and European enterprise clients who have been cautious on discretionary technology spending.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Investors should conduct independent due diligence and consult a SEBI-registered investment adviser before making any financial decisions.