Castrol India Ltd (NSE: CASTROLIND) has long been one of the most reliable income stocks in the Indian mid-cap space, and the current data confirms why: a 91.11% payout ratio, ROCE of 60.27%, and a 4.75% trailing yield at Rs 184.80. The lubricants business is capital-light, brand-driven and cash-generative — a combination that supports high shareholder payouts without compromising the operating model.

Key Highlights

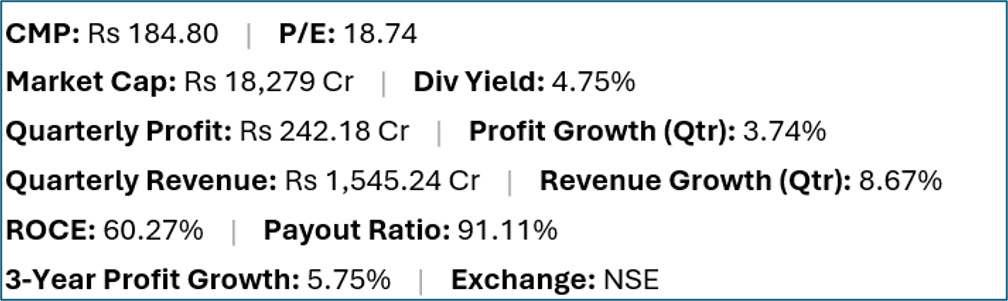

- Castrol India (NSE:CASTROLIND) offers a trailing dividend yield of 4.75% at a current market price of Rs 184.80.

- Quarterly net profit stood at Rs 242.18 crore, representing a 3.74% change year-on-year on revenues of Rs 1,545.24 crore (8.67% change).

- Return on capital employed (ROCE) stands at 60.27%, with a dividend payout ratio of 91.11%.

- Market capitalisation is approximately Rs 18,279 crore. Three-year profit growth is 5.75%.

Financial Snapshot

Company Overview and Business Model

Castrol India is the listed Indian subsidiary of Castrol Limited, part of the global bp (British Petroleum) group. The company manufactures and markets automotive and industrial lubricants, including engine oils, transmission fluids, gear oils, greases and specialty fluids for passenger cars, commercial vehicles, two-wheelers and industrial machinery.

Castrol's Indian operation has been one of the most profitable lubricant businesses in the country for decades, benefiting from brand recognition built through decades of marketing investment, a wide distribution network spanning urban and rural India, and a product portfolio that spans both premium and mass-market segments. The company operates manufacturing facilities in India and sources some products from the global bp supply chain.

The lubricants business in India is linked to vehicle kilometres travelled (VKT) and oil-drain intervals — as vehicle ownership grows and VKT rises, lubricant demand follows. Castrol India is also expanding in the industrial lubricants segment, which serves machinery maintenance in manufacturing, mining and infrastructure operations.

Financial Review

Revenue of Rs 1,545.24 crore grew 8.67%, while quarterly profit of Rs 242.18 crore grew a more modest 3.74% — suggesting some cost headwinds. The exceptional ROCE of 60.27% reflects the asset-light model: Castrol India does not own refineries or raw material sources; it blends, packages and distributes, with brand and distribution as the primary competitive assets. The 91.11% payout ratio means the company retains minimal earnings for reinvestment — consistent with its policy of distributing substantially all profits as dividends.

Dividend Profile and History

Castrol India's dividend policy is one of the most shareholder-friendly on the NSE, with a stated approach of distributing substantially all profits over time. The 91.11% payout ratio at Rs 242 crore quarterly profit supports the 4.75% yield robustly. The three-year profit growth of 5.75% is modest but positive, meaning dividends have also grown over the period. Risk to the dividend would primarily come from a significant contraction in base oil prices (which could compress margins if retail lubricant prices also fall) or a structural shift in vehicle ownership toward EVs (which require different or no traditional engine oil).

Future Outlook

Castrol India's near-term outlook is supported by vehicle parc growth in India. The two-wheeler segment — India's largest vehicle category by number — remains a strong contributor to lubricant volumes. In the medium term, EV penetration is the structural headwind that the market watches: battery-electric two-wheelers and cars do not use conventional engine oil, and as their share of the vehicle parc grows, demand for traditional lubricants will face pressure. However, the internal combustion engine (ICE) vehicle base is large and will continue to require lubricants for many years given typical vehicle lifespans.

Investor Insights

- ROCE of 60.27% confirms that Castrol India's brand-and-distribution model is genuinely capital-efficient — it earns very high returns on the modest physical and working capital the business requires.

- The 91.11% payout ratio means income investors are effectively receiving a pass-through of the company's earnings, with minimal reinvestment. This is high-yield but low-growth by design.

- EV transition risk is real but long-tailed for Castrol India: the existing ICE parc in India is vast, and even aggressive EV adoption targets leave a large lubricant-demand base for the medium term.

- As a subsidiary of bp, Castrol India benefits from global technology and supply chain access but is also subject to parent company strategic decisions on capital allocation.

Frequently Asked Questions

Q: What is Castrol India's dividend policy?

A: Castrol India has a policy of distributing substantially all free cash flow as dividends. The 91.11% payout ratio reflects this approach. Dividends are paid in both interim and final tranches during the year.

Q: Does the EV transition affect Castrol India?

A: Yes, in the long term. Electric vehicles do not use conventional engine oil. As EV penetration grows in India, Castrol India's traditional lubricant volumes will face headwinds. However, Castrol is also developing EV-specific fluids (thermal management, e-axle fluids) to address this transition.

Q: Why is Castrol India's ROCE so high?

A: Castrol's 60.27% ROCE reflects the capital-light blending and distribution model. The company does not require significant fixed-asset investment to generate revenues — its primary assets are the Castrol brand, its distribution relationships, and its working capital. High brand-driven pricing power amplifies returns.

Q: Is Castrol India a buy for income investors?

A: This is general commentary only, not personal financial advice. Castrol India's income credentials are strong — high yield, high payout, high ROCE — but the EV transition is a long-term consideration that investors should factor into their holding horizon.

Conclusion

Castrol India is one of the most consistently income-oriented stocks on the Indian market, and this screen captures its strengths well: a 60.27% ROCE underpins a 91.11% payout that delivers a 4.75% yield from a capital-light, brand-driven lubricants business. The near-term picture is sound, but the EV transition is the question that every Castrol India shareholder must eventually answer for their own investment horizon. For the current period, the income credentials remain difficult to argue with.