Source: company BSE/NSE filings. Verify current data at bseindia.com and nseindia.com

Company Overview

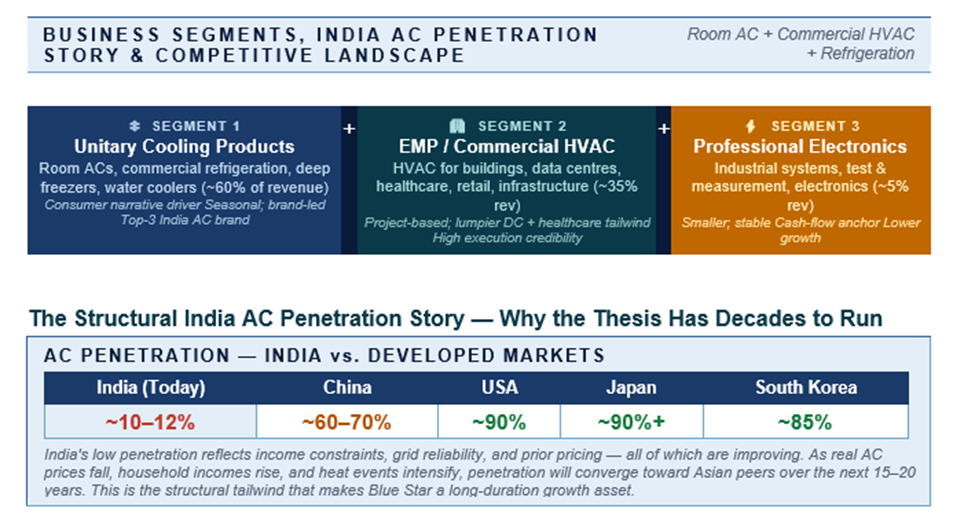

Blue Star Limited (BSE/NSE:BLUESTARCO) is one of India's leading air-conditioning and commercial refrigeration companies, with a presence across three principal segments: unitary cooling products (room air conditioners and commercial refrigeration), electro-mechanical projects and packaged air conditioning (HVAC) for commercial buildings, retail, hospitals, factories, and data centres, and professional electronics and industrial systems. The company is among the top three room AC brands in India and holds leadership positions in commercial refrigeration and project-based HVAC.

Blue Star benefits from two distinct growth themes. First, the structural rise in room-AC penetration in India — still in the low-teens versus 90%+ in developed markets — driven by rising household incomes, declining real prices, increasing awareness of heat-related health impacts, and climate-driven demand. Second, the commercial-HVAC opportunity tied to the broader capex cycle: data centres, retail, healthcare, hospitality, factories, and infrastructure projects all require sophisticated HVAC systems.

Financial Performance & Insights

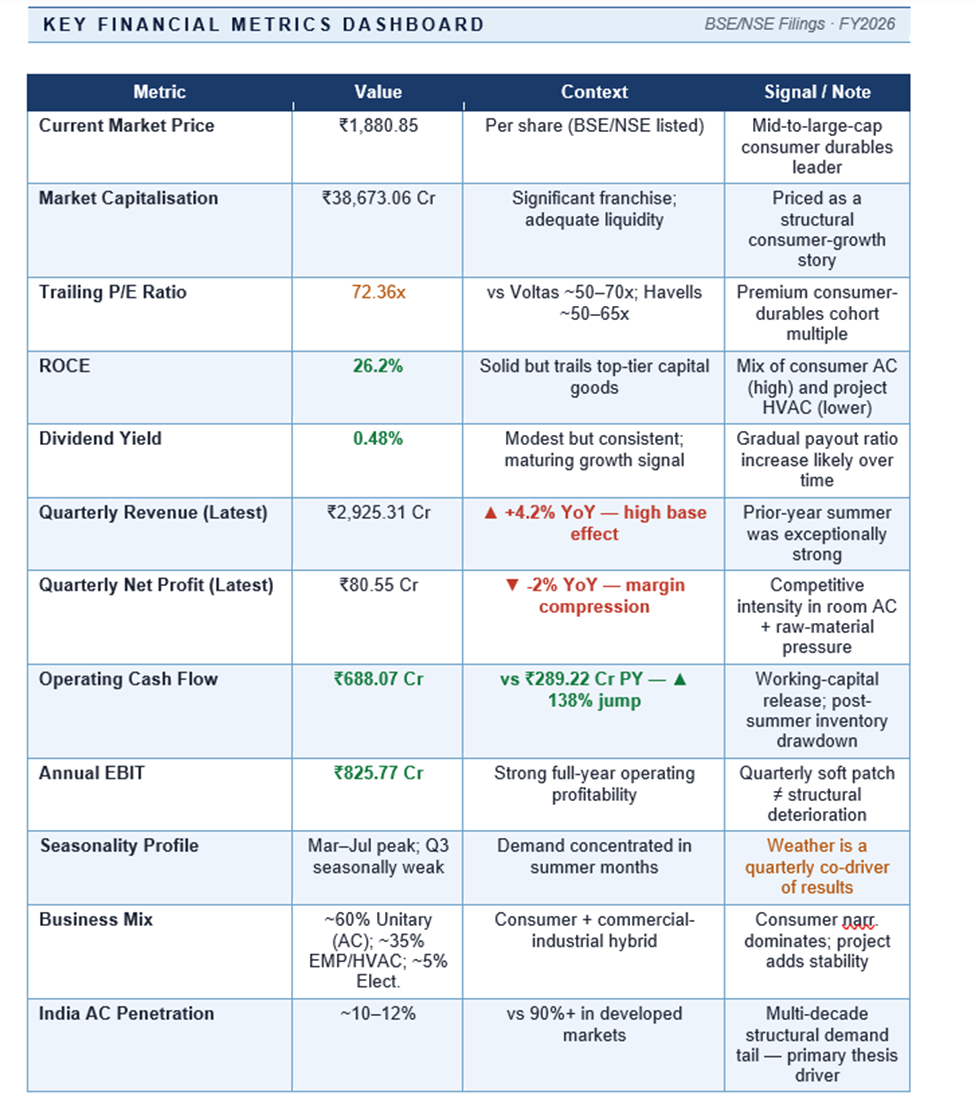

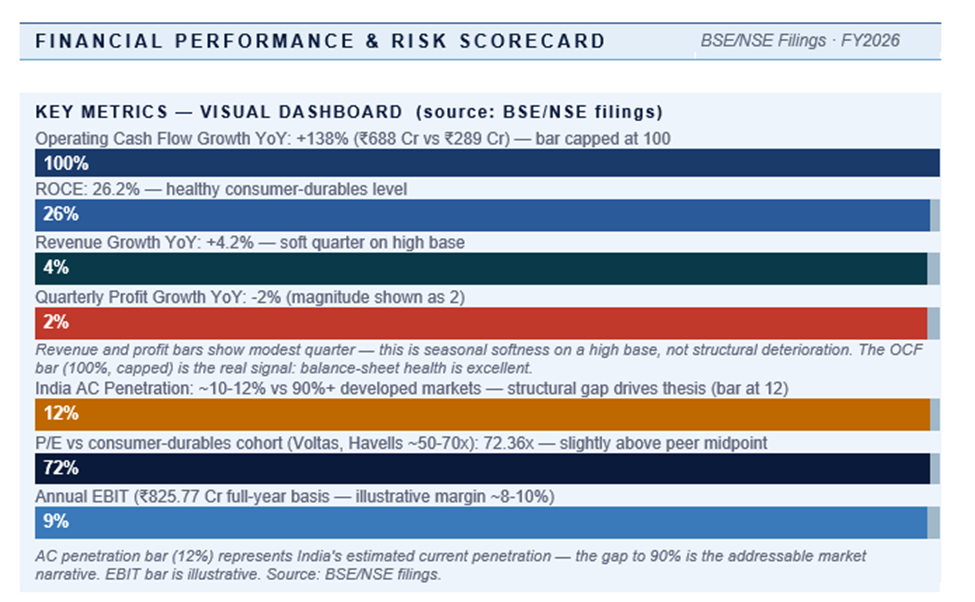

The latest quarter is a softer print than the longer-term trajectory. Revenue of ₹2,925.31 crore grew 4.2% YoY — a meaningfully decelerated rate that likely reflects a high base from a strong prior-year summer, channel inventory normalisation, and some softening in commercial-project ordering. Net profit of ₹80.55 crore was down 2%, indicating modest margin compression driven by competitive intensity in room ACs and raw-material pressure.

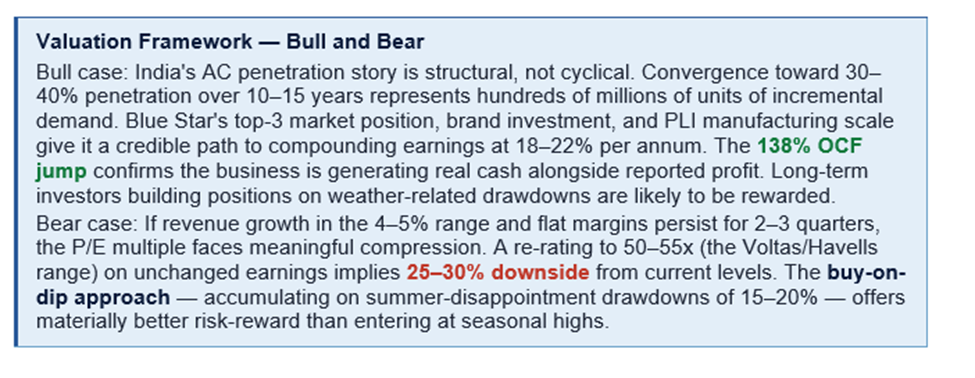

The standout positive is operating cash flow: ₹688.07 crore versus ₹289.22 crore — a 138% jump. This magnitude of cash-flow improvement against modest revenue growth almost always reflects a working-capital release — inventory drawdown, receivables collection, or both. For a seasonal business like Blue Star, this is the right phase of the cycle to release working capital, and management appears to have executed it well.

ROCE of 26.2% remains healthy. Annual EBIT of ₹825.77 crore confirms a strong full-year operating profit base. The current quarterly soft patch should not obscure the structural earnings power — investors should anchor their view to full-year and multi-year trends rather than any individual off-peak quarter.

Price Performance

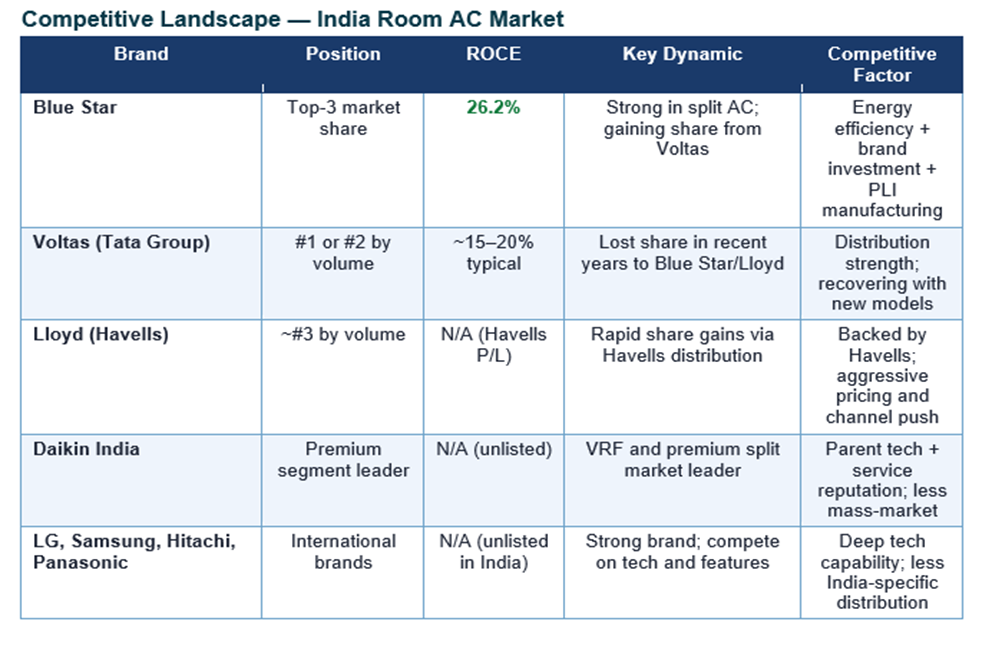

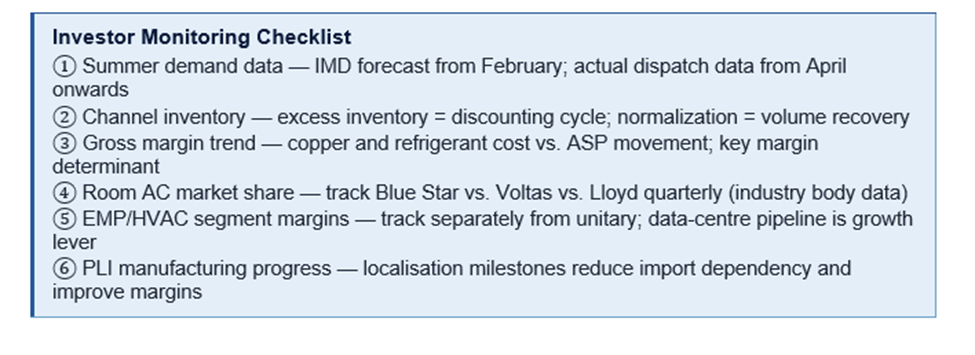

Blue Star has rerated meaningfully over the past three to four years as the room-AC story moved from cyclical-discretionary to structural-staple in investor framing. Voltas, the historical AC leader, has lost share to Blue Star and Lloyd, contributing to Blue Star's outperformance within the cohort. Year-to-year price action is heavily influenced by summer severity — a hot summer drives volume and a mild summer disappoints — making the stock a quasi-weather play in addition to a structural growth story.

Near-term price action will be sensitive to the upcoming summer demand, channel-inventory levels, raw-material movement (copper, aluminium, refrigerants), and any margin commentary. Volatility around quarterly results is meaningful given the seasonal nature of the business. A buy-on-dip approach — accumulating around weather-related drawdowns or weak channel-inventory news — typically offers better risk-reward than entering at peak seasonal sentiment.

Shareholder Returns & Capital Allocation

Blue Star pays a 0.48% dividend yield — modest but consistent. The capital allocation framework retains the bulk of earnings for capacity expansion (the company has been adding AC manufacturing capacity under PLI), inventory build for the seasonal cycle, and brand investment. Long-term shareholder returns have come predominantly from share-price appreciation as the AC penetration story has compounded.

The dividend signal is consistent with a maturing growth business: paying enough to confirm financial discipline and shareholder orientation, retaining enough to fund continued growth investment. A gradual rise in payout ratio over time is a reasonable expectation as growth capex moderates.

Key Risks

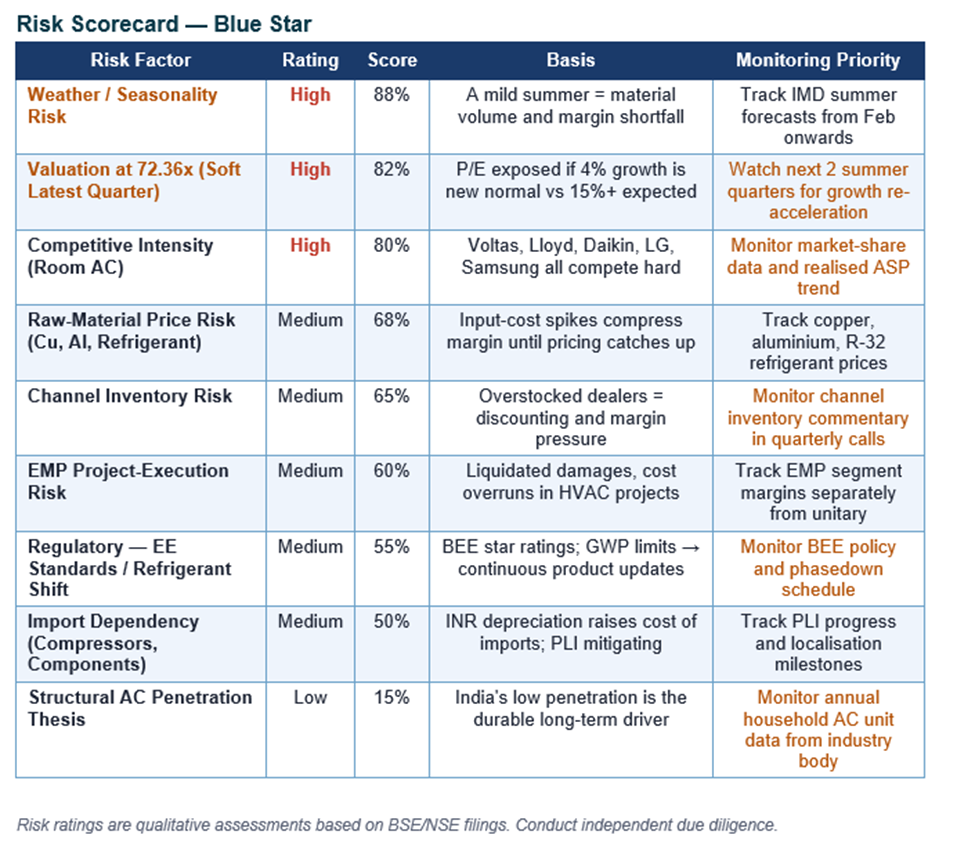

1 — Weather and Seasonality Risk (Intrinsic)

Weather and seasonality risk is intrinsic and cannot be diversified away within the stock. A mild or wet summer can cause room AC volumes to disappoint materially, and the calendar concentration of demand in March–July magnifies the impact of any disruption. Blue Star's quarterly results in off-peak periods (October-December) are not representative of annual earning power.

2 — Valuation Risk at 72.36x

At a P/E of 72.36 with the latest quarter showing 4.2% revenue growth and a 2% profit decline, the multiple is exposed if the slowdown extends. Investors should stress-test the position against a scenario where revenue growth stays in the 5–8% range for two to three quarters — the implied forward P/E would still be elevated, creating downside risk even without a sector-wide de-rating.

3 — Other Risks

- Competition: Voltas, Lloyd (Havells), Daikin, LG, Samsung, Hitachi, and Panasonic all compete aggressively in room ACs, and pricing is regularly tested in peak seasons.

- Raw-material risk: Copper, aluminium, steel, and refrigerant gases (R-32, R-410A) drive cost structure; sustained spikes compress margins.

- Channel-inventory risk: AC distribution is dealer-driven; overstocked channels lead to discounting and margin pressure.

- Regulatory risk: Energy-efficiency standards and refrigerant transition (GWP regulations) requiring continuous product investment.

- EMP project risk: The HVAC project segment is exposed to execution risks — liquidated damages, cost overruns, and customer disputes.

Valuation

At a P/E of 72.36x and a market cap of ₹38,673 crore, Blue Star is priced for sustained 18–22% earnings growth over multiple years. The bull case rests on AC penetration having a multi-decade runway, market-share gains within the AC cohort, and operating leverage from scaling local manufacturing. On these assumptions, current valuation is acceptable for long-term investors.

Business Strategy & Outlook

Strategy is built on four pillars. First, lead the room-AC penetration cycle through brand investment, distribution expansion (especially in Tier-2/3 cities and rural India), and energy-efficient product positioning. Second, scale local manufacturing under PLI to reduce import dependence and improve margins as scale effects compound.

Third, win in commercial HVAC by leveraging brand credibility for data centres, healthcare, and large infrastructure projects — segments seeing accelerated capex. Fourth, manage the channel with discipline — dealer relationships and credit — to avoid the boom-bust dynamics that have hurt peers historically.

The 138% jump in operating cash flow alongside modest profit growth suggests a deliberate working-capital reset and improved channel management. The next watch-items are summer demand, channel re-stocking, and updates on AC manufacturing capacity additions under PLI.

Frequently Asked Questions

Q1. What does Blue Star do?

It is one of India's top-three room-AC brands, a leader in commercial refrigeration, and a major provider of HVAC project services for commercial buildings, data centres, healthcare, and infrastructure.

Q2. Why was the latest quarter weak?

Revenue growth of 4.2% reflects a high prior-year base (strong summer), channel inventory normalisation, and some softness in project ordering. Profit fell 2% on margin compression from competitive intensity and raw-material pressure. This is seasonal and cyclical softness — not a structural reversal.

Q3. Why did operating cash flow jump 138%?

A working-capital release — inventory drawdown and receivables collection — normal for the post-summer phase of the seasonal cycle. This is a positive signal: the business generated more real cash than the P&L shows, and management executed the inventory and receivables discipline well.

Q4. What is the long-term investment thesis?

India's AC penetration is in the low-teens versus 90%+ in developed markets. Rising incomes, climate change, and grid stability all point to multi-decade volume growth, with Blue Star positioned to capture share through brand, distribution, and local manufacturing. The commercial-HVAC segment adds a capex-cycle tailwind via data centres and infrastructure.

Q5. What are the key risks?

Valuation at 72x with a soft latest quarter, weather/seasonality (a mild summer = material disappointment), intense competition (Voltas, Lloyd, Daikin, LG, Samsung, Hitachi), raw-material volatility, channel-inventory risks, and project-execution risks in the EMP/HVAC segment.