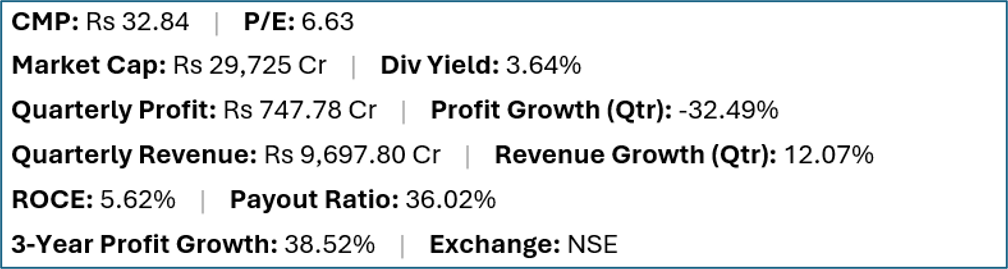

Central Bank of India (NSE: CENTRALBK), one of India's older public sector banks, reported a 32.49% decline in quarterly profit to Rs 747.78 crore even as revenue grew 12.07% to Rs 9,697.80 crore. The divergence between growing revenues and falling profits is a characteristic banking pattern when credit costs rise — and it is the primary feature that income investors must examine before the 3.64% trailing yield becomes the headline consideration.

Key Highlights

- Central Bank of India (NSE:CENTRALBK) offers a trailing dividend yield of 3.64% at a current market price of Rs 32.84.

- Quarterly net profit stood at Rs 747.78 crore, representing a -32.49% change year-on-year on revenues of Rs 9,697.80 crore (12.07% change).

- Return on capital employed (ROCE) stands at 5.62%, with a dividend payout ratio of 36.02%.

- Market capitalisation is approximately Rs 29,725 crore. Three-year profit growth is 38.52%.

Financial Snapshot

Company Overview and Business Model

Central Bank of India is a public sector bank with a history stretching back to 1911, headquartered in Mumbai. The bank operates through a large branch network primarily across central, eastern and western India, serving retail, agricultural and MSME customers alongside corporate banking. It is classified as a public sector undertaking under the Government of India, with the government holding a majority stake.

Central Bank has been on a financial recovery path after a period of elevated non-performing assets (NPAs) and capital adequacy pressure that required government capital support. The bank has gradually improved its NPA ratios and capital position, but it remains a mid-sized PSU bank with lower return ratios than the stronger public sector peers (like SBI or Bank of Baroda) or private sector banks.

PSU bank dividends are partly a function of government fiscal policy — the government collects dividends from banks it owns and factors these into the union budget — creating a structural incentive to pay dividends even in periods of uneven profitability.

Financial Review

Revenue growth of 12.07% to Rs 9,697.80 crore alongside a 32.49% profit fall to Rs 747.78 crore is the classic sign of rising credit provisions — the bank is recognising higher losses on its loan book, which is being charged through the profit and loss account. ROCE of 5.62% is the lowest-but-one on the entire screen (Mawana Sugars aside), reflecting the capital-intensive and low-return-on-equity nature of PSU banking. Three-year profit growth of 38.52% reflects recovery from a very troubled prior period, not a sustainably strong profitability trajectory.

Dividend Profile and History

The 3.64% yield at a 36.02% payout ratio means Central Bank is distributing just over a third of its profits. The 32.49% quarterly profit decline has already reduced the earnings base supporting the dividend, and if credit costs remain elevated in subsequent quarters, further dividend pressure is plausible. Government ownership provides structural incentive to maintain dividends, but at reduced profit levels the absolute payout will likely be smaller.

Future Outlook

Central Bank's outlook is tied to its asset quality trajectory, loan growth in its focus segments (agriculture, MSME, retail), and net interest margin trends. India's broader banking sector has seen asset quality improve from the NPA crisis peaks, and Central Bank has been a beneficiary of this cycle. However, the current quarter's profit decline suggests some reversal of that improvement. The government's continued ownership and capital support if needed provides a degree of financial stability that smaller private banks lack.

Investor Insights

- A 32.49% profit decline in a bank almost always points to higher provisions — investors should read the quarterly results for gross NPA, net NPA and provision coverage ratios before drawing conclusions.

- ROCE of 5.62% in a bank reflects low return on equity and high leverage — PSU banks in India typically trade at discounts to book value for this reason.

- Three-year profit growth of 38.52% is a recovery number, not a growth number — it reflects how bad things were three years ago rather than a sustainable earning trajectory.

- Government ownership is a double-edged sword: it provides capital support when needed but also means lending decisions can be influenced by policy priorities, which can affect asset quality over time.

Frequently Asked Questions

Q: Why did Central Bank of India's profit fall 32.49%?

A: In banking, a profit decline alongside revenue growth typically signals higher provisions for bad loans (NPAs). Investors should check the bank's quarterly results for specific NPA and provision data.

Q: Is Central Bank of India's dividend reliable?

A: Government ownership creates structural incentive to pay dividends, but the 32.49% profit decline will reduce the absolute dividend. The 36.02% payout ratio provides some buffer, but sustained high provisions would eventually force a payout reduction.

Q: What is Central Bank of India's NPA situation?

A: Central Bank has been on a recovery trajectory from elevated NPA levels, but the current quarter's profit decline suggests potential asset quality pressure. Investors should review the latest Basel III disclosure and quarterly results for current NPA ratios.

Q: Is Central Bank of India suitable for income investors?

A: This is general commentary only. The yield is backed by government ownership incentives but is under pressure from declining profits. PSU bank income investing requires tolerance for asset quality volatility and low return on equity.

Conclusion

Central Bank of India's 3.64% yield is a government-backed income story operating against a difficult quarterly backdrop: profit fell 32.49% even as revenues grew, suggesting rising credit costs. The three-year recovery trajectory from NPA highs gives the long-term story some credibility, but income investors should not rely on the trailing yield as an indicator of near-term distributions without examining the bank's asset quality disclosures carefully. This is a yield with uncertainty, not a yield with comfort.