Cravatex Ltd is a BSE-listed company that operates the FILA brand in India — a globally known Italian sportswear label. The stock offers a 3.39% trailing dividend yield at Rs 384.25, and a quarterly profit of Rs 1.60 crore that grew 11.11%. However, the critical number on this entry is the 34.72% revenue contraction to Rs 39.51 crore — a sharp sales decline that raises direct questions about the business's near-term financial health.

Key Highlights

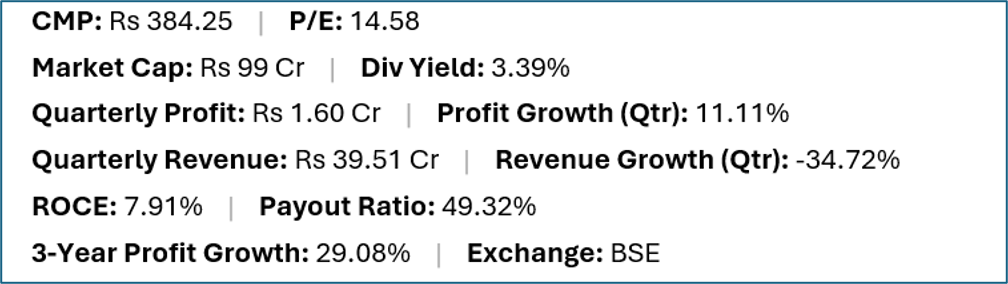

- Cravatex (BSE:CRAVATEX) offers a trailing dividend yield of 3.39% at a current market price of Rs 384.25.

- Quarterly net profit stood at Rs 1.60 crore, representing a 11.11% change year-on-year on revenues of Rs 39.51 crore (-34.72% change).

- Return on capital employed (ROCE) stands at 7.91%, with a dividend payout ratio of 49.32%.

- Market capitalisation is approximately Rs 99 crore. Three-year profit growth is 29.08%.

Financial Snapshot

Company Overview and Business Model

Cravatex holds the India rights for the FILA brand of athletic and lifestyle footwear and apparel, and for the Proline brand, a domestic sportswear label that serves a more value-oriented segment. The company distributes these brands through a combination of exclusive brand outlets, multi-brand sports retail chains and e-commerce platforms.

FILA is a heritage Italian sportswear brand that has found renewed relevance globally through a nostalgia-driven fashion cycle and strategic repositioning by its South Korean parent company (Fila Holdings Corp). In India, the brand competes in a market dominated by Nike, Adidas, Puma and Reebok, with FILA sitting in a premium-but-accessible positioning.

At a market cap of Rs 99 crore, Cravatex is a micro-cap by Indian standards. Brand distribution businesses for international labels can carry meaningful fixed costs (store rentals, staff, marketing commitments) relative to the revenue base, making the P&L more sensitive to top-line volatility than a manufacturing business.

Financial Review

Revenue of Rs 39.51 crore falling 34.72% year-on-year is a severe top-line contraction for a small business. Profit of Rs 1.60 crore growing 11.11% despite this revenue fall could reflect cost reduction, but a Rs 1.60 crore profit on a Rs 39.51 crore revenue base represents a thin 4% margin with very little earnings cushion. ROCE of 7.91% is low. Three-year profit growth of 29.08% suggests the business has recovered meaningfully from a prior earnings trough, though the current revenue collapse introduces fresh uncertainty.

Dividend Profile and History

The 3.39% trailing yield from a company earning Rs 1.60 crore of quarterly profit should be treated carefully. The absolute annual dividend amount from Cravatex at current earnings would be small in rupee terms, and the 34.72% revenue decline is the immediate risk factor. If revenues do not recover in coming quarters, the profit base — already thin — could deteriorate, and dividend sustainability would be at risk.

Future Outlook

Cravatex's recovery depends on stabilising and growing FILA brand revenues in India. A 35% revenue decline is likely to reflect a combination of market challenges: reduced retail footfall in specialty sports stores, competitive pressure from larger brands with stronger marketing budgets, and potentially the unwinding of a post-pandemic demand recovery. The global FILA brand positioning refresh (heritage sportswear aesthetic) is an asset if executed well in India, but the company lacks the marketing scale of its direct competitors. Revenue recovery, not dividend yield, is the most important variable to track for this name.

Investor Insights

- A 34.72% revenue decline alongside a 11.11% profit growth is only possible if costs fell even faster than revenues — investors should examine the cost structure for one-time reductions or lease modifications.

- At Rs 99 crore market cap, Cravatex is the second-smallest company on this screen by market cap — liquidity and governance risks are relevant.

- The FILA brand's global resurgence is a tailwind, but in India the company lacks the advertising and distribution scale of Nike, Adidas or Puma, limiting how much brand momentum translates to Cravatex's revenues.

- Three-year profit growth of 29.08% from a low base needs to be reconciled with the current sharp revenue decline — investors should compare the revenue level today with three years ago, not just the profit.

Frequently Asked Questions

Q: What brands does Cravatex distribute in India?

A: Cravatex holds the India rights for the FILA international sportswear brand and also markets the Proline domestic sportswear label, distributed through brand stores, multi-brand sports outlets and e-commerce.

Q: Why did Cravatex's revenue fall 34.72%?

A: A 34.72% revenue decline is severe and likely reflects a combination of reduced brand retail demand, store count changes, competitive pressure and potentially the unwind of post-pandemic demand normalisation. Investors should read the management commentary in the quarterly filing for the specific explanation.

Q: Is Cravatex's 3.39% yield safe?

A: With quarterly revenue falling 35% and profit of only Rs 1.60 crore, the earnings base is fragile. The yield is covered at current profit levels, but a further revenue decline without corresponding cost reduction would quickly compress or eliminate the profit base.

Q: Is Cravatex suitable for income investors?

A: This is general commentary only. The yield is real but the revenue trajectory is concerning. Investors should not rely on the trailing yield without understanding the cause and likely duration of the revenue contraction.

Conclusion

Cravatex closes this list with the lowest yield (3.39%) and one of the most concerning revenue trends: a 34.72% quarterly sales decline. The profit growth of 11.11% despite this revenue fall is an accounting curiosity that requires explanation rather than celebration. For income investors, Cravatex's headline yield is supported by thin earnings that are now dependent on a revenue trajectory moving in the wrong direction. This is a name to monitor closely, not one to rely on for stable income without first understanding what drove the revenue collapse and whether it is reversible.