Credo Brands Marketing Ltd (NSE: CREDOBRANDS) is the company behind the Mufti apparel brand, one of India's established men's casual fashion labels. With a 3.49% trailing yield at Rs 86.09 and a quarterly profit of Rs 15.23 crore growing 10.12%, the company offers modest income credentials — though the three-year profit decline of -14.64% is a context-setter that income investors cannot ignore.

Key Highlights

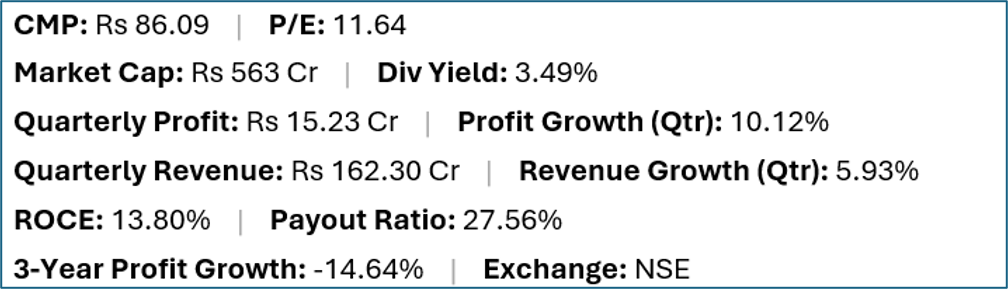

- Credo Brands Marketing (NSE:CREDOBRANDS) offers a trailing dividend yield of 3.49% at a current market price of Rs 86.09.

- Quarterly net profit stood at Rs 15.23 crore, representing a 10.12% change year-on-year on revenues of Rs 162.30 crore (5.93% change).

- Return on capital employed (ROCE) stands at 13.80%, with a dividend payout ratio of 27.56%.

- Market capitalisation is approximately Rs 563 crore. Three-year profit growth is -14.64%.

Financial Snapshot

Company Overview and Business Model

Credo Brands Marketing is the exclusive licensee and marketing company for the Mufti brand of men's apparel in India. Mufti is positioned in the premium casual and smart-casual segment — above mass-market retail brands like Fabindia or Shoppers Stop house brands, but below the luxury tier. The brand's distribution spans exclusive brand outlets (EBOs), multi-brand outlets (MBOs) and e-commerce platforms.

The company's business model involves design, sourcing (from third-party manufacturers), brand management and retail distribution — it does not own manufacturing facilities, making it an asset-light brand house. This model is common in Indian apparel where brand owners focus on design and sales while outsourcing production. Revenue and margins depend on brand strength, retail expansion, and the ability to hold pricing in a competitive market that includes international fast-fashion brands.

Financial Review

Revenue of Rs 162.30 crore grew 5.93% and profit of Rs 15.23 crore grew 10.12% — positive but unspectacular figures. ROCE of 13.80% is moderate for a brand-led consumer company. The payout ratio of 27.56% is conservative relative to the 3.49% yield, suggesting the yield is supported by a generous absolute payout given the current share price rather than an aggressive distribution policy. The three-year profit decline of -14.64% indicates the post-pandemic retail environment has been difficult for Mufti relative to its pre-pandemic earnings.

Dividend Profile and History

The 3.49% yield at a 27.56% payout ratio has reasonable earnings coverage given the current profit level, but the three-year declining profit context is the caveat. If revenues and profits continue to recover from the post-pandemic dip, the income case improves; if growth stalls at current modest levels, the dividend at current payout remains stable but is unlikely to grow meaningfully.

Future Outlook

Credo Brands' growth depends on Mufti's brand health, store expansion and the premiumisation of Indian apparel consumption. The men's premium casual segment is competitive, with brands like UCB, Pepe, Levis and international fast-fashion chains all competing for the same consumer. E-commerce growth is a double-edged sword — it opens distribution but also accelerates price discovery and competition. Credo's ability to maintain brand pricing power and continue recovering profits toward pre-pandemic levels is the key earnings narrative.

Investor Insights

- A three-year profit decline of -14.64% signals the business has not fully recovered from pandemic-related disruption — the current quarterly improvement (10.12%) is encouraging but needs to be sustained.

- The 27.56% payout ratio is conservative — the dividend could grow without straining finances if profits recover, but it also means the current yield is not a reflection of maximum payout capacity.

- Mufti's brand is established but operates in a highly competitive mid-premium apparel segment; maintaining differentiation against international fast-fashion and domestic competitors requires ongoing brand investment.

- At P/E 11.64 with a recovering earnings trajectory, the valuation is not demanding — but investors should track whether the quarterly recovery is being driven by volume growth or one-time factors.

Frequently Asked Questions

Q: What is Credo Brands and what brand does it own?

A: Credo Brands Marketing is the company behind the Mufti brand of premium men's casual apparel in India. It manages brand licensing, design, sourcing and retail distribution for the brand without owning manufacturing facilities.

Q: Why has Credo Brands shown a three-year profit decline?

A: The -14.64% three-year profit decline reflects the disruption to retail operations and consumer spending during and after the pandemic period. Specialty apparel brands were among the harder-hit categories during retail closures.

Q: Is Credo Brands' 3.49% yield safe?

A: The 27.56% payout ratio gives reasonable earnings coverage, and the quarterly profit is currently growing (10.12%). The yield appears relatively stable at current earnings, though recovery to pre-pandemic profitability is needed for meaningful dividend growth.

Q: Is Credo Brands suitable for income investors?

A: This is general commentary only. Credo offers a modest yield from an established apparel brand, but the three-year earnings decline and competitive retail environment are factors to weigh carefully.

Conclusion

Credo Brands' 3.49% yield reflects a company that is recovering from a difficult three-year period but has not yet reached the profitability levels that would make the income case compelling. The Mufti brand is established, the business model is asset-light, and the current profit growth is encouraging. However, income investors seeking reliable and growing distributions should wait for at least two to three consecutive quarters of profit recovery before treating Credo as a dependable income stock.