Crizac Ltd (NSE: CRIZAC) brings the second-highest ROCE on this dividend screen at 52.34% alongside a 50.26% quarterly profit jump to Rs 74.50 crore — making it one of the more unusual income names on the list. It is not an oil company or a PSU: Crizac is an education services business, specifically a B2B platform for international student recruitment, and its high returns on capital reflect the asset-light economics of a tech-enabled service business operating in a fast-growing market.

Key Highlights

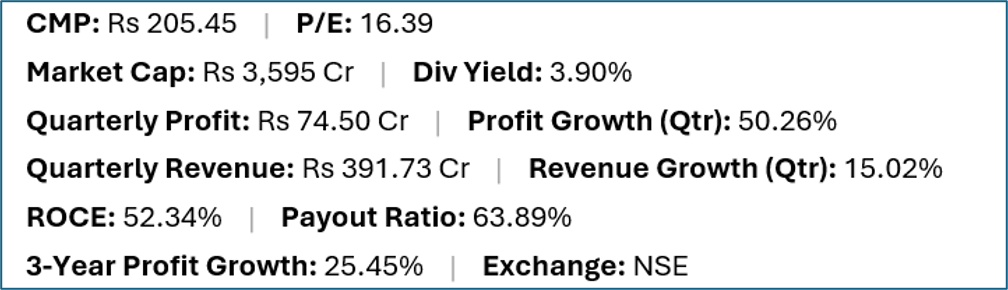

- Crizac (NSE:CRIZAC) offers a trailing dividend yield of 3.90% at a current market price of Rs 205.45.

- Quarterly net profit stood at Rs 74.50 crore, representing a 50.26% change year-on-year on revenues of Rs 391.73 crore (15.02% change).

- Return on capital employed (ROCE) stands at 52.34%, with a dividend payout ratio of 63.89%.

- Market capitalisation is approximately Rs 3,595 crore. Three-year profit growth is 25.45%.

Financial Snapshot

Company Overview and Business Model

Crizac operates a B2B platform connecting overseas education institutions (universities and colleges primarily in the UK, Canada, Australia and Ireland) with a network of education agents and consultancies that guide Indian and international students through the application and admission process. Rather than recruiting students directly, Crizac's platform aggregates demand from the agent network and institutional supply from partner universities, earning fees from successful student placements.

This model is distinct from both direct-to-student platforms (like Leap Scholar or iSchoolConnect) and from traditional education consultancies. By operating as infrastructure for the agent ecosystem rather than competing with agents, Crizac avoids the high customer acquisition costs of direct-to-consumer models and benefits from network effects as more agents and institutions join the platform.

The international student mobility market has grown significantly in recent years, with India consistently one of the largest source countries for students studying in English-speaking destinations. Visa policy changes — including UK post-study work route extensions and Canadian student visa tightening — create periodic volatility in destination country flows but do not eliminate the underlying demand for international education facilitation.

Financial Review

Revenue of Rs 391.73 crore grew 15.02%, while profit surged 50.26% to Rs 74.50 crore — indicating strong operating leverage as the platform scales. An ROCE of 52.34% is exceptional and reflects the capital-light nature of the B2B platform model, where technology and relationships rather than physical assets drive the business. The payout ratio of 63.89% at quarterly profit of Rs 74.50 crore means the absolute dividend is growing as profits expand. Three-year profit growth of 25.45% confirms the compounding quality of the earnings.

Dividend Profile and History

The 3.90% trailing yield at a 63.89% payout ratio and growing profits gives Crizac one of the stronger dividend growth profiles on this screen. Unlike names where earnings are flat or declining, Crizac's 50.26% quarterly profit growth and 25.45% three-year track mean the absolute dividend has been rising, making the trailing yield potentially understated relative to what a forward yield calculation would show.

Future Outlook

Crizac's growth outlook depends on continued international student mobility from India, the company's ability to expand its agent network and institutional partnerships, and its platform's ability to process a growing volume of applications at scale. The UK and Canada remain the most important destination markets; UK policy on student visas and Canadian changes to permit caps are the primary policy variables to monitor. Over the medium term, the company's expansion into new destination countries (e.g., Germany, New Zealand, continental Europe) would diversify geographic risk.

Investor Insights

- Crizac's 52.34% ROCE combined with 25.45% three-year profit growth makes it arguably the highest-quality earnings combination among the income names on this screen.

- The B2B platform model insulates Crizac from the high customer acquisition costs of direct-to-student businesses — it monetises the agent ecosystem rather than competing with it.

- Canadian student visa policy changes in 2024 created sector-level uncertainty; investors should verify how Crizac's Canada-directed volumes have been affected in recent quarters.

- At P/E 16.39 with 50.26% profit growth, Crizac appears attractively valued relative to its growth rate — a lower PEG ratio than most quality mid-cap growth stocks in India.

Frequently Asked Questions

Q: What does Crizac do?

A: Crizac operates a B2B technology platform connecting international universities with education agents and consultancies that help students from India and other countries apply to study abroad. It earns fees from successful student placements processed through its platform.

Q: Why is Crizac's ROCE so high?

A: At 52.34%, Crizac's ROCE reflects its asset-light business model — it connects institutions with agents through a technology platform, requiring minimal physical capital investment. Its primary assets are its platform, agent network and institutional relationships.

Q: How does Canadian visa policy affect Crizac?

A: Canada tightened international student permit approvals in 2024, which affected volumes for all companies in the student recruitment ecosystem. Crizac's multi-destination model provides some offset, but Canada-directed student flows are a material part of its business.

Q: Is Crizac suitable for income investors?

A: This is general commentary only. Crizac offers a growing dividend backed by high ROCE and strong profit growth — an uncommon combination in the income space. Investors should consider destination country policy risks and assess the company's filings.

Conclusion

Crizac is the most distinctively positioned income name on this screen — not a PSU or a commodity business but a B2B technology platform for international student recruitment with ROCE of 52.34% and 50.26% profit growth. The 3.90% yield is likely understated relative to where forward earnings will deliver the dividend, given the trajectory of profit growth. For income investors who are comfortable with sector-specific policy risk (student visa changes) and want quality growth alongside yield, Crizac is among the most compelling mid-cap names on this list.