Gateway Distriparks Ltd (NSE: GATEWAY) is a logistics company operating container freight stations (CFS) and inland container depots (ICD) with a rail-linked container movement model. A 25.51% quarterly profit jump to Rs 63.70 crore alongside flat revenues (down 0.24%) is an unusual combination that deserves investigation — and it gives the 3.42% trailing yield an improving near-term earnings base.

Key Highlights

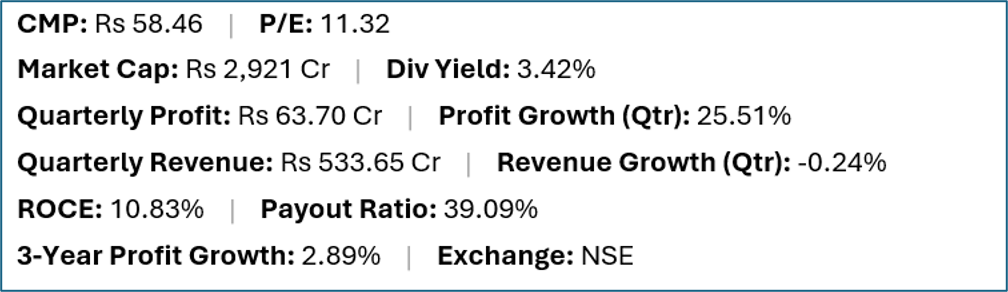

- Gateway Distriparks (NSE:GATEWAY) offers a trailing dividend yield of 3.42% at a current market price of Rs 58.46.

- Quarterly net profit stood at Rs 63.70 crore, representing a 25.51% change year-on-year on revenues of Rs 533.65 crore (-0.24% change).

- Return on capital employed (ROCE) stands at 10.83%, with a dividend payout ratio of 39.09%.

- Market capitalisation is approximately Rs 2,921 crore. Three-year profit growth is 2.89%.

Financial Snapshot

Company Overview and Business Model

Gateway Distriparks operates at the intersection of port logistics and inland container transportation. Its CFS facilities handle import and export containers at or near major ports, providing customs clearance, stuffing, destuffing and storage services for shipping lines and cargo owners. Its rail-linked ICDs move containers between ports and inland locations using dedicated freight corridor and conventional rail services, reducing dependence on road transport.

The company's subsidiary Snowman Logistics operates a cold chain logistics network, adding a temperature-controlled segment to the broader logistics offering. Gateway's model is infrastructure-based: it owns or leases land and equipment at strategic logistics locations, earning fees from container handling, storage and transportation.

The shift of container traffic to rail is a structural tailwind for Gateway's model — rail movement is cheaper per tonne-kilometre than road for long-distance containers, and the government's dedicated freight corridor (DFC) network is improving both speed and capacity for rail logistics.

Financial Review

Revenue of Rs 533.65 crore was essentially flat (down 0.24%), yet profit grew 25.51% to Rs 63.70 crore — indicating a significant margin improvement, likely from cost management, operating leverage on the existing asset base, or a favourable mix shift in services. ROCE of 10.83% is modest for a logistics business, consistent with the infrastructure-heavy model where capital is employed in land and equipment with long payback periods. Three-year profit growth of only 2.89% suggests this is a business with stable but slow-growing earnings over the medium term.

Dividend Profile and History

The 3.42% yield at a 39.09% payout ratio has reasonable earnings coverage. The 25.51% profit jump provides a larger earnings base for the next distribution cycle, which could support a higher absolute dividend. Three-year profit growth of 2.89% means the dividend has grown very little over the medium term, however, making this more of a stable-income than a growing-income story.

Future Outlook

Gateway Distriparks' outlook is supported by the expansion of the dedicated freight corridor network in India, which improves rail logistics speed and reliability — directly benefiting ICD and CFS operators. Container volumes at Indian ports have been growing, driven by export activity and import demand, providing underlying volume growth for CFS operations. The Snowman cold chain subsidiary has growth potential as organised cold chain infrastructure expands in India with food processing investment.

Investor Insights

- Revenue flat while profit grew 25.51% — investors should identify whether this margin expansion is sustainable or reflects one-time items (asset sale gains, provision reversals, etc.).

- Rail-linked logistics is a structurally growing segment in India as the DFC matures; Gateway's ICD model is well-positioned to benefit from traffic shifting from road to rail.

- The 39.09% payout ratio leaves room to grow absolute dividends alongside earnings without a policy change — conservative payout relative to peers.

- Snowman Logistics' cold chain operations are a growth option embedded within Gateway's portfolio — the value of this business is not always explicitly priced in by investors focused on the core CFS/ICD operations.

Frequently Asked Questions

Q: What does Gateway Distriparks do?

A: Gateway Distriparks operates container freight stations (CFS) near major Indian ports and inland container depots (ICD) that move containers between ports and inland locations via rail. Its subsidiary Snowman Logistics operates cold chain warehousing and distribution.

Q: Why did Gateway's profit grow 25.51% despite flat revenues?

A: A profit increase alongside flat revenues indicates margin improvement. This could reflect cost reduction, improved asset utilisation, operating leverage on the existing infrastructure, or a change in revenue mix. Investors should verify the specific driver in the quarterly results commentary.

Q: How does India's dedicated freight corridor benefit Gateway?

A: The DFC provides faster and more reliable rail freight movement, which is the primary logistics mode for Gateway's ICDs. Improved rail transit times make ICD-based container logistics more competitive versus road transport, potentially increasing volumes through Gateway's facilities.

Q: Is Gateway Distriparks suitable for income investors?

A: This is general commentary only. Gateway offers a stable yield from essential logistics infrastructure with a reasonable payout ratio and improving near-term earnings. Investors should review the sustainability of the profit margin improvement before relying on the enhanced earnings base.

Conclusion

Gateway Distriparks offers a 3.42% yield from a logistics infrastructure business that is structurally positioned to benefit from India's rail freight expansion. The 25.51% profit growth on flat revenues is the most interesting feature of the current quarter — if that margin improvement is sustainable, the income case strengthens materially. The three-year profit growth of 2.89% sets a conservative baseline, making near-term margin trajectory the critical variable for investors assessing this stock as an income holding.