Gujarat Intrux Ltd is among the smaller names on this dividend screen, with a market capitalisation of just Rs 150 crore, but it makes the list on the strength of a 5.73% trailing dividend yield at a CMP of Rs 437. For investors who look beyond large-caps for income, Gujarat Intrux represents a niche industrial manufacturer that has maintained shareholder payouts even through a period of declining quarterly profits.

Key Highlights

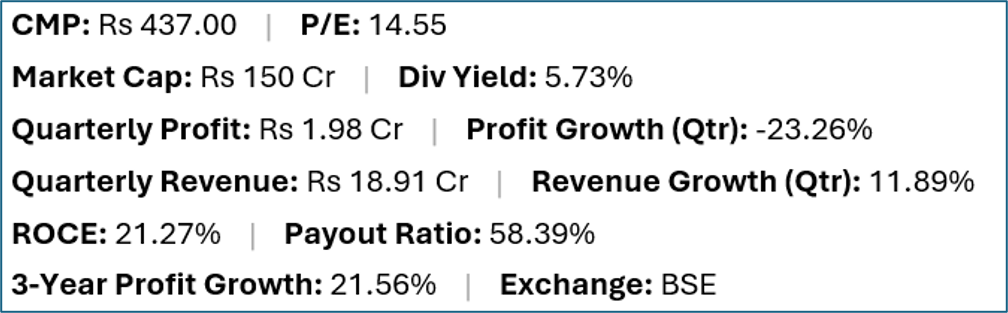

- Gujarat Intrux (BSE:GUJARATINTRUX) offers a trailing dividend yield of 5.73% at a current market price of Rs 437.00.

- Quarterly net profit stood at Rs 1.98 crore, representing a -23.26% change year-on-year on revenues of Rs 18.91 crore (11.89% change).

- Return on capital employed (ROCE) stands at 21.27%, with a dividend payout ratio of 58.39%.

- Market capitalisation is approximately Rs 150 crore. Three-year profit growth is 21.56%.

Financial Snapshot

Company Overview and Business Model

Gujarat Intrux is an Ahmedabad-based manufacturer of industrial valves and investment castings, supplying components used in sectors including oil and gas, chemicals, power, and general engineering. Investment casting — also known as lost-wax casting — produces precision metal parts with complex geometries that cannot be efficiently machined, and the Indian industrial casting segment has historically supplied both domestic end-users and export markets.

The company operates from manufacturing facilities in Gujarat and positions itself as a supplier of both standard and custom-engineered valve and casting products. At a market cap of Rs 150 crore, Gujarat Intrux is a micro-cap by institutional standards, and the stock's liquidity is correspondingly limited — a factor income investors must weigh alongside the headline yield.

Financial Review

Quarterly net profit of Rs 1.98 crore fell 23.26% year-on-year, which is a meaningful decline on a small base. Revenue of Rs 18.91 crore grew 11.89%, suggesting top-line momentum but margin compression, likely from input costs or product mix. ROCE of 21.27% is respectable for a small industrial manufacturer. The three-year profit growth of 21.56% indicates the company has grown earnings over the medium term despite the recent quarterly dip. Payout ratio of 58.39% is high relative to the absolute profit base of under Rs 2 crore per quarter, which means the annual dividend is a significant call on the company's modest cash generation.

Dividend Profile and History

Gujarat Intrux has maintained a dividend despite the small and volatile profit base, which reflects management's commitment to shareholder returns but also means any sustained profit decline would quickly challenge the payout ratio. The 5.73% yield at the current CMP is attractive in isolation, but must be viewed against the fact that the company's quarterly profit is only Rs 1.98 crore — meaning an annual profit in the Rs 7–8 crore range is supporting a meaningful payout. Dividend coverage here is thin relative to the large-caps on this list.

Future Outlook

Gujarat Intrux's outlook is tied to industrial capex activity in its end-user sectors — oil and gas, chemicals and power — where project award activity has been improving with India's infrastructure push. Export demand for precision castings is a potential growth avenue if the company can achieve quality certifications and scale capacity. However, margin pressure from raw material costs (primarily metal alloys) and competition from larger domestic and international casting manufacturers are ongoing challenges. A recovery in quarterly profit toward historical levels would be the key signal for dividend sustainability.

Investor Insights

- At Rs 150 crore market cap, Gujarat Intrux is a micro-cap with limited trading liquidity — investors should check average daily volumes before sizing a position.

- The 23.26% quarterly profit decline on already modest absolute earnings makes the 58.39% payout ratio one of the more stretched on this list in terms of earnings coverage.

- Three-year profit growth of 21.56% shows the business has grown earnings over the medium term, suggesting the current quarter may be a temporary setback rather than a structural deterioration.

- Industrial casting companies are cyclical; demand is closely linked to capex decisions in oil and gas, chemicals, and power — all sectors currently receiving policy support in India.

Frequently Asked Questions

Q: What does Gujarat Intrux manufacture?

A: Gujarat Intrux manufactures industrial valves and investment castings used in oil and gas, chemicals, power and general engineering applications. The company is based in Ahmedabad, Gujarat.

Q: Is the 5.73% yield from Gujarat Intrux sustainable?

A: Sustainability is uncertain given that quarterly profit fell 23.26% to Rs 1.98 crore, making the payout ratio of 58.39% tightly stretched against the current earnings base. Investors should monitor the next two to three quarters of results to assess whether the profit dip reverses.

Q: What are the risks of investing in micro-cap dividend stocks?

A: Micro-cap stocks like Gujarat Intrux carry higher risks: limited liquidity, lower information availability, concentrated customer relationships, and earnings that can be significantly affected by a single large order or cost event. The headline yield may be less reliable than the same yield from a larger company.

Q: Is Gujarat Intrux a buy for income investors?

A: This is general commentary only, not personal financial advice. The yield is real but thinly covered by current earnings. Investors should review filings and assess the profit trajectory before acting.

Conclusion

Gujarat Intrux offers a 5.73% yield from a niche industrial position in valves and investment castings, but the recent profit decline and the thin earnings-to-dividend coverage ratio mean this is not a set-and-forget income stock. The medium-term profit growth record is encouraging, and India's industrial capex cycle could support a recovery. Income investors considering this name should apply a higher margin of safety and check liquidity carefully before entering.