Hindustan Petroleum Corporation Ltd (NSE: HPCL) has delivered one of the more striking quarterly profit rebounds on this list, with net profit surging 77.58% year-on-year to Rs 6,065 crore on revenues of Rs 1,14,937 crore. For a downstream oil marketing company that endured painful marketing losses when crude prices spiked and retail fuel prices were capped, the reversal is substantial. At a trailing P/E of just 4.65 and a dividend yield of 6.15%, the stock has re-entered income-investor conversations.

Key Highlights

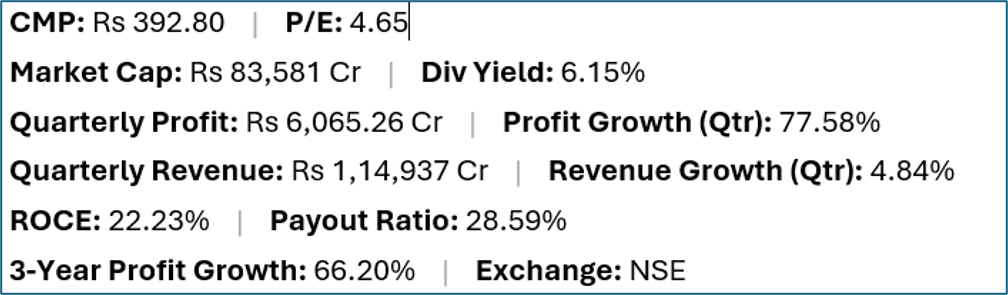

- HPCL (NSE: HPCL) offers a trailing dividend yield of 6.15% at a current market price of Rs 392.80.

- Quarterly net profit stood at Rs 6,065.26 crore, representing a 77.58% change year-on-year on revenues of Rs 1,14,937 crore (4.84% change).

- Return on capital employed (ROCE) stands at 22.23%, with a dividend payout ratio of 28.59%.

- Market capitalisation is approximately Rs 83,581 crore. Three-year profit growth is 66.20%.

Financial Snapshot

Company Overview and Business Model

HPCL is one of India's three major state-owned oil marketing companies (OMCs), alongside Indian Oil Corporation and Bharat Petroleum. The company's core business covers refining crude oil at its refineries in Mumbai and Vishakhapatnam and marketing petroleum products — petrol, diesel, LPG, lubricants and aviation fuel — through a network of retail outlets, pipelines and bulk supply channels across India.

As a government-of-India enterprise with the Government holding a majority stake, HPCL's pricing decisions on key fuel products are influenced by policy considerations, particularly around petrol and diesel retail prices. That political economy dimension is the single most important variable for HPCL's earnings — the spread between international crude prices and domestic retail prices determines whether the company earns a marketing margin or absorbs a marketing loss.

Beyond marketing, HPCL has been investing in expanding refinery capacity. Its Rajasthan Refinery project at Barmer, being developed in partnership with the Rajasthan government under HPCL Rajasthan Refinery Ltd (HRRL), represents the company's most significant long-term capacity investment — though the project has faced timelines and cost scrutiny over successive years.

Financial Review

Quarterly revenue of Rs 1,14,937 crore grew a modest 4.84%, but the profit swing was dramatic: Rs 6,065.26 crore in the latest quarter versus a significantly lower base a year prior. The ROCE of 22.23% indicates reasonable capital efficiency for a capital-intensive refining and marketing business. A relatively low payout ratio of 28.59% — despite the 6.15% yield — reflects the government's requirement for PSUs to pay dividends as a fiscal contribution, but also suggests the yield is supported by the size of absolute profits rather than aggressive payout.

Dividend Profile and History

HPCL has historically been a consistent dividend payer, partly driven by the government's reliance on PSU dividends as a budget revenue line. The 6.15% trailing yield at Rs 392.80 is meaningful for a large-cap, though it is worth noting that HPCL's dividend has varied significantly across years when marketing losses compressed earnings. The three-year profit growth of 66.20% suggests earnings have recovered strongly from the loss-making phase, which strengthens the sustainability argument for the current yield level — provided marketing margins remain positive.

Future Outlook

HPCL's outlook is primarily a function of crude oil prices and the government's willingness to allow periodic retail fuel price adjustments. A sustained period of elevated crude prices without compensatory retail price hikes would compress margins and put dividend sustainability under pressure, as seen in prior cycles. The Rajasthan Refinery project, once commissioned, would add significantly to HPCL's refining capacity and reduce dependence on third-party crude processing, but the capital expenditure associated with it will weigh on free cash flow during the construction phase. LNG and petrochemicals expansion are also on the company's medium-term agenda.

Investor Insights

- HPCL's earnings are highly sensitive to the crude-to-retail price differential. Investors should track monthly fuel pricing decisions and international crude benchmarks alongside quarterly results.

- The P/E of 4.65 is low even by PSU standards, partly reflecting the market's scepticism about the durability of marketing margins in a politically influenced pricing environment.

- A payout ratio of 28.59% means a significant portion of earnings is retained, which may support reinvestment in the Rajasthan refinery but also limits near-term dividend growth.

- HPCL's government ownership is both a support (implied financial backing) and a constraint (pricing decisions are not purely commercial).

Frequently Asked Questions

Q: What drove HPCL's 77.58% profit jump?

A: The sharp profit recovery reflects an improvement in marketing margins — the gap between the cost of refined products and what HPCL charges retail customers. After a period when retail prices were capped below cost, an easing of that pressure allowed margins to normalise. The absolute revenue growth of 4.84% shows volumes were relatively stable, so the profit swing was primarily a margin story.

Q: Is HPCL's 6.15% dividend yield sustainable?

A: The yield is backed by a 28.59% payout ratio and strong quarterly profits, suggesting room for sustainability in a favourable margin environment. The primary risk is a return to the marketing-loss cycle if crude prices spike and retail prices are not adjusted commensurately.

Q: What is the Rajasthan Refinery project?

A: HPCL Rajasthan Refinery Ltd (HRRL) is a joint venture between HPCL and the Rajasthan government to build a large refinery-cum-petrochemical complex at Barmer. It is a major long-term capacity investment but has faced repeated timeline revisions and carries significant capital commitment.

Q: Is HPCL suitable for dividend-focused investors?

A: This is general commentary, not financial advice. HPCL offers a high yield at a low P/E, but the dividend history shows earnings can be volatile depending on government pricing policy. Investors should assess their own risk tolerance and review company filings before deciding.

Conclusion

HPCL's profit rebound and 6.15% yield make it one of the more compelling income names among large-cap PSUs, but the investment case cannot be separated from the political economy of fuel pricing in India. When marketing margins are healthy, as they appear to be currently, HPCL generates strong cash flows and supports a meaningful dividend. The question every HPCL investor must hold in mind is how long that margin environment persists — and what happens to the dividend when it doesn't.