Kuantum Papers Ltd presents one of the more challenged income profiles on this screen: a 45.10% quarterly profit decline to Rs 14.34 crore, a three-year profit growth of -38.27%, and an ROCE of just 5.19% — all while offering a 3.91% trailing dividend yield at Rs 76.45. The yield exists, but the earnings trajectory behind it raises direct questions about sustainability that income investors cannot afford to overlook.

Key Highlights

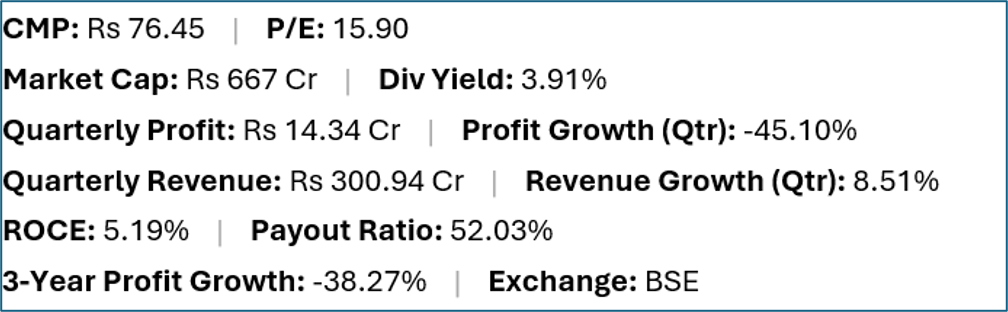

- Kuantum Papers (BSE:KUANTUM) offers a trailing dividend yield of 3.91% at a current market price of Rs 76.45.

- Quarterly net profit stood at Rs 14.34 crore, representing a -45.10% change year-on-year on revenues of Rs 300.94 crore (8.51% change).

- Return on capital employed (ROCE) stands at 5.19%, with a dividend payout ratio of 52.03%.

- Market capitalisation is approximately Rs 667 crore. Three-year profit growth is -38.27%.

Financial Snapshot

Company Overview and Business Model

Kuantum Papers is a Punjab-based integrated paper manufacturer producing writing and printing paper, copier paper and specialty papers. The company operates its own pulp manufacturing using agro-residue (wheat and paddy straw) as its primary fibre source, which differentiates it from wood-based paper mills and gives it feedstock sourced from the local agricultural economy.

The Indian paper industry is a fragmented, capital-intensive sector where margins are closely linked to the price spread between pulp/raw material costs and finished paper realisations. Kuantum Papers competes in the writing and printing paper segment against both organised domestic manufacturers and imports, particularly from ASEAN countries where production costs can be lower.

The company's agro-residue based model is its key operational differentiator, reducing dependence on imported wood pulp, but it introduces seasonal feedstock availability challenges and requires ongoing investment in pulp processing technology.

Financial Review

Revenue of Rs 300.94 crore grew 8.51%, a reasonable top-line showing, but profit of Rs 14.34 crore fell 45.10% — a very sharp contraction. ROCE of 5.19% is the second-lowest on this screen, reflecting both the capital intensity of paper manufacturing and the current margin compression. A three-year profit decline of -38.27% shows this is not a quarterly blip but a sustained earnings deterioration over a meaningful time period. The payout ratio of 52.03% at a declining profit base means the absolute dividend has likely already been reduced, and further cuts are a real possibility.

Dividend Profile and History

The 3.91% trailing yield should be read with significant caution given the three-year profit decline and the 45.10% quarterly profit fall. A payout ratio of 52.03% on declining profits means the absolute dividend in the most recent period is lower than in prior years. If the profit decline trend continues, further dividend reductions are likely. This is a yield that is diminishing in both absolute and sustainability terms.

Future Outlook

Kuantum Papers' outlook depends on a recovery in writing and printing paper realisations (which have been under pressure from import competition and demand softness) and/or a reduction in input costs. The company's wheat straw pulping process is more sustainable and cost-efficient than wood pulp when agro-residue prices are favourable, but the overall paper market dynamics are challenging. A recovery in education sector demand (a key driver of writing paper volumes) and any anti-dumping duty support from the government would help margins.

Investor Insights

- A three-year profit decline of -38.27% combined with a 45.10% quarterly fall is the most bearish earnings profile on this dividend screen — the yield is real but the earnings trend is clearly deteriorating.

- ROCE of 5.19% is barely above the cost of debt for most corporate borrowers, meaning the business is currently earning a return that does not clearly exceed its financing cost.

- The agro-residue pulping model has long-term sustainability credentials, but near-term paper market dynamics are overriding any cost advantage.

- Income investors should wait for at least one quarter of profit recovery before treating the 3.91% yield as indicative of future income potential.

Frequently Asked Questions

Q: What does Kuantum Papers manufacture?

A: Kuantum Papers manufactures writing and printing paper, copier paper and specialty papers at its Punjab plant, using agro-residue (wheat and paddy straw) as its primary pulp feedstock rather than wood-based fibre.

Q: Why has Kuantum Papers' profit declined so sharply?

A: The combination of higher input costs, lower paper realisations due to import competition from ASEAN manufacturers, and demand softness in certain segments has compressed margins significantly over the past three years.

Q: Is Kuantum Papers' dividend at risk?

A: Yes. With a three-year profit decline of -38.27% and a 45.10% quarterly fall, the dividend has already been declining in absolute terms, and further reductions are a realistic scenario if profitability does not recover.

Q: Is Kuantum Papers a buy for income investors?

A: This is general commentary only. Given the sustained earnings deterioration, ROCE below 6%, and the challenged paper market environment, Kuantum Papers requires very careful evaluation before being considered for an income portfolio.

Conclusion

Kuantum Papers is the most challenged income name on this screen: declining profits over three years, a very low ROCE, and a quarterly profit fall of nearly half. The 3.91% trailing yield reflects a historical distribution that the current earnings trajectory does not comfortably support going forward. Income investors should treat this as a watch-and-wait situation, tracking whether the paper market cycle turns and whether management commentary indicates a recovery path, rather than acting on the headline yield.