Mawana Sugars Ltd is one of the smaller income names on this list, but the combination of a 3.95% yield at Rs 101.30, three-year profit growth of 44.32%, and a market capitalisation of Rs 396 crore makes it a name worth examining for investors interested in India's integrated sugar-and-ethanol sector. The quarterly profit dip of 9.55% to Rs 62.83 crore should be read alongside a strong revenue growth of 9.20%, suggesting the core business is growing even if margins fluctuated in the period.

Key Highlights

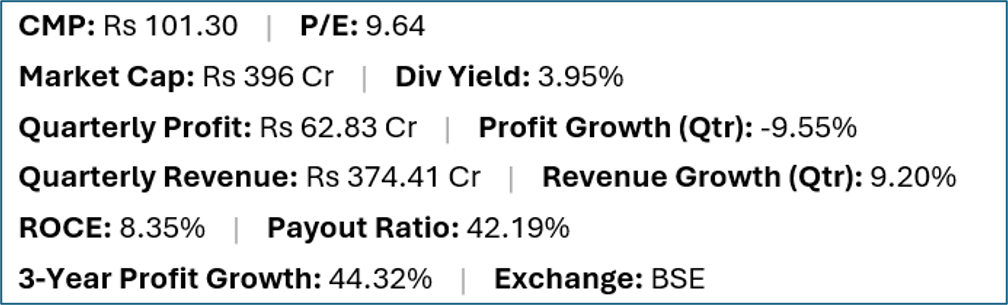

- Mawana Sugars (BSE:MAWANASUG) offers a trailing dividend yield of 3.95% at a current market price of Rs 101.30.

- Quarterly net profit stood at Rs 62.83 crore, representing a -9.55% change year-on-year on revenues of Rs 374.41 crore (9.20% change).

- Return on capital employed (ROCE) stands at 8.35%, with a dividend payout ratio of 42.19%.

- Market capitalisation is approximately Rs 396 crore. Three-year profit growth is 44.32%.

Financial Snapshot

Company Overview and Business Model

Mawana Sugars is an Uttar Pradesh-based integrated sugar company operating cane crushing, sugar manufacturing, power cogeneration (using bagasse as fuel), and ethanol distillation across its mills in the Mawana and Simbhaoli regions of western UP. The integrated model — where sugarcane is processed into sugar, bagasse powers the mills and sells surplus electricity, and molasses is converted to ethanol — reflects the Indian sugar industry's shift toward higher value-added, policy-supported revenue streams.

The ethanol blending programme under the Government of India, which mandates increasing blending of ethanol with petrol and incentivises sugar companies to convert surplus sugar/molasses into fuel ethanol, has become a significant earnings driver for integrated players like Mawana. Ethanol revenues provide a more stable income stream than sugar, since ethanol is purchased by oil marketing companies at government-set prices rather than fluctuating market rates.

Financial Review

Revenue of Rs 374.41 crore grew 9.20%, while quarterly profit of Rs 62.83 crore fell 9.55% — a divergence that likely reflects higher cane costs or a shift in product mix. ROCE of 8.35% is the second-lowest on this list, reflecting the capital intensity of sugar mills and the low-margin nature of the base sugar business. The three-year profit growth of 44.32% is one of the stronger track records in the mid-small cap segment, driven by the ethanol programme's contribution to earnings.

Dividend Profile and History

Mawana Sugars has paid dividends consistently as its earnings recovered, and the 42.19% payout ratio at a quarterly profit of Rs 62.83 crore gives the 3.95% yield reasonable earnings coverage. The cyclical nature of sugar earnings — driven by cane availability, sugar prices and ethanol procurement schedules — means dividends are more variable than in consumer-branded businesses. A three-year profit growth of 44.32% reflects the positive structural impact of ethanol, and continued government support for the blending programme is important for this trajectory.

Future Outlook

The government's ethanol blending programme remains the most important policy variable for Mawana Sugars. As blending targets increase (India has committed to 20% ethanol blending in petrol by 2025–26), demand for ethanol from sugar companies is expected to remain strong. Cane availability and the sugar season's starting inventory position affect both sugar volumes and the raw material available for ethanol production. Mawana's cogeneration capacity provides an additional revenue stream from power sales to the grid, which adds stability to the earnings mix.

Investor Insights

- The ethanol programme is the key structural tailwind for Mawana Sugars — ethanol revenues at government-set prices reduce the earnings volatility inherent in commodity sugar markets.

- ROCE of 8.35% is low, reflecting the capital intensity of sugar mill assets. The profitability of integrated operations improves meaningfully with scale and diversification into ethanol and power.

- Three-year profit growth of 44.32% is one of the stronger compounding records on this list, but investors should verify what proportion was structural (ethanol) versus cyclical (sugar price highs).

- Sugar company dividends are inherently more variable than FMCG or IT dividends — cane costs, weather, and government price policies all affect earnings within a single season.

Frequently Asked Questions

Q: What is the ethanol blending programme and how does it affect Mawana Sugars?

A: India's ethanol blending programme mandates mixing ethanol derived from sugarcane with petrol. Oil marketing companies procure ethanol from sugar companies at government-set prices. For Mawana, this provides a stable, policy-backed revenue stream that reduces dependence on volatile open-market sugar prices.

Q: Why is Mawana Sugars' ROCE so low?

A: ROCE of 8.35% reflects the heavy capital investment required for sugar mills — crushing equipment, boilers, distilleries and cogeneration plant — relative to the margin earned from commodity sugar. Integrated operations with ethanol and power improve the return profile, but the asset intensity remains a structural feature.

Q: Is Mawana Sugars' dividend sustainable?

A: At a 42.19% payout ratio and a growing revenue base, the dividend appears reasonably supported, though sugar companies' earnings are cyclical. Continued government support for ethanol blending is the most important sustainability factor.

Q: Is Mawana Sugars suitable for income investors?

A: This is general commentary only. Mawana offers a real yield backed by a growing business, but sugar sector earnings are cyclical and policy-dependent. Investors should assess their tolerance for earnings volatility alongside the income yield.

Conclusion

Mawana Sugars' 3.95% yield is backed by one of the stronger three-year profit growth records on this screen, largely attributable to the ethanol blending programme's structural contribution to earnings. The capital intensity and ROCE limitations of the sugar mill business are real constraints, and the quarterly profit dip is a variable to monitor. For income investors willing to accept sugar-sector cyclicality in exchange for a growth-backed yield, Mawana Sugars is a credible inclusion on a watchlist.