NMDC Ltd (NSE: NMDC) is India's largest iron ore producer and one of the stronger volume stories on this dividend screen. The quarterly revenue surge of 61.94% to Rs 11,343 crore, accompanied by a 37.19% profit jump to Rs 2,027 crore, makes NMDC one of the more convincingly growing income stories on this list. A 3.90% yield at Rs 84.81 with a P/E of 10.02 and three-year profit growth of 16.81% rounds out a picture that combines income, growth and moderate valuation.

Key Highlights

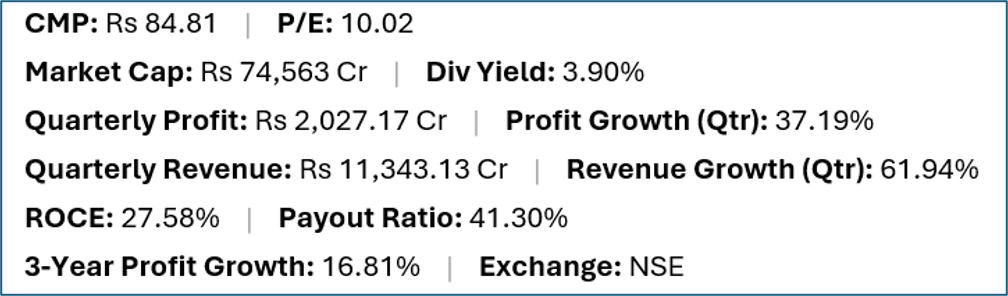

- NMDC (NSE:NMDC) offers a trailing dividend yield of 3.90% at a current market price of Rs 84.81.

- Quarterly net profit stood at Rs 2,027.17 crore, representing a 37.19% change year-on-year on revenues of Rs 11,343.13 crore (61.94% change).

- Return on capital employed (ROCE) stands at 27.58%, with a dividend payout ratio of 41.30%.

- Market capitalisation is approximately Rs 74,563 crore. Three-year profit growth is 16.81%.

Financial Snapshot

Company Overview and Business Model

NMDC is a Navratna PSU under the Ministry of Steel, headquartered in Hyderabad. The company operates iron ore mines in Chhattisgarh and Karnataka, with its two major production centres at Bailadila (Chhattisgarh) and Donimalai (Karnataka). It is the dominant domestic supplier of iron ore to Indian steelmakers, including major integrated steel plants in the country.

Beyond iron ore, NMDC has been developing a greenfield integrated steel plant at Nagarnar, Chhattisgarh — a project that has been years in gestation and has since been transferred to NMDC Steel Limited, a subsidiary, for commissioning. This downstream diversification from mining into steelmaking is a significant strategic shift that alters the company's financial profile and risk character.

NMDC's iron ore is priced at rates it notifies periodically, which are broadly aligned with market prices but can lag international benchmarks. The company's production volume and realisation per tonne are the two primary levers for revenue performance.

Financial Review

Revenue of Rs 11,343.13 crore growing 61.94% reflects both volume recovery and potentially higher iron ore notified prices. Profit of Rs 2,027.17 crore growing 37.19% shows strong operating leverage but with some margin compression — common when revenues grow faster than profits in mining due to cost escalation or royalty payments scaling with realisations. ROCE of 27.58% is healthy for a mining company, reflecting relatively low capital intensity in the extraction phase. The payout ratio of 41.30% at this profit scale gives the 3.90% yield solid earnings coverage.

Dividend Profile and History

NMDC has a consistent track record of dividend payments, supported by its PSU status and government requirement to maintain distributions. The three-year profit growth of 16.81% and the current volume recovery give the dividend a growing earnings base. Unlike names where the yield is shrinking alongside profits, NMDC's income case is supported by earnings momentum in the current quarter.

Future Outlook

NMDC's near-term production trajectory is the key variable. Iron ore volumes from Bailadila and Donimalai have been subject to regulatory clearances, forest diversion approvals and infrastructure constraints, and any improvement in these areas drives revenue growth disproportionately given the high fixed-cost base of mining operations. India's steel sector demand — driven by infrastructure, construction and manufacturing growth — underpins iron ore consumption domestically. The Nagarnar steel plant, once fully operational under NMDC Steel Limited, will add downstream earnings but also capital obligations.

Investor Insights

- The 61.94% revenue growth is the sharpest on this list — investors should verify whether this is a volume surge, a price increase, or both, since the sustainability of the jump depends on the driver.

- NMDC's P/E of 10.02 with three-year profit growth of 16.81% appears attractively valued relative to its growth record, suggesting the market has not fully re-rated the stock for the volume recovery.

- The government's steel sector ambitions (targeting 300 million tonnes of annual production capacity by 2030) are a structural tailwind for NMDC as the primary domestic iron ore supplier.

- Demerger or strategic decisions around the Nagarnar steel plant subsidiary will affect NMDC's consolidated financials and capital allocation, and are worth tracking in investor communications.

Frequently Asked Questions

Q: What does NMDC produce?

A: NMDC is India's largest iron ore producer, mining ore from its deposits in Chhattisgarh and Karnataka. It also has a downstream steel plant under NMDC Steel Limited at Nagarnar, Chhattisgarh.

Q: Why did NMDC's revenue jump 61.94%?

A: The surge reflects a combination of higher iron ore production volumes and potentially improved ore notified prices during the quarter. Investors should verify the volume vs. price mix in NMDC's quarterly investor disclosures.

Q: Is NMDC's dividend growing?

A: With three-year profit growth of 16.81% and a strong current-quarter performance, the dividend appears to have growing earnings support. PSU ownership also provides a structural incentive to maintain and grow distributions.

Q: Is NMDC suitable for income investors?

A: This is general commentary only. NMDC offers an income yield with volume-driven earnings momentum, and a reasonable P/E. Investors should track iron ore volume data and regulatory clearance updates as the primary earnings drivers.

Conclusion

NMDC combines a 3.90% yield with some of the most convincing earnings momentum on this screen — 61.94% revenue growth and 37.19% profit growth in the latest quarter, against a three-year growth track of 16.81%. The valuation at P/E 10.02 suggests the market has not fully priced in the current volume recovery. For income investors looking for a dividend yield backed by earnings growth, NMDC is among the more balanced options on this list.