Oil and Natural Gas Corporation Ltd (NSE: ONGC) posted a 47.80% year-on-year surge in quarterly net profit to Rs 13,677.87 crore, making it the largest absolute profit generator on this dividend screen. At a CMP of Rs 234.30 with a P/E of just 7.04 and a trailing yield of 5.21%, ONGC occupies the intersection of value and income that PSU energy investors have historically found attractive — when commodity cycles cooperate.

Key Highlights

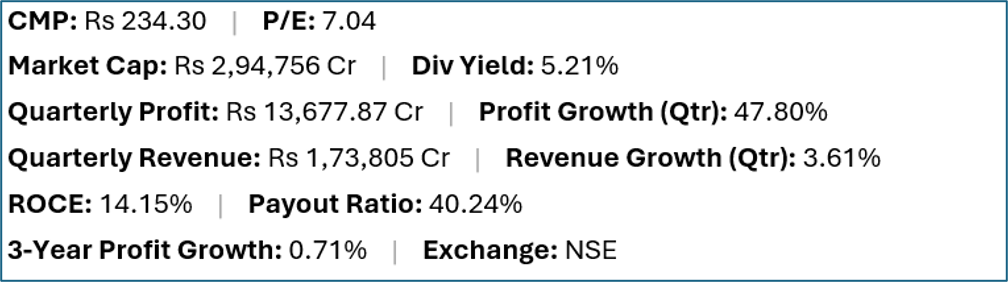

- ONGC (NSE:ONGC) offers a trailing dividend yield of 5.21% at a current market price of Rs 234.30.

- Quarterly net profit stood at Rs 13,677.87 crore, representing a 47.80% change year-on-year on revenues of Rs 1,73,805 crore (3.61% change).

- Return on capital employed (ROCE) stands at 14.15%, with a dividend payout ratio of 40.24%.

- Market capitalisation is approximately Rs 2,94,756 crore. Three-year profit growth is 0.71%.

Financial Snapshot

Company Overview and Business Model

ONGC is India's largest upstream oil and gas company and one of the largest energy companies in Asia. Its core business is the exploration, development and production of crude oil and natural gas from domestic fields, principally in the Mumbai High offshore basin, which remains its most significant producing asset despite declining reservoir pressures after decades of production, and onshore blocks across Assam, Gujarat, Andhra Pradesh and Rajasthan.

Beyond domestic upstream, ONGC has substantial international operations through its wholly owned subsidiary ONGC Videsh Ltd (OVL), which holds equity stakes in oil and gas assets across 17 countries including Russia, Vietnam, Brazil, Mozambique and Azerbaijan. ONGC also holds controlling stakes in downstream entities including HPCL and Mangalore Refinery and Petrochemicals Ltd (MRPL), making it a vertically integrated energy conglomerate with upstream, midstream and downstream exposure.

ONGC's financial performance is tied more closely to global crude oil prices than to domestic demand, since its revenues come primarily from selling crude at market-linked prices to refineries. Subsidiary contributions from HPCL and MRPL add downstream earnings but also introduce marketing-margin volatility.

Financial Review

Quarterly profit of Rs 13,677.87 crore growing 47.80% on revenues of Rs 1,73,805 crore (up only 3.61%) indicates that the profit jump was driven by margins — either crude realisation improvement, cost reduction, or favourable OVL contribution — rather than volume growth. ROCE of 14.15% is moderate for an upstream business, reflecting the capital intensity of exploration and production assets. The payout ratio of 40.24% leaves meaningful retained earnings while still generating a 5.21% yield on the current CMP.

Dividend Profile and History

ONGC has a long track record as one of India's largest absolute dividend payers, with distributions supported by its scale of upstream earnings. The government's majority ownership creates a structural incentive to maintain payouts. The 40.24% payout ratio is conservative relative to peers like Coal India (53%), giving ONGC more financial flexibility to sustain dividends if crude prices soften. The flat three-year profit trend (0.71%) shows that earnings, while large in absolute terms, have not grown meaningfully over the medium term.

Future Outlook

ONGC's near-term production trajectory is a key focus: Mumbai High oil production has been in a long structural decline, and the company's brownfield rejuvenation programmes and new enhanced oil recovery projects will determine whether this trend is arrested. OVL's international portfolio provides some production diversification but also introduces geopolitical risk, particularly around its Russian assets post-2022. LNG import investments and the push toward domestic gas production are areas where ONGC has strategic ambitions but returns remain long-dated.

Investor Insights

- The 47.80% profit jump on only 3.61% revenue growth warrants close examination — investors should identify whether the driver was crude price realisation, OVL income, or one-time items before assuming this run rate is sustainable.

- A P/E of 7.04 with 5.21% yield is attractive on income metrics, but the flat three-year profit growth suggests the market is pricing in continued earnings stagnation rather than a sustained re-rating.

- OVL's Russian assets are a potential liability under evolving sanctions and repatriation dynamics — an often-underweighted risk in ONGC valuations.

- ONGC's downstream subsidiary HPCL adds earnings diversification but also introduces downstream margin volatility that is not always transparent in ONGC's consolidated numbers.

Frequently Asked Questions

Q: How does ONGC make money?

A: ONGC's primary income is from selling crude oil and natural gas produced from its domestic exploration blocks and international assets (via OVL) at market-linked prices to refineries. It also earns dividends and income from its stakes in HPCL and MRPL.

Q: Is ONGC's dividend yield sustainable?

A: With quarterly profit of Rs 13,678 crore and a 40.24% payout ratio, the dividend appears well-covered in the current environment. Sustainability depends on crude oil prices remaining at levels that support upstream margins.

Q: What is ONGC Videsh?

A: ONGC Videsh Ltd (OVL) is ONGC's wholly owned subsidiary for international oil and gas exploration and production. It holds stakes in assets across 17 countries, providing ONGC with production and earnings diversification beyond Indian domestic blocks.

Q: Why is ONGC's P/E so low?

A: At 7.04x, ONGC's P/E reflects market scepticism about earnings growth given Mumbai High's declining production trajectory, crude price cyclicality, and the government's role in pricing and dividend decisions. It is a value stock, not a growth stock, in market perception.

Conclusion

ONGC's scale of earnings — Rs 13,678 crore of quarterly profit — gives its 5.21% yield one of the strongest absolute earnings bases on this list. The challenge is that those earnings have been essentially flat for three years, and the structural decline of Mumbai High production is a long-running concern. For income investors, ONGC is a legitimate choice in periods of favourable crude pricing, but the investment case requires a clear view on crude oil's near-term trajectory and a realistic assessment of the company's domestic production outlook.