Quess Corp Ltd (NSE: QUESS) is India's largest workforce management and business services company, with quarterly revenues of Rs 3,892.45 crore and a 3.65% trailing dividend yield at Rs 276.75. The company's 74.12% payout ratio at modest quarterly profit growth of 5.02% makes the yield income-visible, but the gap between revenue scale and net profit margin is the central feature that investors must understand when assessing Quess as an income stock.

Key Highlights

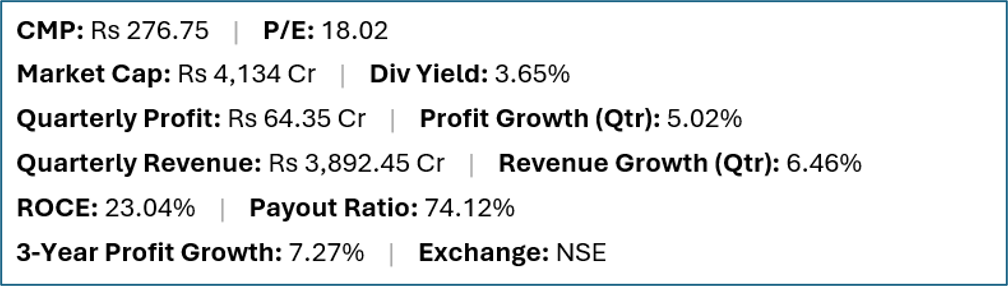

- Quess Corp (NSE:QUESS) offers a trailing dividend yield of 3.65% at a current market price of Rs 276.75.

- Quarterly net profit stood at Rs 64.35 crore, representing a 5.02% change year-on-year on revenues of Rs 3,892.45 crore (6.46% change).

- Return on capital employed (ROCE) stands at 23.04%, with a dividend payout ratio of 74.12%.

- Market capitalisation is approximately Rs 4,134 crore. Three-year profit growth is 7.27%.

Financial Snapshot

Company Overview and Business Model

Quess Corp operates across three broad business pillars: workforce management (staffing and flexible workforce solutions for enterprises across sectors), operating asset management (facility management, food services and technology-enabled business process services), and global technology solutions (IT staffing and managed services). The company manages one of India's largest associate headcounts — close to 500,000 associates at peak periods — across its staffing and facility management businesses.

Staffing businesses are inherently low-margin: they bill clients for associates' time and skills, passing through salary costs while earning a spread. The economics are volume-dependent, and operating leverage means that as headcount rises, the fixed cost base is spread over more billing relationships. Quess has been working to improve its margin profile through a shift toward higher-value managed services and technology-enabled offerings.

Financial Review

Revenue of Rs 3,892.45 crore growing 6.46% is solid for a large-base staffing business, but the net profit of Rs 64.35 crore growing only 5.02% reveals the thin margins inherent in workforce management. The gap between Rs 3,892 crore of revenue and Rs 64 crore of profit implies a net margin of approximately 1.65% — typical for staffing companies globally but a useful number for income investors to understand. ROCE of 23.04% is respectable given the working-capital-intensive nature of staffing. The 74.12% payout ratio means the company is distributing a high proportion of its modest absolute profits.

Dividend Profile and History

The 3.65% yield is supported by the 74.12% payout ratio at current profit levels, but the thin margins mean the income stream is sensitive to any disruption in the staffing business — a large client loss, wage inflation, or a market slowdown can compress net profit quickly given the pass-through cost structure. Three-year profit growth of 7.27% is modest but positive, consistent with the steady-state nature of large staffing businesses.

Future Outlook

Quess Corp's growth outlook is tied to India's formalisation of employment — as companies move from informal to formal employment arrangements, the addressable market for organised staffing grows. The company has been pruning loss-making or low-margin businesses and focusing on higher-quality revenue. Technology-enabled managed services, which carry better margins than basic staffing, are a key medium-term revenue mix improvement target. The global IT staffing segment provides international diversification.

Investor Insights

- Quess earns Rs 64 crore of net profit on Rs 3,892 crore of revenue — investors should understand that a 1.65% net margin means even small revenue disruptions translate to material profit swings.

- The 74.12% payout ratio is high relative to the thin margins — the company is distributing most of its modest earnings, leaving limited retained capital to absorb business setbacks.

- India's employment formalisation trend is a genuine structural tailwind for organised staffing — Quess benefits as enterprises shift from informal to formal workforce management.

- At P/E 18.02 on 5% profit growth, the valuation is not obviously cheap — it reflects the market pricing in business quality and the structural staffing opportunity rather than current earnings momentum.

Frequently Asked Questions

Q: What does Quess Corp do?

A: Quess Corp is India's largest workforce management and business services company, providing staffing, facility management, food services, IT staffing and technology-enabled business process services to enterprises across India and internationally.

Q: Why is Quess Corp's net profit so small relative to revenue?

A: Staffing businesses are inherently thin-margin: they bill clients for associates' time and costs while earning a spread. Quess's Rs 64 crore profit on Rs 3,892 crore revenue reflects a net margin of approximately 1.65%, typical for large staffing companies globally.

Q: Is Quess Corp's 3.65% yield sustainable?

A: At 74.12% payout, the yield is dependent on the current profit level being maintained. Revenue growth of 6.46% with 5.02% profit growth suggests the business is stable, supporting near-term yield sustainability, though the thin margins make the income stream relatively sensitive to disruptions.

Q: Is Quess Corp suitable for income investors?

A: This is general commentary only. The yield is real and the business is large and established, but the thin-margin staffing model means income investors should understand what drives profitability before relying on the yield.

Conclusion

Quess Corp's 3.65% yield reflects the income credentials of India's largest workforce management business, but the thin margins inherent in staffing are the defining characteristic that income investors must understand. The company is distributing 74.12% of its modest profits as dividends, which makes the yield visible but also fragile to margin compression. The structural tailwind of employment formalisation in India is real, and Quess has the scale to benefit — but income investors should treat this as a steady-state yield rather than a growing one unless the company's margin improvement strategy demonstrably takes hold.