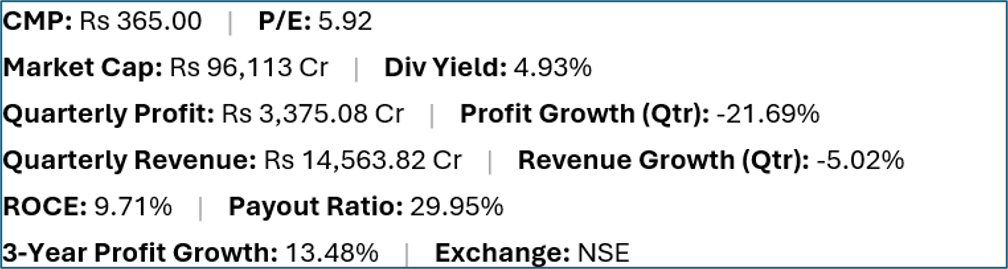

REC Ltd (NSE: RECLTD), formerly Rural Electrification Corporation, is one of India's largest government-backed non-banking financial companies focused on financing the power sector. With a market capitalisation of Rs 96,113 crore and a 4.93% trailing yield at Rs 365, it sits among the larger income names on this list. However, the quarterly profit decline of 21.69% to Rs 3,375 crore and a 5.02% revenue contraction are metrics that warrant careful scrutiny before the yield becomes the headline.

Key Highlights

- REC Ltd (NSE:RECLTD) offers a trailing dividend yield of 4.93% at a current market price of Rs 365.00.

- Quarterly net profit stood at Rs 3,375.08 crore, representing a -21.69% change year-on-year on revenues of Rs 14,563.82 crore (-5.02% change).

- Return on capital employed (ROCE) stands at 9.71%, with a dividend payout ratio of 29.95%.

- Market capitalisation is approximately Rs 96,113 crore. Three-year profit growth is 13.48%.

Financial Snapshot

Company Overview and Business Model

REC Ltd provides long-term loans to state electricity boards, power generation companies, transmission and distribution utilities, and renewable energy developers across India. The company is effectively a conduit between capital markets (where it raises bonds and loans) and the power sector (where it deploys funds as project finance). It is classified as an infrastructure finance company and carries the government's implicit backing as a Navratna PSU under the Ministry of Power.

REC's lending book spans thermal, hydro, nuclear and renewable power generation as well as transmission and distribution infrastructure — a portfolio that reflects the breadth of India's power sector investment needs. In recent years, the company has also expanded into non-power infrastructure financing and international lending, diversifying beyond its traditional electricity-sector remit.

Because REC is a lender rather than an operator, its financial performance is primarily a function of net interest margin (the spread between borrowing and lending rates), loan growth, and asset quality (the level of non-performing assets in its portfolio).

Financial Review

Revenue fell 5.02% and net profit contracted 21.69% to Rs 3,375.08 crore — the sharpest absolute profit decline among the financial names on this list. ROCE of 9.71% is consistent with a financial intermediary where leverage amplifies returns but also means capital employed is large relative to equity. The payout ratio of 29.95% is conservative, which gives the dividend more earnings coverage than most names on this screen. Three-year profit growth of 13.48% shows the business has grown over the medium term, making the current quarter's decline a notable deviation from trend.

Dividend Profile and History

The 4.93% yield at a 29.95% payout ratio means REC is distributing less than a third of its profits as dividends — a conservative approach that provides a substantial earnings buffer and makes the yield more durable than peers with higher payout ratios. Even with a 21.69% quarterly profit decline, the absolute profit of Rs 3,375 crore comfortably covers the dividend at this payout level. Government ownership reinforces the dividend commitment.

Future Outlook

REC Ltd's loan book is growing as India's power sector investment accelerates, but the net interest margin is under pressure from higher borrowing costs and competition for renewable energy lending. Asset quality in the state utility segment has historically been a concern — many state electricity boards carry significant financial stress — and any deterioration in borrower repayment capacity would affect REC's provisions and profit. The company's expansion into renewables is strategically sound given the energy transition, but lower-risk renewable lending may also carry narrower spreads than traditional thermal project finance.

Investor Insights

- A 21.69% quarterly profit decline in a financial intermediary can reflect higher provisions, margin compression, or one-time items — the specific cause matters significantly for assessing forward earnings.

- The 29.95% payout ratio provides a meaningful earnings buffer; the dividend is not at immediate risk despite the profit decline.

- REC trades at P/E 5.92, a low multiple that the market applies to power-sector NBFCs due to asset quality risk and government policy dependency.

- State electricity board loan exposures carry implicit sovereign credit risk; any large-scale restructuring of SEBs would affect REC's book — a tail risk worth understanding before investing.

Frequently Asked Questions

Q: What does REC Ltd do?

A: REC Ltd is a government-backed NBFC that provides long-term project finance to the power sector — including generation, transmission, distribution and renewable energy projects — and increasingly to broader infrastructure.

Q: Why did REC's profit fall 21.69%?

A: Profit declined on both a revenue contraction (-5.02%) and likely higher provisions or NIM compression. Investors should read the quarterly investor presentation and earnings call transcript for the specific breakdown of the decline.

Q: Is REC Ltd's dividend safe despite the profit fall?

A: At a 29.95% payout ratio, the dividend has substantial earnings coverage. Even at a lower quarterly profit run rate, the annual dividend appears funded. However, a sustained earnings decline would eventually reduce absolute dividend payments.

Q: What is the main risk in REC Ltd?

A: Asset quality in its state electricity board and power project loan portfolio is the primary credit risk. Interest rate risk (borrowing costs rising faster than lending rates) and regulatory changes to NBFC capital requirements are secondary risks.

Conclusion

REC Ltd's 4.93% yield is among the more conservatively covered on this list — a 29.95% payout ratio means the dividend is not dependent on a high earnings distribution. The concern is the direction of profitability: a 21.69% quarterly profit decline needs to be traced to its cause before investors can assess whether this is a temporary blip or an emerging trend. For income investors who understand power-sector NBFC risk, REC's conservative payout and government backing give the yield reasonable structural support.