Infrastructure investment trusts have carved out a distinct place in the Indian income-investing landscape, and Shrem InvIT sits at the top of the dividend-yield table among BSE and NSE-listed instruments, offering a trailing yield of 13.44% at a current unit price of Rs 101.80. For investors focused on predictable income from real assets, that headline figure naturally commands attention — though the structure of an InvIT and the risks that accompany it are quite different from an equity dividend.

Key Highlights

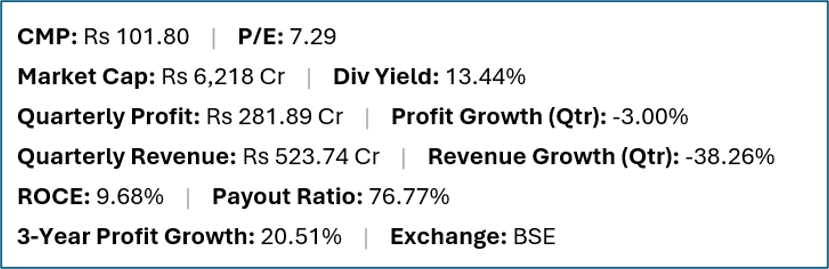

- Shrem InvIT (BSE:SHREM) offers a trailing dividend yield of 13.44% at a current market price of Rs 101.80.

- Quarterly net profit stood at Rs 281.89 crore, representing a -3.00% change year-on-year on revenues of Rs 523.74 crore (-38.26% change).

- Return on capital employed (ROCE) stands at 9.68%, with a dividend payout ratio of 76.77%.

- Market capitalisation is approximately Rs 6,218 crore. Three-year profit growth is 20.51%.

Financial Snapshot

Company Overview and Business Model

Shrem InvIT is a registered infrastructure investment trust in India that holds road assets as its underlying investments. The InvIT structure is designed specifically to pool infrastructure assets and distribute the cash flows generated from those assets — typically toll collections or annuity payments from the National Highways Authority of India (NHAI) — to unitholders. Unlike an operating company, Shrem InvIT's distributions are not purely a function of equity profits; they are linked to the cash generated by the underlying concession agreements governing its road assets.

The trust holds a portfolio of build-operate-transfer (BOT) or hybrid annuity model (HAM) road projects, where cash inflows are contractually defined and largely predictable over the concession period. This gives the income stream a different risk character than cyclical business earnings — but also means that distributions are tied to the longevity and performance of specific concession agreements rather than to organic business growth.

Shrem InvIT's market capitalisation of Rs 6,218 crore positions it as a mid-sized infrastructure trust by Indian standards. Its units are listed and tradeable on the exchange, giving retail investors access to infrastructure cash flows that were historically the preserve of institutional capital.

Financial Review

The trust reported quarterly net income of Rs 281.89 crore, a modest decline of 3.00% year-on-year, alongside a sharper 38.26% fall in quarterly revenues to Rs 523.74 crore. The revenue contraction likely reflects the timing of distribution payments or changes in underlying asset reporting rather than a structural deterioration in cash flows, but this warrants verification against official SEBI disclosures. ROCE of 9.68% is lower than the equity names on this screen, consistent with the capital-intensive nature of infrastructure assets. A payout ratio of 76.77% reflects the trust's mandate to distribute the majority of distributable cash flows to unitholders, which is both a feature and an obligation under InvIT regulations.

Dividend Profile and History

The 13.44% trailing dividend yield is the highest on this list and reflects both the pass-through income mandate of the InvIT structure and the current unit price. InvITs in India are required under SEBI regulations to distribute at least 90% of their net distributable cash flows to investors. That regulatory floor gives distributions more structural support than a discretionary corporate dividend, but it also means there is limited retained cash to buffer against asset-level disruptions. Distributions may be structured as a combination of interest, dividend and return of capital, with different tax treatment for each component — an important consideration for unitholders assessing the after-tax yield.

Future Outlook

The outlook for Shrem InvIT is tied to the performance and remaining concession life of its underlying road assets. India's infrastructure investment pipeline remains robust, and the government's continued focus on national highway development supports the broader sector. However, toll-based assets carry traffic-volume risk, while HAM assets are exposed to counterparty risk from NHAI annuity payments. Any refinancing of underlying project debt at higher rates, or an acquisition of new assets at elevated valuations, could affect distribution levels. Investors should track the trust's quarterly distribution announcements, project-level traffic and revenue reports, and any SEBI filings relating to asset acquisitions or changes to the portfolio.

Investor Insights

- InvIT distributions are not the same as corporate dividends: they may include return of capital, which reduces the cost base of units held rather than representing pure income, with distinct tax implications.

- The 38.26% quarterly revenue decline should be examined against official unitholder reports before drawing conclusions — InvIT revenue recognition can be lumpy across reporting periods.

- At a P/E of 7.29 and yield of 13.44%, the unit appears attractively priced on an income basis, but the sustainability of distributions depends on concession-level cash flows, not headline earnings.

- Infrastructure trusts are relatively illiquid compared to large-cap equities; bid-ask spreads and trading volumes should be checked before establishing a meaningful position.

Frequently Asked Questions

Q: What is Shrem InvIT and how does it generate income?

A: Shrem InvIT is a SEBI-registered infrastructure investment trust that holds road concession assets. Its income comes from toll collections or NHAI annuity payments under the terms of its underlying concession agreements, which it is required to largely distribute to unitholders.

Q: Why is Shrem InvIT's dividend yield so high?

A: The combination of a regulatory requirement to distribute at least 90% of net distributable cash flows, the pass-through income structure of InvITs, and the current unit price produces a trailing yield of 13.44%. This reflects the structure of the instrument rather than extraordinary business profitability.

Q: Is Shrem InvIT suitable for retail investors?

A: Retail investors can buy InvIT units on the exchange, but should understand that distributions may include return of capital (not just income), liquidity is lower than equities, and the risk profile is tied to specific infrastructure concessions. Consulting a SEBI-registered adviser before investing is advisable.

Q: What drives the risk in Shrem InvIT's distributions?

A: Key risks include traffic volume variability on toll roads, NHAI payment timeliness on HAM projects, refinancing risk on project-level debt, and the finite life of concession agreements. A reduction in any of these inputs can reduce distributable cash flows.

Conclusion

Shrem InvIT's 13.44% yield makes it the standout income instrument on this list, but it demands a different analytical lens than an equity dividend. The underlying road assets provide contractual cash flows with a different risk character than corporate earnings, but distributions are not unconditional — they are linked to concession-level performance, traffic trends, and the trust's debt structure. Income-focused investors should read the SEBI-mandated unitholder reports carefully before treating the headline yield as a durable annual income commitment.