Shares of Asarfi Hospital Limited (BOM:543943) witnessed heavy selling pressure and hit lower circuit after a sharp rally in recent weeks. The stock declined nearly 20% in the latest session and slipped below its 51-day EMA near ₹201, indicating near-term weakness after an extended upmove.

Despite the recent correction, the company reported strong FY26 financial performance driven by higher patient volumes, expansion in specialty healthcare services, and improving oncology operations.

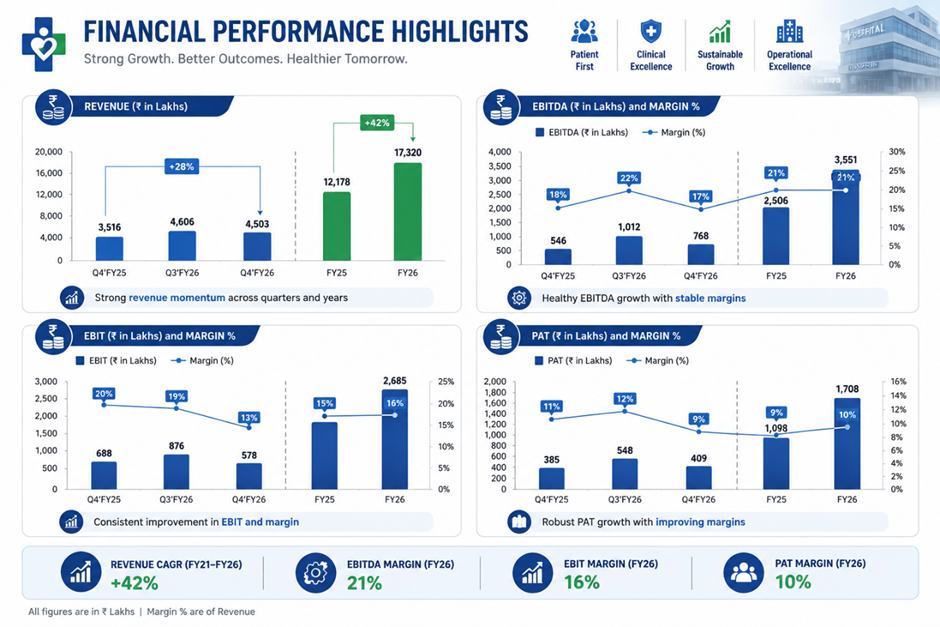

Data Source: Company Filing; Image source: © 2026 Krish Capital Pty. Ltd., Analysis: Kalkine Group

Strong FY26 Revenue and Profit Growth

Asarfi Hospital reported consolidated FY26 revenue of ₹173.5 crore, reflecting 42% YoY growth compared to ₹121.8 crore in FY25. EBITDA increased 42% YoY to ₹35.3 crore, while PAT rose 58% YoY to ₹16.7 crore.

FY26 EBITDA margin remained stable at 20%, while PAT margin improved to 10% from 9% in FY25.

During Q4FY26, revenue increased 29% YoY to ₹45.2 crore, while PAT rose 9% YoY to ₹3.9 crore. However, quarterly margins moderated due to higher operating expenses and lower occupancy in the super-specialty unit following bed expansion.

Oncology and Super-Specialty Expansion Driving Growth

The company continues strengthening its healthcare infrastructure across Eastern India through expansion in super-specialty and cancer care services.

Asarfi Hospital currently operates:

- 285-bed super-specialty hospital

- 65-bed cancer hospital

- 110+ doctors

- 1,100+ nursing and support staff

Management highlighted that FY26 ARPOB (Average Revenue Per Occupied Bed) in the super-specialty unit increased to ₹23,020 compared to ₹17,505 in FY25, supported by better case mix and higher ICU utilization. Cancer hospital ARPOB also improved to ₹37,428 during FY26.

The company plans to:

- Expand super-specialty bed capacity from 285 to 350

- Increase cancer hospital capacity from 65 to 150 beds by FY27

- Establish a Bone Marrow Transplant unit

- Launch Jharkhand’s first multi-organ transplant facility in partnership with Gleneagles Hospital

Regional Healthcare Expansion Opportunity

Management stated that Eastern India continues to offer strong healthcare growth potential due to:

- Low organized healthcare penetration

- Limited oncology infrastructure

- Growing health insurance adoption

- Rising demand for advanced medical services

The company remains one of only three dedicated cancer hospitals in Jharkhand, providing a strategic regional advantage.

Technical Summary

The stock witnessed a sharp correction after recently touching fresh highs near ₹250. Price action indicates profit booking following a steep rally over the last few months. Immediate support is visible around ₹190–200, while resistance remains near ₹225–250. Sustaining above the ₹190 zone may help stabilize sentiment, whereas a decisive breakdown could lead to additional near-term volatility.

Chart by TradingView

Conclusion

Asarfi Hospital delivered strong FY26 growth supported by higher patient volumes, oncology expansion, and improving healthcare infrastructure. The company’s aggressive capacity expansion plans and specialty healthcare focus continue to support its long-term growth strategy.

However, after the recent sharp rally, the stock has entered a corrective phase amid profit booking and near-term technical weakness.

FAQs

- Why did Asarfi Hospital stock fall sharply?

The stock witnessed heavy profit booking after a strong rally and corrected nearly 20% in the latest trading session.

- What was Asarfi Hospital’s FY26 revenue growth?

The company reported 42% YoY revenue growth with FY26 consolidated revenue reaching ₹173.5 crore.

- What are Asarfi Hospital’s expansion plans?

The company plans to expand cancer hospital capacity, establish a bone marrow transplant unit, and develop Jharkhand’s first multi-organ transplant center.