Britannia Industries Limited (NSE:BRITANNIA) reported steady revenue and profit growth for Q4FY26 and FY26, supported by resilient domestic demand, strong traction in adjacency businesses, and continued investments in premiumization and e-commerce. However, the company faced pressure from geopolitical disruptions, higher logistics costs, and softer profitability momentum, which weighed on investor sentiment.

Following the earnings announcement, Britannia shares declined more than 5% intraday to around ₹5,517. The stock also slipped below its 50-day moving average near ₹5,754, reflecting cautious market sentiment despite stable long-term fundamentals.

Q4 FY26 Financial Performance

Britannia reported consolidated net sales of ₹4,686 crore in Q4FY26, registering 7.1% year-on-year growth. Operating profit stood at ₹768 crore, up 6% YoY, while profit before tax increased 4.4% to ₹785 crore. Profit after tax attributable to owners rose strongly by 21.1% to ₹678 crore during the quarter.

Profit after tax margin improved to 14.5% of revenue in Q4FY26 compared to 13.9% in Q3FY26, indicating sequential improvement in profitability despite operational challenges.

The company stated that its international business revenues and profitability were impacted during the quarter due to vessel unavailability, rising ocean freight rates, and higher fuel costs linked to the West Asia conflict. However, Britannia confirmed there was no major disruption to manufacturing operations in India.

Commodity trends remained mixed during the quarter. Cocoa prices declined 16% YoY and flour prices softened 6%, while milk prices increased 17% YoY, creating pressure on input costs across certain product categories.

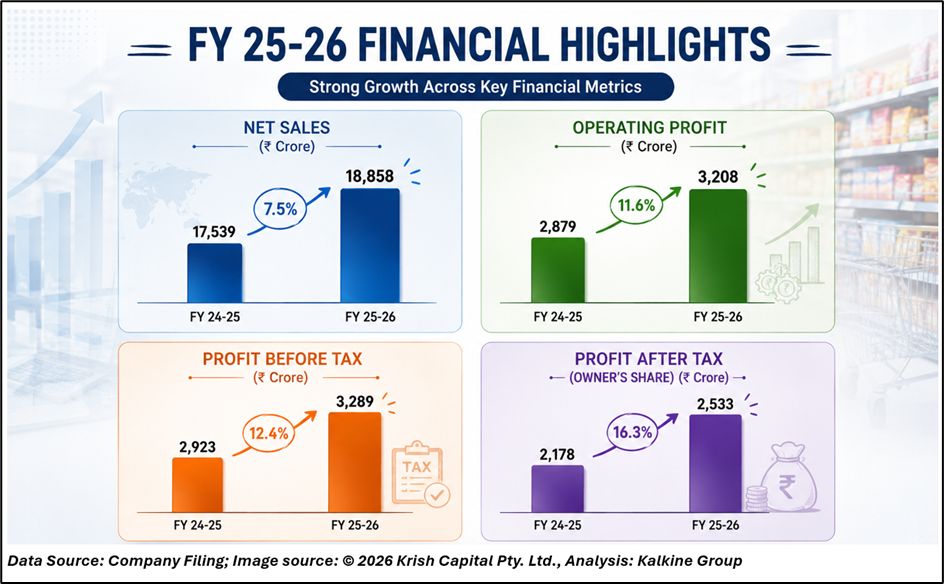

FY26 Financial Performance

For the full FY26 period, Britannia posted consolidated net sales of ₹18,858 crore, reflecting 7.5% year-on-year growth. Operating profit increased 11.6% to ₹3,208 crore, while profit before tax rose 12.4% to ₹3,289 crore. Profit after tax attributable to owners grew 16.3% YoY to ₹2,533 crore.

Operating margin improved to 17% during FY26 compared to 16.4% in FY25, reflecting disciplined cost management and better product mix. Profit after tax margin also improved to 13.4% from 12.4% in the previous financial year.

Britannia maintained healthy growth momentum across multiple categories, with wafers, dairy, cakes, rusks, and premium offerings contributing positively to overall performance.

Strategy and Outlook

Britannia continued to focus on five major strategic priorities, including strengthening sales and supply-chain efficiencies, expanding premium product offerings, accelerating innovation, enhancing regional localization strategies, and improving sustainability initiatives.

The company highlighted strong growth in e-commerce, where channel salience in the domestic business increased to 6% in FY26 from 2% in FY22. Adjacency categories also continued outperforming the core biscuits business.

Britannia stated that products such as 50-50 Cheeze Dipped and Caramel Dipped gained strong market traction, becoming the second-largest player in the sandwich cracker category within three months of launch.

Management also emphasized aggressive cost optimization initiatives, including packaging re-engineering, logistics efficiency, renewable energy adoption, and alternate fuel sourcing to mitigate supply disruptions and protect margins.

Looking ahead, the company plans calibrated price hikes from Q1FY27 to offset inflationary pressures and geopolitical disruptions affecting freight and fuel costs. Britannia expects continued momentum from premium products, regional strategies, and adjacency businesses to support long-term growth.

Technical Summary

Britannia shares corrected sharply after earnings and slipped below the 50-day SMA near ₹5,754, indicating short-term weakness. The stock is currently testing support around ₹5,500. Sustained weakness below this level may trigger further downside toward ₹5,350, while resistance is placed near ₹5,800–₹5,900 amid elevated selling pressure and volatility.

Chart by TradingView

Conclusion

Britannia delivered stable FY26 revenue and profit growth despite geopolitical disruptions and cost pressures. Strong execution across premium products, adjacency categories, and e-commerce continues to support long-term growth prospects. However, rising logistics expenses and softer market sentiment may keep the stock under pressure in the near term until margin visibility improves.

FAQs

- Why did Britannia shares fall after Q4FY26 results?

Britannia shares declined due to geopolitical cost pressures, weaker sentiment, and concerns over rising freight and fuel-related expenses. - How did Britannia perform in FY26?

Britannia reported 7.5% revenue growth and 16.3% profit growth during FY26, supported by operational efficiencies and premiumization strategies. - What are Britannia’s growth drivers for FY27?

Premium products, e-commerce expansion, adjacency businesses, regional strategies, and calibrated price increases are expected to support future growth.