Dabur India Limited (NSE:DABUR) delivered a resilient operational performance in Q4FY26, supported by healthy domestic volume growth, strong momentum in home and personal care products, and continued market share gains across core categories despite macroeconomic and weather-related challenges.

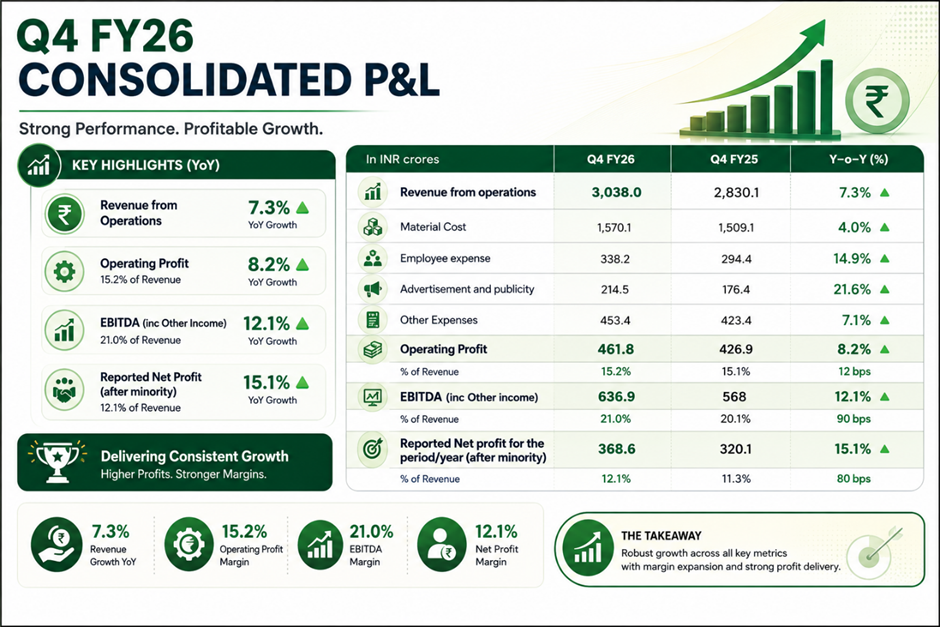

The FMCG major reported consolidated revenue from operations of ₹3,038 crore for the quarter ended March 31, 2026, reflecting a 7.3% year-on-year increase. Consolidated profit after tax rose 15.1% YoY to ₹368.6 crore, while operating profit increased 8.2% to ₹461.8 crore during the quarter.

Investor sentiment remained moderately positive following the earnings announcement, with Dabur shares witnessing buying interest as investors welcomed improving profitability, margin expansion, and sustained volume-led growth amid a still-volatile consumption environment.

Data Source: Company Filing

The company reported 6% India FMCG volume growth during Q4FY26, indicating steady recovery in consumer demand and strong execution across urban and rural markets. Consolidated operating margins expanded by 12 basis points year-on-year, while PAT margins improved by 82 basis points, highlighting better operating leverage and cost management.

Dabur’s domestic Home & Personal Care (HPC) business emerged as the strongest growth contributor, registering 16.8% YoY growth during the quarter. The hair care portfolio delivered growth in the twenties, driven by Dabur Amla, Dabur Almond, and coconut oil brands. Shampoo sales also witnessed strong double-digit expansion alongside market share gains.

Oral care continued to outperform category growth, supported by brands such as Dabur Red, Meswak, and Dabur Herb’l. Meanwhile, home care brands including Odonil, Sanifresh, and Odomos recorded robust double-digit growth driven by premium product launches and stronger consumer demand.

Within healthcare, Dabur Honey, Hajmola, Honitus, and health juice portfolios sustained strong momentum. The company noted that Dabur Honey registered double-digit growth in the twenties, while Hajmola and Honitus continued gaining market share through focused advertising and differentiated positioning.

The Foods & Beverages segment delivered relatively moderate performance with low single-digit growth, although the company highlighted strong traction in the Real Activ juices and coconut water portfolio. Culinary products and the Badshah spices business also posted healthy double-digit growth during the quarter.

International operations grew 2.5% YoY in reported terms, with strong performances from markets such as Bangladesh, Turkey, Nigeria, and the UK. However, Dabur indicated that geopolitical disturbances impacted the Middle East business, while unseasonal rains in March affected summer-focused categories, including beverages and glucose products.

Strategically, Dabur continued strengthening its brand visibility through celebrity-driven campaigns, influencer-led marketing initiatives, and digital engagement strategies. The company also highlighted improving ESG credentials, with its DJSI sustainability score rising to 83 in FY2024-25 from 81 in the previous year.

The board recommended a final dividend of ₹5.50 per share, taking total FY26 dividend payout to ₹8.25 per share.

Technical Summary

Dabur India shares closed near ₹470, trading above the 50-day SMA around ₹456, indicating improving short-term momentum after recent recovery from lower levels. RSI near 61 suggests strengthening bullish sentiment. Immediate support is seen around ₹450–445, while resistance is positioned near ₹485 and ₹520 levels.

Chart by TradingView

Conclusion

Dabur India delivered a strong Q4FY26 performance driven by healthy FMCG volume growth, margin expansion, and sustained market share gains across core categories. While weather disruptions and geopolitical challenges affected select segments, the company’s diversified portfolio, strong brands, and expanding digital engagement continue supporting its long-term growth trajectory.

FAQs

- What was Dabur India’s Q4FY26 net profit?

Dabur India reported Q4FY26 consolidated PAT of ₹368.6 crore, reflecting 15.1% year-on-year growth driven by margin expansion.

- Which business segment performed strongest for Dabur in Q4FY26?

The Home & Personal Care segment delivered strongest growth, rising 16.8% year-on-year led by hair care and home care products.

- What impacted Dabur’s international business during Q4FY26?

Geopolitical disturbances in the Middle East and currency-related volatility impacted growth in select overseas markets during the quarter.