Temporary Global Disruptions and Weak Technical Structure Weigh on Hospitality Major

Shares of Indian Hotels Company Limited (NSE:INDHOTEL) declined more than 4% in the latest trading session, closing near ₹634 despite the company reporting record FY26 earnings and continued expansion across brands and geographies. The stock slipped below its 51-day EMA near ₹647, indicating weakening near-term momentum amid broader market volatility and profit booking in hospitality counters.

The Tata Group hospitality major delivered its 16th consecutive best-ever quarter during Q4FY26 while strengthening its leadership position in India’s hospitality industry through aggressive portfolio expansion, premiumisation, and strong demand across leisure, weddings, and business travel segments.

Data Source: Company Filing; Image source: © 2026 Krish Capital Pty. Ltd., Analysis: Kalkine Group

IHCL Reports Record FY26 Revenue and Profit Growth

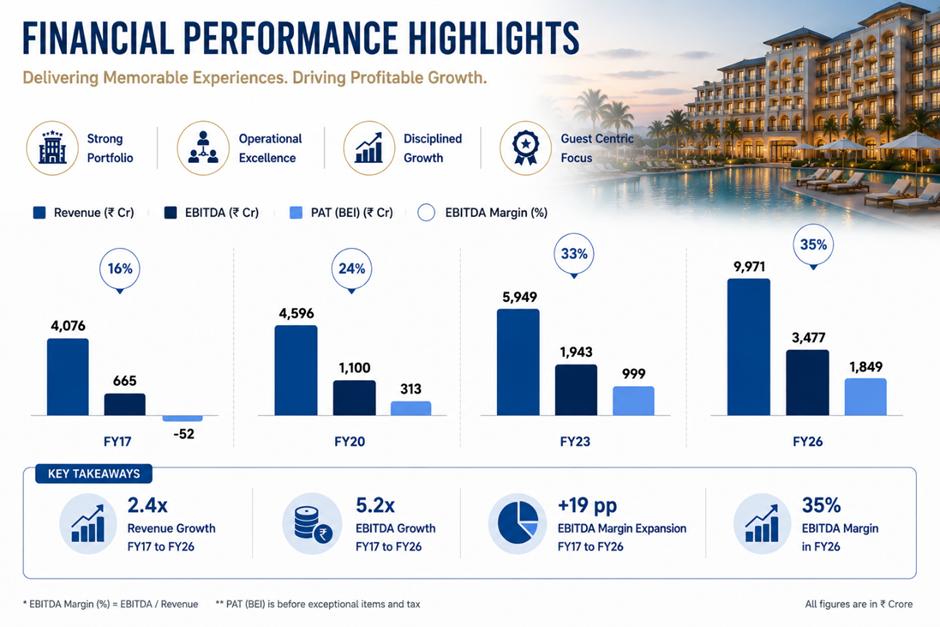

Indian Hotels Company Limited reported consolidated FY26 revenue of ₹9,971 crore, reflecting 16% year-on-year growth compared to FY25. EBITDA stood at ₹3,477 crore with EBITDA margin at 34.9%, while PAT before exceptional items rose 15% year-on-year to ₹1,849 crore. Reported PAT came in at ₹2,084 crore for FY26.

The company’s hotel segment generated revenue of ₹8,761 crore during FY26, while the air catering business contributed ₹1,219 crore. Management highlighted that the company achieved its FY26 revenue guidance despite macroeconomic and geopolitical disruptions during the year.

During Q4FY26, consolidated revenue increased 14% year-on-year to ₹2,845 crore, while EBITDA rose 15% to ₹1,052 crore with EBITDA margin of 37%. PAT before exceptional items stood at ₹600 crore for the quarter.

The company stated that Q4FY26 performance was impacted by temporary global disruptions including West Asia geopolitical tensions, airline route suspensions, and lower occupancy in Dubai hotels, which adversely affected revenue by nearly ₹40–45 crore at the consolidated level during March. However, strong domestic tourism demand, MICE activity, and wedding-led travel supported overall business resilience.

Expansion Strategy Strengthens Long-Term Growth Visibility

IHCL continued aggressive portfolio expansion during FY26, signing 250 hotels and opening 132 properties during the year. As of April 2026, the company’s portfolio crossed 1,000 units including hotels and amã villas, reinforcing its leadership in the Indian hospitality market.

The company currently operates 375 hotels with over 33,000 operational keys while maintaining a pipeline of 255 hotels and more than 31,000 keys across multiple brands including Taj, Vivanta, SeleQtions, Gateway, and Ginger.

IHCL’s capital-light growth strategy remains a key pillar of expansion, with nearly 93% of its pipeline based on managed and revenue-share lease models. Management expects more than 100 hotels to open over the next 24 months, supporting strong fee income growth.

The Ginger brand continued emerging as a strong growth driver, with the company targeting leadership in the mid-scale hospitality segment. Management also expects strategic acquisitions including ANK/Pride, Brij, and Atmantan to strengthen boutique leisure and wellness offerings.

Strong Balance Sheet and Demand Outlook Support Future Growth

IHCL ended FY26 with gross cash and cash equivalents exceeding ₹4,300 crore and maintained strong return ratios alongside rising free cash flow generation. The company’s dividend payout increased 44% year-on-year to ₹3.25 per share, including a special dividend to commemorate its 125th AGM.

Management remains optimistic on FY27 demand trends supported by tight room supply across key Indian cities, robust wedding demand, rising domestic tourism, and multiple large-scale sporting and MICE events scheduled during the year.

Technical Summary

Indian Hotels stock remains under pressure after slipping below its 51-day EMA near ₹647. The chart structure indicates continued consolidation with lower highs visible over recent months. RSI near 46 suggests weakening momentum and cautious sentiment. Immediate support is placed near ₹620, while resistance remains around ₹680–700 levels.

Chart by TradingView

Conclusion

Indian Hotels Company Limited delivered record FY26 financial performance supported by strong domestic travel demand, premiumisation, management fee growth, and rapid portfolio expansion. Its asset-light strategy, expanding Ginger platform, and strong balance sheet continue strengthening long-term growth visibility.

However, temporary geopolitical disruptions and near-term technical weakness may continue keeping investor sentiment cautious in the short term.

FAQs

- Why did Indian Hotels stock decline despite strong results?

The stock corrected due to profit booking, weak technical sentiment, and temporary global travel disruptions impacting hospitality stocks.

- What was IHCL’s FY26 consolidated revenue?

IHCL reported consolidated FY26 revenue of ₹9,971 crore, reflecting 16% year-on-year growth.

- What is IHCL’s expansion strategy?

The company is focusing on capital-light hotel expansion, management contracts, premiumisation, and scaling Ginger and leisure hospitality brands.