NOCIL Limited (NSE:NOCIL), India’s largest rubber chemicals manufacturer, reported subdued financial performance for Q4FY26 and FY26 as persistent dumping pressure, pricing challenges, and weak realizations continued to impact profitability. Despite margin pressure, the company witnessed improving volume momentum during the second half of FY26, supported by domestic demand recovery and stronger international business traction.

NOCIL shares declined over 3.5% during the session to around ₹182 after the earnings announcement. However, the stock continues to trade above its 50-day moving average, indicating improving medium-term momentum following a strong rebound from recent lows near ₹130.

Q4 FY26 Financial Performance

NOCIL reported Q4FY26 revenue from operations of ₹330 crore, registering a 5% sequential increase compared to ₹316 crore in Q3FY26. However, operating performance remained under pressure due to continued pricing weakness in the domestic market.

Operating EBITDA for the quarter stood at ₹21 crore, declining 22% quarter-on-quarter, while EBITDA margin narrowed to 6.4% from 8.5% in the previous quarter. Profit before tax increased 56% sequentially to ₹21 crore due to higher other income, while net profit rose sharply to ₹17 crore from ₹9 crore in Q3FY26.

Management stated that domestic volumes witnessed single-digit growth during the quarter, aided by improved demand conditions linked to GST 2.0 implementation. International markets also delivered single-digit growth as ongoing customer engagements converted into business opportunities.

The company highlighted that volume growth in H2FY26 remained strong at 12% YoY, helping offset weakness witnessed during the first half of the year. Overall FY26 volume growth stood at 3% year-on-year.

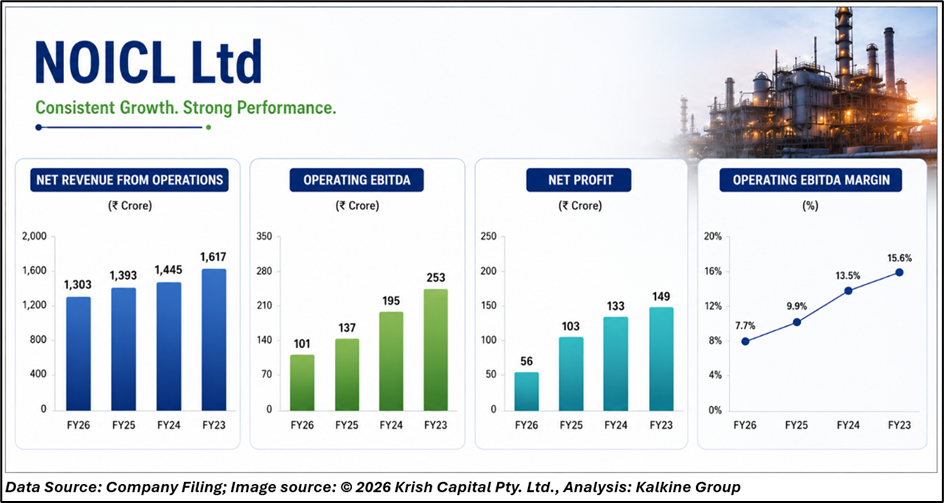

FY26 Financial Performance

For the full year FY26, NOCIL reported revenue from operations of ₹1,303 crore, reflecting a 6% decline compared to ₹1,393 crore in FY25. The decline was mainly attributed to pricing pressure arising from continued dumping in the domestic market.

Operating EBITDA declined significantly to ₹101 crore from ₹137 crore in FY25, while EBITDA margin contracted to 7.7% from 9.9% last year. Net profit for FY26 dropped sharply by 46% year-on-year to ₹56 crore compared to ₹103 crore in FY25.

The company also reported improved working capital efficiency, with cash flows from operating activities increasing substantially to ₹252 crore in FY26 versus ₹26 crore in FY25. Inventory levels reduced sharply to ₹158 crore from ₹281 crore a year earlier.

Strategy and Outlook

NOCIL remains optimistic about long-term demand opportunities driven by the global “China+1” sourcing strategy, where international tire manufacturers are increasingly seeking non-Chinese suppliers for supply-chain diversification. The company believes India is well-positioned to benefit from this shift.

To capitalize on future growth opportunities, NOCIL continues expanding its Dahej manufacturing facility through a ₹250 crore brownfield capex program. Management stated that the Dahej expansion remains within budget and has already entered the trial production phase, with customer validation and sampling currently underway.

The company also reiterated its focus on sustainability, green chemistry, and environmentally responsible manufacturing processes. NOCIL aims to strengthen its export footprint across Asia, Europe, and the United States while leveraging its diversified product portfolio and strong technical capabilities.

Dividend

NOCIL announced a dividend payout equivalent to 15% of face value for FY26, lower than the 20% payout declared in FY25. The company maintained a payout ratio of around 39% for FY26.

Technical Summary

NOCIL shares remain in a recovery trend after rebounding sharply from February-March lows near ₹130. The stock continues trading above its 50-day moving average, indicating improving momentum despite recent profit booking. Immediate support is placed near ₹175–₹170, while resistance remains around ₹190–₹200 in the near term.

Chart by TradingView

Conclusion

NOCIL faced a difficult FY26 amid pricing pressure and weak industry realizations, impacting margins and profitability. However, improving volumes, stronger export opportunities under the China+1 strategy, and ongoing Dahej expansion provide long-term growth visibility. Investors will closely monitor margin recovery, pricing stability, and execution of capacity expansion plans.

FAQs

- Why did NOCIL’s profit decline in FY26?

NOCIL’s profitability declined due to continued dumping pressure, weak pricing environment, and margin compression in the rubber chemicals market. - What is the China+1 opportunity for NOCIL?

Global tire manufacturers are increasingly diversifying sourcing away from China, creating export growth opportunities for Indian suppliers like NOCIL. - What is the status of NOCIL’s Dahej expansion project?

The Dahej brownfield expansion remains within the ₹250 crore budget and has entered the trial production and customer validation phase.